Navigating the lending landscape with poor credit can feel overwhelming, but adding a cosigner to your personal loan application might provide the solution you need. A personal loan with cosigner bad credit represents a viable path for borrowers who struggle to qualify on their own, though understanding the requirements and implications for both parties is essential. This arrangement allows lenders to evaluate the combined financial strength of two individuals rather than relying solely on one applicant's credit profile, potentially opening doors that would otherwise remain closed.

Understanding the Cosigner Dynamic for Bad Credit Borrowers

A cosigner essentially vouches for your ability to repay a loan by agreeing to take on equal responsibility for the debt. When you apply for a personal loan with cosigner bad credit, the lender evaluates both your financial profile and your cosigner's creditworthiness. This dual assessment can significantly improve your chances of approval, especially when your own credit score falls below the lender's typical threshold.

The cosigner relationship works because it mitigates risk from the lender's perspective. If you default on payments, the cosigner becomes legally obligated to cover the remaining balance. This guarantee gives lenders confidence to extend credit they might otherwise deny.

What Lenders Examine in Cosigned Applications

Financial institutions assess several key factors when reviewing a personal loan with cosigner bad credit:

- Combined debt-to-income ratios from both applicants

- Credit scores of each party, with greater weight on the cosigner's profile

- Employment stability and income verification for both individuals

- Payment history across all existing credit accounts

- Outstanding debts and current financial obligations

Most lenders prefer cosigners with credit scores above 670, though requirements vary by institution. Income stability matters equally, as lenders want assurance that at least one party has consistent cash flow to support monthly payments.

Can Your Cosigner Have Bad Credit Too?

One of the most common questions borrowers ask is whether a cosigner can also have poor credit. The short answer is that while technically possible, having a cosigner with bad credit significantly reduces the benefits of this arrangement. Lenders typically require cosigners to demonstrate strong creditworthiness precisely because they're offsetting the primary borrower's financial weaknesses.

When both parties have compromised credit, lenders face compounded risk. This scenario often results in loan denial or extremely unfavorable terms, including higher interest rates and stricter repayment schedules. According to industry experts who analyze cosigner qualifications, the cosigner's credit profile should ideally compensate for the primary borrower's shortcomings.

Minimum Cosigner Qualifications

Different lenders maintain varying standards, but most require cosigners to meet these baseline criteria:

| Requirement | Typical Threshold | Purpose |

|---|---|---|

| Credit Score | 670+ (Good to Excellent) | Demonstrates creditworthiness |

| Debt-to-Income Ratio | Below 43% | Ensures repayment capacity |

| Employment History | 2+ years stable income | Confirms income reliability |

| Bankruptcy History | None in past 7 years | Indicates financial stability |

| Legal Status | U.S. citizen or permanent resident | Meets regulatory requirements |

These standards exist to protect both the lender and, surprisingly, the borrower. A financially stable cosigner increases approval odds while potentially securing better interest rates, ultimately reducing the total cost of borrowing.

Finding the Right Cosigner for Your Situation

Identifying someone willing and qualified to cosign a personal loan with cosigner bad credit requires careful consideration. The ideal candidate combines strong credit, stable income, and a genuine willingness to help. Family members often serve as cosigners, though close friends or mentors sometimes fulfill this role as well.

Before approaching anyone, honestly assess what you're asking. The risks associated with cosigning include potential credit damage if you miss payments, strained relationships, and financial liability that could last years. Transparency about your financial situation and repayment plan demonstrates respect for the commitment you're requesting.

Approaching Potential Cosigners Professionally

- Prepare your financial documentation including recent pay stubs, tax returns, and a detailed budget showing how you'll manage payments

- Explain your specific need for the loan, whether for debt consolidation, medical expenses, home improvements, or education

- Present a concrete repayment strategy with realistic timelines and contingency plans

- Discuss potential risks openly without minimizing the responsibility you're asking them to assume

- Offer regular financial updates throughout the loan term to maintain transparency and trust

This structured approach shows maturity and increases the likelihood someone will agree to support your application.

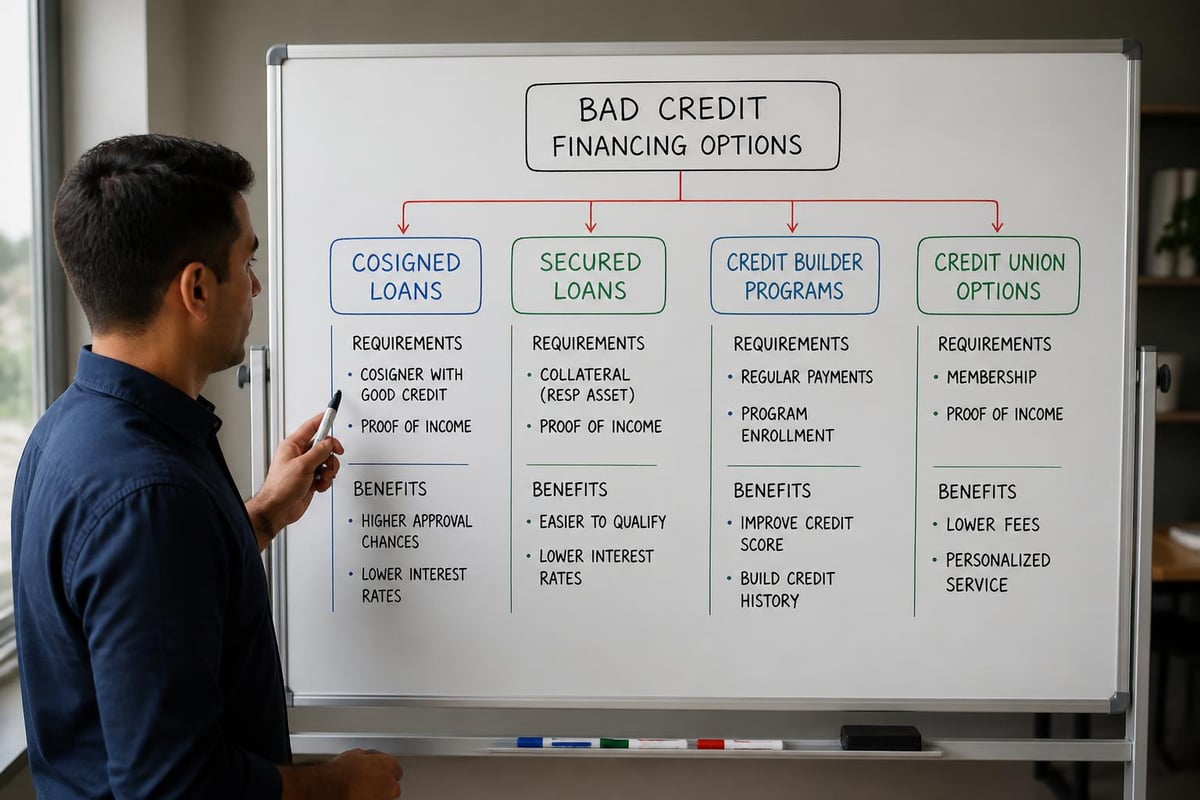

Alternative Paths When Cosigner Options Are Limited

Not everyone has access to a qualified cosigner, and some individuals prefer to avoid placing this burden on friends or family. Fortunately, several alternatives exist for obtaining financing despite poor credit. Exploring various loan options reveals multiple pathways to securing necessary funds.

Secured personal loans represent one viable option. By pledging collateral such as a vehicle, savings account, or other valuable asset, you reduce lender risk without involving a third party. The trade-off is that you could lose the collateral if you default on payments.

Credit unions often maintain more flexible lending standards than traditional banks. These member-owned institutions sometimes offer specialized programs for individuals rebuilding credit, with more personalized underwriting that considers factors beyond just credit scores.

Building Your Credit Before Applying

Sometimes the best strategy involves delaying your loan application while actively improving your credit profile:

- Dispute errors on your credit reports through all three bureaus

- Become an authorized user on someone else's well-managed credit card

- Pay down existing balances to improve your credit utilization ratio

- Make all payments on time for at least six months before applying

- Avoid new credit inquiries that could temporarily lower your score

Even modest improvements in your credit score can dramatically impact loan terms and approval odds. A jump from 580 to 620, for instance, might qualify you for significantly better interest rates.

Understanding Interest Rates and Loan Terms

When you secure a personal loan with cosigner bad credit, expect interest rates higher than those offered to prime borrowers but lower than what you'd receive alone. As of 2026, rates for cosigned loans to borrowers with poor credit typically range from 12% to 28%, depending on the lender, loan amount, and cosigner's credit strength.

Loan terms also vary based on creditworthiness and the amount borrowed. Most personal loans span two to seven years, with longer terms reducing monthly payments but increasing total interest paid over the life of the loan.

| Loan Amount | Typical Term Options | Monthly Payment Example (18% APR) |

|---|---|---|

| $5,000 | 2-5 years | $242 (3 years) |

| $10,000 | 3-5 years | $299 (5 years) |

| $15,000 | 3-7 years | $387 (5 years) |

| $25,000 | 5-7 years | $645 (5 years) |

These figures illustrate why shopping around for the best rates matters. Even a few percentage points difference can save hundreds or thousands of dollars over the loan's duration.

Reading the Fine Print

Before signing any loan agreement, scrutinize these often-overlooked details:

- Prepayment penalties that charge fees for paying off the loan early

- Origination fees that reduce the actual amount you receive

- Variable vs. fixed rates and how rate changes could affect payments

- Default terms explaining what triggers penalties or acceleration

- Cosigner release provisions that might allow removing the cosigner after consistent payments

Understanding these elements prevents unpleasant surprises and helps you select the most advantageous loan structure for your circumstances.

Protecting Your Cosigner's Interests

Responsible borrowers recognize the significant favor a cosigner provides and take active steps to protect this person from negative consequences. When someone agrees to support your personal loan with cosigner bad credit application, they're placing considerable faith in your financial discipline and commitment.

Resources for understanding cosigner requirements emphasize that this arrangement impacts both parties' credit reports. Every payment, whether on time or late, appears on both credit profiles. This shared responsibility means your financial behavior directly affects your cosigner's creditworthiness.

Best Practices for Cosigned Loans

Set up automatic payments through your checking account to eliminate the risk of forgetting due dates. Most lenders offer this option and some even provide small interest rate discounts for enrolling in autopay.

Communicate proactively if financial difficulties arise. Contacting your cosigner before missing a payment allows both parties to explore solutions rather than creating surprises that damage trust and credit.

Consider insurance options that could cover payments if you become unable to work due to disability or unemployment. While these products add to your costs, they provide valuable protection for both you and your cosigner.

Make extra payments when possible to reduce the principal balance faster and minimize the total interest paid. This strategy also demonstrates financial responsibility and builds positive payment history.

How Regional Lenders Approach Cosigned Loans

Community-based financial institutions across the Southeast often take a more personalized approach to lending compared to large national banks. These lenders frequently consider factors beyond credit scores, including local employment stability, community ties, and individual circumstances that contributed to credit challenges.

Regional lenders in states like Louisiana, Mississippi, Tennessee, and Georgia understand the economic realities facing their communities. This local perspective sometimes translates to more flexible underwriting standards, especially when applicants can demonstrate recent financial stability despite past credit issues.

What Sets Community Lenders Apart

- Face-to-face consultations that allow for explaining extenuating circumstances

- Relationship-based decisions that consider your full financial picture

- Flexible documentation requirements that accommodate various employment situations

- Local economic understanding that contextualizes creditworthiness

- Ongoing support throughout the loan term, not just at origination

These advantages make exploring regional lending options worthwhile, particularly when national lenders have denied your applications.

Managing Your Loan Successfully

Once approved for a personal loan with cosigner bad credit, your focus shifts to successful repayment. This phase determines whether you rebuild your credit, maintain your relationship with your cosigner, and position yourself for independent borrowing in the future.

Creating a dedicated repayment budget ensures you prioritize loan payments above discretionary spending. Calculate your monthly payment amount, add it to your essential expenses, and structure your budget around this fixed obligation. Many borrowers find success by treating their loan payment like rent or utilities-non-negotiable expenses paid before anything else.

Tracking Your Progress

Monitor your credit score quarterly to watch your progress as consistent payments rebuild your credit profile. Many credit card companies and financial apps now offer free score tracking, making this easier than ever.

Keep records of all payments including confirmation numbers and dated receipts. This documentation proves invaluable if disputes arise or if you need to demonstrate payment history for future credit applications.

Update your cosigner regularly with brief status reports showing on-time payments and declining principal balances. These updates reinforce their decision to help you and maintain positive relationships.

Explore refinancing opportunities after 12-18 months of consistent payments. As your credit improves, you might qualify to refinance the loan in your name only, releasing your cosigner from their obligation.

Special Considerations for Different Loan Purposes

The purpose of your personal loan with cosigner bad credit can influence both approval odds and optimal loan structure. Lenders view different loan purposes through varying risk lenses, affecting terms and requirements.

Home improvement loans often receive favorable consideration because they increase property value, creating tangible assets. Documentation showing specific project plans and contractor estimates strengthens these applications.

Medical expense loans address urgent needs that lenders generally understand. Providing itemized bills and payment plans from healthcare providers demonstrates the legitimate nature of your request.

Education-related loans for career advancement or skill development can improve approval odds when you demonstrate how the education will increase earning potential. Understanding the benefits and risks of cosigned loans helps both parties make informed decisions about supporting educational pursuits.

Debt consolidation loans receive scrutiny because they often indicate past financial struggles. However, showing a clear plan to avoid accumulating new debt while paying off the consolidation loan can reassure lenders.

| Loan Purpose | Typical Approval Factors | Documentation Needed |

|---|---|---|

| Home Improvement | Property value increase potential | Contractor estimates, project plans |

| Medical Expenses | Urgent healthcare needs | Medical bills, payment plans |

| Education | Career advancement prospects | Enrollment verification, cost breakdown |

| Debt Consolidation | Realistic repayment plan | List of debts, monthly expenses |

| Emergency Expenses | Nature and urgency of need | Supporting documentation of emergency |

Tailoring your application to emphasize how your specific purpose mitigates risk can improve outcomes.

Building Independence for Future Borrowing

While a cosigner provides immediate access to needed funds, most borrowers aspire to eventually qualify independently. Your personal loan with cosigner bad credit represents an opportunity to demonstrate creditworthiness and establish the payment history necessary for future solo applications.

Every on-time payment reports to credit bureaus, gradually improving your credit score. Most borrowers see meaningful improvement after six months of consistent payments, with significant gains occurring around the 12-18 month mark. This timeline makes personal loans powerful credit-building tools when managed responsibly.

Beyond just making payments, focus on comprehensive credit health. Keep credit card balances below 30% of available limits, maintain diverse credit types, and avoid new hard inquiries unless absolutely necessary. These practices complement your loan payments to maximize credit score improvements.

Timeline for Credit Recovery

Months 1-6: Establish perfect payment history and begin seeing minor score improvements as positive payment data accumulates.

Months 7-12: Credit scores typically rise more substantially as consistent behavior demonstrates reliability. Some borrowers move from "poor" to "fair" credit tiers during this period.

Months 13-24: With continued responsible management, many borrowers reach "good" credit territory, qualifying for better rates and independent loan approvals.

Beyond 24 months: Sustained positive payment history positions you for premium rates and terms, with past credit issues receding in importance as recent behavior dominates your credit profile.

This progression varies based on individual circumstances, but the pattern holds across most credit rebuilding journeys. Finding strategies for obtaining personal loans with bad credit provides additional insights into maximizing your credit recovery through strategic borrowing.

Securing a personal loan with cosigner bad credit opens financial opportunities while providing a pathway to rebuild your credit profile through responsible repayment. Whether you need funds for home improvements, medical expenses, education, or other essential purposes, understanding cosigner requirements and protecting both parties' interests creates a foundation for success. Standard Financial specializes in helping borrowers throughout Louisiana, Mississippi, Tennessee, and Georgia access flexible financing solutions, even when past credit challenges have created obstacles elsewhere. With personalized service and understanding of local economic realities, we work with applicants to find solutions that fit their unique circumstances and support their financial goals.

No comment yet, add your voice below!