Finding the right loan in 2026 requires more than simply accepting the first offer that comes your way. Whether you're financing home improvements, covering medical expenses, or consolidating debt, taking the time to compare loan rates can save you thousands of dollars over the life of your loan. Understanding how to evaluate different loan products, what factors influence your rate, and which tools can help you make informed decisions will empower you to choose the financing option that best fits your financial situation and long-term goals.

Understanding What Affects Your Loan Rate

When you compare loan rates, you'll quickly notice that lenders don't offer everyone the same terms. Several key factors determine the rate you'll receive, and knowing these elements helps you understand why rates vary and how you might qualify for better terms.

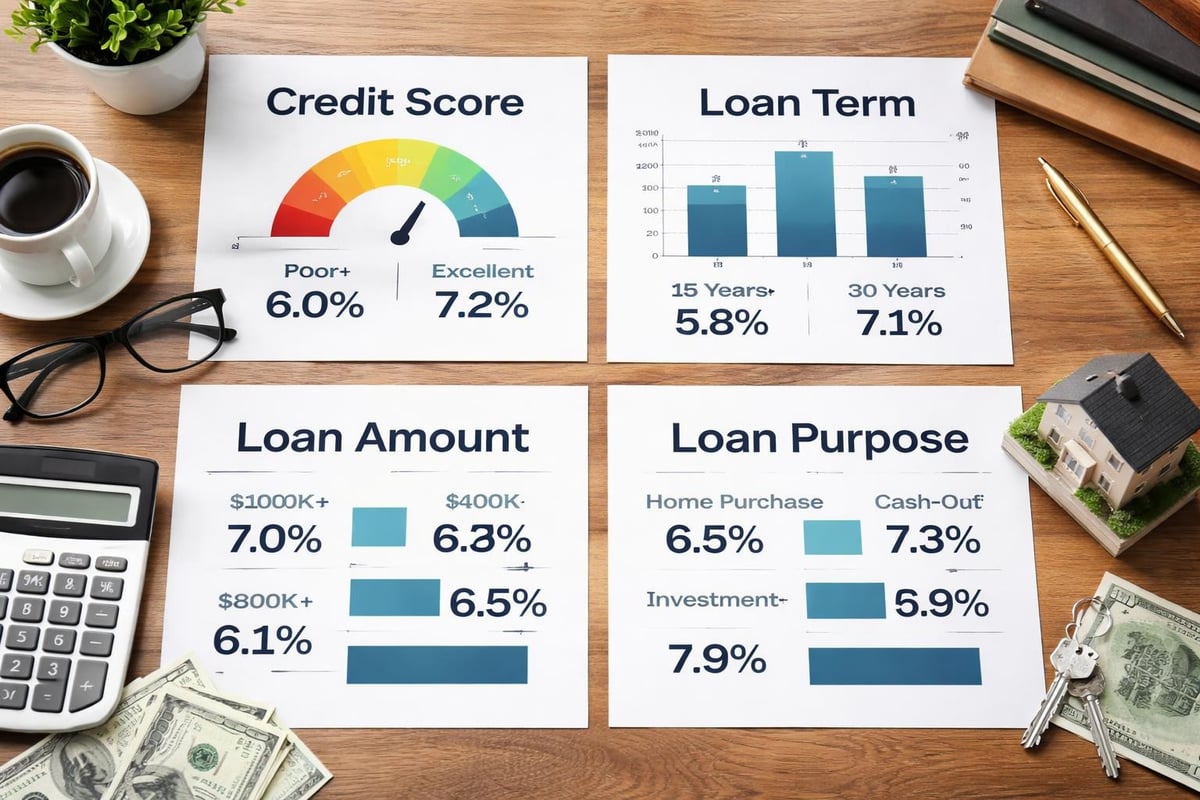

Credit Score Impact

Your credit score serves as one of the most significant determinants of your loan rate. Lenders use this three-digit number to assess how risky it is to lend you money. Higher credit scores typically unlock lower interest rates, while lower scores often result in higher rates to offset perceived risk.

For borrowers with past credit challenges, the good news is that many lenders, including those specializing in consumer lending across the Southeast, offer options even for those working to rebuild their credit. These loans may carry higher rates initially, but they provide an opportunity to improve your financial standing.

Loan Term Length

The duration of your loan significantly impacts both your interest rate and total cost:

- Short-term loans (1-3 years) usually feature lower interest rates but higher monthly payments

- Medium-term loans (3-5 years) balance affordable payments with reasonable interest costs

- Long-term loans (5-7 years) offer lower monthly payments but typically come with higher overall interest charges

When you compare loan rates across different terms, calculate the total amount you'll pay over the loan's lifetime, not just the monthly payment.

Loan Amount and Purpose

Lenders often adjust rates based on how much you're borrowing and what you plan to use the funds for. Personal loans for home improvements might qualify for different rates than those for medical expenses or debt consolidation. Larger loan amounts sometimes qualify for better rates because they generate more interest revenue for lenders, though this varies by institution.

Key Metrics Beyond the Interest Rate

While the interest rate catches most people's attention first, savvy borrowers know to compare loan rates using several metrics to understand the true cost of borrowing.

Annual Percentage Rate (APR)

The APR represents the total cost of your loan expressed as a yearly rate, including both the interest rate and fees. This makes it a more comprehensive measure than interest rate alone. When comparing offers from multiple lenders, the APR gives you an apples-to-apples comparison.

| Metric | What It Includes | Why It Matters |

|---|---|---|

| Interest Rate | Cost of borrowing the principal | Determines base monthly payment |

| APR | Interest rate + fees + closing costs | Shows true total cost |

| Monthly Payment | Principal + interest divided by term | Affects monthly budget |

| Total Interest Paid | All interest over loan life | Reveals long-term cost |

Origination Fees and Other Costs

Some lenders charge origination fees ranging from 1% to 8% of the loan amount. Others might advertise no origination fees but compensate with higher interest rates. The Consumer Financial Protection Bureau provides guidance on comparing loan estimates to help borrowers understand these different cost structures.

Always request a complete breakdown of fees when evaluating loan offers. Hidden costs can make an apparently attractive rate much less competitive once all expenses are factored in.

Tools and Resources to Compare Loan Rates

In 2026, borrowers have access to numerous digital tools that simplify the comparison process. These resources help you evaluate multiple offers simultaneously and understand how different loan structures impact your finances.

Online Comparison Calculators

Several reputable financial websites offer free comparison tools. Bankrate’s loan comparison calculator allows you to input details from multiple loan offers and view them side-by-side, making it easier to identify the best option for your situation.

These calculators typically let you compare:

- Different interest rates and how they affect monthly payments

- Various loan terms and their impact on total cost

- The effect of origination fees on overall expenses

- Total interest paid over the life of each loan

- Break-even points if you're considering refinancing

Rate Comparison Platforms

Platforms like Bankrate and PrimeRates aggregate current rates from multiple lenders, providing a snapshot of what's available in the market. While these platforms offer excellent starting points, remember that the rates shown typically represent offers for borrowers with excellent credit.

Your actual rate will depend on your unique financial profile, including your credit score, income, existing debt obligations, and the specific loan amount and term you're requesting.

How to Effectively Compare Loan Rates

Simply looking at numbers isn't enough. You need a systematic approach to ensure you're making a fair comparison and selecting the loan that truly serves your best interests.

Gather Multiple Quotes

Request loan quotes from at least three to five lenders. This gives you a realistic picture of available rates and strengthens your negotiating position. When requesting quotes, provide the same information to each lender to ensure comparable offers.

Include a mix of lender types in your search:

- Traditional banks with physical branches

- Credit unions serving your area

- Online lenders with streamlined applications

- Regional consumer lending specialists

Compare Identical Terms

To accurately compare loan rates, evaluate offers with the same basic parameters. If you're comparing a three-year loan from one lender with a five-year loan from another, you're not making a fair comparison. Match the loan amounts and terms as closely as possible.

Understand Rate Locks

Some lenders offer rate locks, guaranteeing your quoted rate for a specific period, typically 30 to 60 days. This can be valuable in a rising rate environment, but make sure you understand any fees associated with the lock and how long it remains valid.

Special Considerations for Different Loan Types

Different types of personal loans may require specific comparison strategies. Understanding these nuances helps you focus on the most relevant factors for your particular financing need.

Home Improvement Loans

When financing home improvements, consider whether you're comparing secured or unsecured loans. Secured loans using your home as collateral typically offer lower rates but carry more risk. Home improvement loans may also qualify for tax benefits in some cases, affecting the true cost of borrowing.

Medical Expense Financing

Medical loans often feature competitive rates because they address essential needs. Some healthcare providers partner with specific lenders to offer preferential terms. When you compare loan rates for medical expenses, ask about:

- Deferred interest promotional periods

- Hardship programs if your situation changes

- Direct payment to medical providers

- Flexibility for ongoing treatment costs

Educational Financing

Private student loans vary significantly in terms and rates. NerdWallet’s student loan comparison shows how different lenders structure their educational financing products. Pay particular attention to repayment terms, deferment options, and whether rates are fixed or variable.

Negotiating Better Rates

Many borrowers don't realize that loan rates aren't always set in stone. Particularly with consumer lenders who value long-term customer relationships, there's often room for negotiation.

Leverage Competing Offers

If you've received a better rate from one lender, don't hesitate to share this with others. Many lenders will attempt to match or beat competitive offers to earn your business. Present your competing offers professionally and ask if they can improve their terms.

Improve Your Negotiating Position

Several strategies can strengthen your position when you compare loan rates and negotiate terms:

- Demonstrate stable income with recent pay stubs and tax returns

- Show a history of on-time payments for existing obligations

- Offer a larger down payment if applicable to your loan type

- Consider a shorter loan term to reduce lender risk

- Ask about relationship discounts if you're an existing customer

Timing Your Application

Economic conditions influence lending rates. While you can't control federal rate policies, you can monitor trends and time your application strategically. If rates are currently high but projected to decrease, waiting a few months might save you money, assuming your situation allows for flexibility.

Red Flags When Comparing Loan Offers

As you compare loan rates, watch for warning signs that might indicate predatory lending practices or unfavorable terms that could cause financial hardship.

Unrealistic Rate Promises

If a rate seems dramatically better than all other offers you've received, investigate thoroughly. Some lenders advertise low teaser rates that apply only under very specific circumstances or for limited periods. Read the fine print and verify that the advertised rate matches what you qualify for based on your credit profile.

Pressure Tactics

Reputable lenders understand that comparing offers takes time. Be wary of anyone who pressures you to sign immediately or claims that a special rate expires in just hours. Take the time you need to compare loan rates properly and make an informed decision.

Excessive Fees

While some fees are standard, excessive charges can indicate a lender is padding profits at your expense. Compare the total fee structure across lenders, not just the interest rate:

| Fee Type | Reasonable Range | Red Flag Territory |

|---|---|---|

| Origination Fee | 1-5% of loan amount | 8% or higher |

| Application Fee | $0-50 | $100+ |

| Prepayment Penalty | None preferred | Any significant penalty |

| Late Payment Fee | $25-35 | $50+ or percentage-based |

Making Your Final Decision

After you've gathered quotes, used comparison tools, and evaluated all terms, it's time to make your final decision. This choice should balance multiple factors beyond just securing the lowest rate.

Total Cost Calculation

Calculate the total amount you'll repay over the loan's lifetime for each offer. Multiply your monthly payment by the number of months in the loan term, then add any upfront fees. This reveals the true cost difference between offers.

Payment Affordability

Even the best rate won't help if the monthly payment strains your budget. Apply the 28/36 rule as a guideline: your monthly debt payments (including the new loan) shouldn't exceed 36% of your gross monthly income. Leave yourself a financial cushion for unexpected expenses.

Lender Reputation and Service

Consider the lender's reputation for customer service, especially if you might need flexibility later. Local and regional lenders often provide more personalized service and may be more willing to work with you if your circumstances change. For residents of Louisiana, Mississippi, Tennessee, and Georgia, having access to branch offices where you can speak with someone face-to-face offers advantages that purely online lenders can't match.

Flexibility and Features

Review the loan's flexibility features:

- Can you make extra payments without penalties?

- Is there an option to skip a payment if needed?

- Does the lender offer rate reduction programs for automatic payments?

- Are there hardship programs if you experience financial difficulties?

Long-Term Financial Impact

The loan you choose today will affect your finances for years to come. As you compare loan rates and finalize your decision, consider how this loan fits into your broader financial picture.

Building Positive Credit History

Regardless of your current credit situation, every loan offers an opportunity to build positive payment history. Even if you don't qualify for the lowest rates today, making consistent on-time payments can improve your credit score, potentially allowing you to refinance at better terms in the future.

Future Refinancing Opportunities

Monitor your loan and the lending market after closing. If rates drop significantly or your credit improves substantially, refinancing might save you money. When you initially compare loan rates, ask about refinancing policies and any fees that might apply.

Taking the time to thoroughly compare loan rates ensures you secure financing that supports rather than strains your financial goals. The difference between rates might seem small at first glance, but over the life of a loan, even a percentage point can translate to significant savings. Whether you're financing a home improvement project, covering medical expenses, or pursuing educational opportunities, Standard Financial offers flexible financing solutions with transparent terms across our branch locations in Louisiana, Mississippi, Tennessee, and Georgia, helping you find the right loan for your unique situation, even if you've faced credit challenges in the past.

No comment yet, add your voice below!