Your credit score affects nearly every major financial decision in your life, from securing a mortgage to qualifying for personal loans. Whether you're planning a home improvement project, need medical financing, or want to refinance existing debt, understanding how to improve credit score fast can save you thousands of dollars in interest charges and open doors to better opportunities. The good news is that with the right strategies and consistent effort, you can see meaningful improvements in your score within weeks or months rather than years.

Understanding What Impacts Your Credit Score

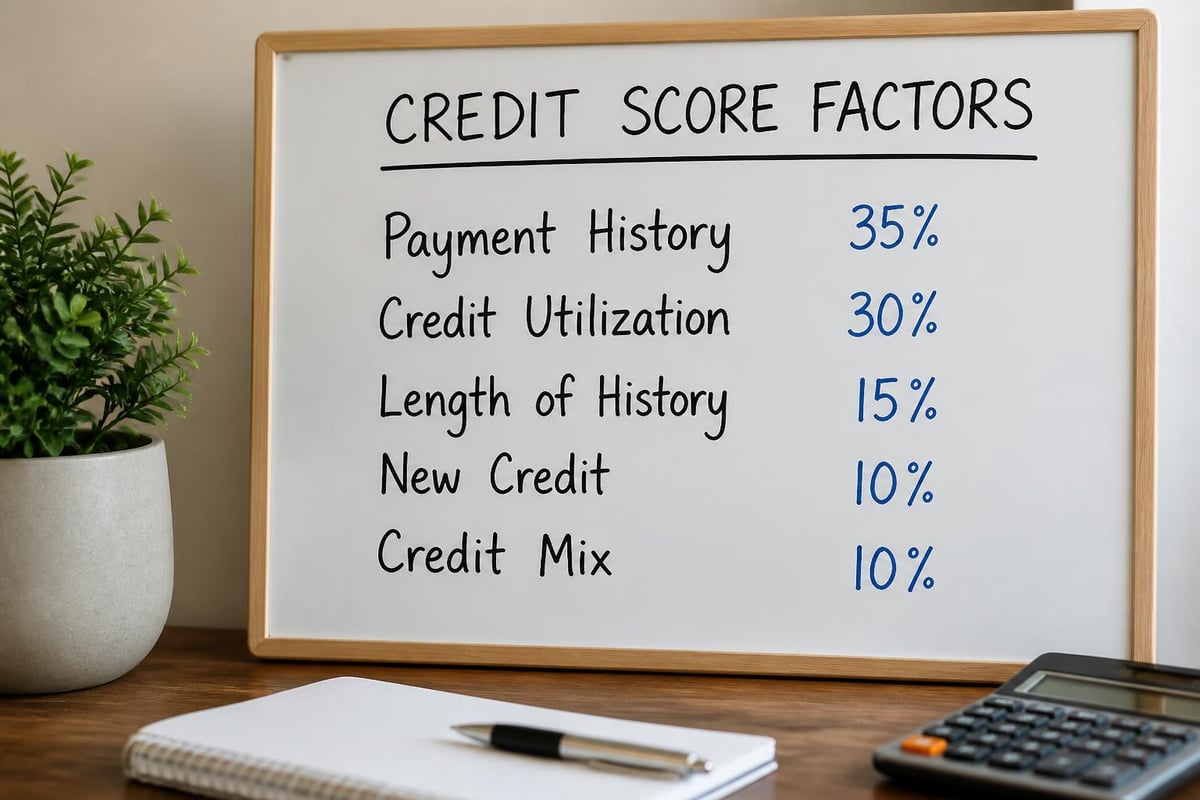

Before diving into improvement strategies, you need to understand the components that determine your credit score. Payment history accounts for approximately 35% of your FICO score, making it the single most important factor. This includes whether you've paid past credit accounts on time, the number of late payments, and how recently those late payments occurred.

Credit utilization ratio comes in second at 30% of your score. This measures how much of your available credit you're currently using across all accounts. Length of credit history (15%), new credit inquiries (10%), and credit mix (10%) round out the remaining factors.

Key factors affecting your credit score:

- Payment history and on-time payment patterns

- Total debt compared to available credit limits

- Age of your oldest and newest credit accounts

- Recent credit applications and hard inquiries

- Mix of credit types (revolving credit, installment loans, mortgages)

Understanding these percentages helps you prioritize which actions will have the most significant impact when learning how to improve credit score fast.

Pay Down Credit Card Balances Strategically

One of the fastest ways to boost your score involves reducing your credit card balances below 30% of your available limits. Even better, aim for utilization below 10% on each individual card and across all cards combined. This strategy can yield results within 30-45 days once your card issuers report the lower balances to credit bureaus.

The Avalanche vs. Snowball Approach

Two proven methods exist for tackling credit card debt. The avalanche method focuses on paying off cards with the highest interest rates first while making minimum payments on others. This saves money on interest charges over time. The snowball method targets your smallest balances first, creating psychological wins that build momentum.

For credit score improvement specifically, consider a third approach: balance distribution. If you have one card maxed out at $5,000 and another with only $500 used on a $5,000 limit, paying down the maxed-out card will improve your score faster than paying off the smaller balance.

| Strategy | Best For | Credit Score Impact Speed |

|---|---|---|

| Avalanche | Minimizing interest costs | Moderate (2-3 months) |

| Snowball | Building motivation | Moderate (2-3 months) |

| Balance Distribution | Fastest score improvement | Fast (1-2 months) |

Multiple small payments throughout the month can also help. Credit card companies typically report your balance to bureaus once monthly, usually on your statement closing date. Making payments before this date reduces the reported balance and immediately improves your utilization ratio.

Dispute Credit Report Errors Immediately

According to consumer protection studies, approximately 20% of credit reports contain errors that could negatively impact scores. Reviewing your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) should be your first step in learning how to improve credit score fast.

Common errors include accounts that don't belong to you, incorrect payment statuses, duplicate accounts, and outdated negative information. You're entitled to one free credit report annually from each bureau through AnnualCreditReport.com.

The Dispute Process

When you identify an error, file disputes with each bureau reporting the mistake. The bureaus have 30 days to investigate your claim. During this investigation period, they must verify the information with the creditor. If the creditor can't verify the disputed item, it must be removed from your report.

Steps to dispute credit report errors:

- Document the error with supporting evidence (receipts, payment confirmations, account statements)

- File disputes online with each credit bureau reporting the error

- Send certified letters to creditors directly for serious errors

- Follow up after 30 days if you haven't received a response

- Request written confirmation of any corrections or deletions

Successful dispute resolutions, especially for negative items like late payments or collections that shouldn't be there, can boost your score by 50-100 points almost immediately. Experian provides detailed guidance on improving your credit score through error correction and other proven methods.

Become an Authorized User on Established Accounts

This strategy works particularly well for people with limited credit history or those recovering from past credit issues. When someone adds you as an authorized user on their credit card account, that account's payment history and credit limit can appear on your credit report.

The key is choosing the right account. Look for someone with excellent payment history, low credit utilization, and a long account history. The age of their account and their responsible usage patterns can transfer positive information to your credit profile.

However, this strategy requires trust and clear communication. You don't need to actually use the card or even possess it. Simply being listed as an authorized user can provide the credit score benefit. The account holder also maintains complete control and can remove you at any time without affecting their own credit.

Request Credit Limit Increases

Requesting higher credit limits on existing cards provides an immediate decrease in your credit utilization ratio without requiring you to pay down balances. This method for how to improve credit score fast works because it increases your total available credit while your debt remains the same.

Most credit card issuers allow you to request limit increases online every six months. Before requesting, ensure you have several months of on-time payments and preferably some history of responsible usage with that specific issuer.

Timing Your Requests

The best time to request a credit limit increase is when you've recently received a raise, changed jobs with higher income, or paid down significant debt. These factors demonstrate improved creditworthiness to lenders. Some issuers perform only a soft inquiry (which doesn't hurt your score), while others use a hard inquiry. Always ask which type they'll use before proceeding.

If you have three credit cards with $3,000 limits and $1,500 in total debt, your utilization is 50%. If you successfully increase each limit to $5,000, your utilization drops to 10% with the same debt level. This single action could improve your score by 20-40 points within the next reporting cycle.

Make All Payments On Time Moving Forward

While catching up on missed payments matters, establishing a perfect payment record from today forward creates the foundation for long-term credit health. Payment history carries the most weight in your credit score calculation, and strategies to raise your credit score fast emphasize that consistency matters more than perfection in the past.

Set up automatic payments for at least the minimum amount due on every account. Most banks and credit card companies offer free automatic payment options. Even if you plan to pay more than the minimum, automating the base payment ensures you never miss a due date due to oversight.

Payment automation best practices:

- Schedule automatic payments for 2-3 days before the due date

- Set calendar reminders to verify sufficient funds in your account

- Keep email and text alerts enabled for payment confirmations

- Review statements monthly even with automation enabled

- Maintain a cushion in your checking account to prevent overdrafts

One missed payment can drop your score by 60-110 points, and it remains on your report for seven years. The impact diminishes over time, but preventing future late payments is crucial. If you do miss a payment, make it as soon as possible. Payments less than 30 days late typically aren't reported to credit bureaus.

Consider a Secured Credit Card or Credit-Builder Loan

For those with limited credit history or severe credit damage, traditional credit cards may be unavailable. Secured credit cards and credit-builder loans offer pathways to establish positive payment history while learning how to improve credit score fast.

A secured credit card requires a cash deposit that typically becomes your credit limit. You use it like a regular credit card, and the issuer reports your payment activity to credit bureaus. After 12-18 months of responsible use, many issuers graduate you to an unsecured card and return your deposit.

| Product Type | Deposit Required | Typical Timeline | Credit Impact |

|---|---|---|---|

| Secured Credit Card | $200-$500 | Reports monthly | Builds utilization & payment history |

| Credit-Builder Loan | Varies by lender | 6-24 months | Builds payment history & credit mix |

| Authorized User | None | Immediate | Adds account history & age |

Credit-builder loans work differently. The lender places the loan amount in a savings account that you can't access. You make monthly payments, and once the loan is paid off, you receive the funds. This creates a positive payment history without the risk of accumulating debt you can't afford.

Both options typically show positive results on your credit report within 2-3 months of your first reported payment. For individuals recovering from bankruptcy or foreclosure, these tools provide essential stepping stones back to mainstream credit.

Optimize Your Credit Mix Carefully

While credit mix accounts for only 10% of your score, having different types of credit can provide incremental improvements. Lenders like to see that you can manage various credit responsibilities, from revolving credit (credit cards) to installment loans (auto loans, personal loans, mortgages).

However, never take on debt solely to improve your credit mix. The potential score increase doesn't justify paying interest on loans you don't need. Instead, consider how your legitimate borrowing needs might naturally diversify your credit portfolio.

When Adding Credit Types Makes Sense

If you only have credit cards and need to finance a necessary expense like home improvements, medical procedures, or education costs, choosing an installment loan adds diversity to your credit profile while serving a genuine purpose. Understanding what constitutes a good credit score helps you evaluate whether your current credit mix is holding you back or if other factors deserve more attention.

Personal loans from consumer lenders often provide flexible terms that accommodate various credit levels, making them accessible options for building credit mix while addressing real financial needs. These loans typically have fixed payments over 12-60 months, creating a predictable payment history that demonstrates reliability to future lenders.

Avoid Hard Inquiries When Possible

Each time you apply for new credit, lenders typically perform a hard inquiry that can temporarily lower your score by 5-10 points. While the impact is small and fades within a year, multiple inquiries in a short period signal financial stress to lenders.

Rate shopping for certain loans (mortgages, auto loans, student loans) gets special treatment. Credit scoring models recognize that consumers compare rates, so multiple inquiries for the same loan type within 14-45 days typically count as a single inquiry.

Minimize hard inquiries by:

- Researching which lenders use soft pulls for prequalification

- Spacing out credit applications by at least six months when possible

- Using prequalification tools that don't affect your credit score

- Only applying for credit you genuinely need and qualify for

- Understanding the difference between hard and soft inquiries

Soft inquiries, such as checking your own credit score or prequalification checks initiated by lenders for promotional offers, don't affect your credit score at all. Many credit card companies and personal finance websites offer free credit score monitoring with soft inquiries, allowing you to track your progress as you work on how to improve credit score fast.

Address Collections and Charge-Offs Strategically

Negative items like collections and charge-offs significantly damage your credit score. While paying them doesn't remove them from your report, it does change their status from unpaid to paid, which looks better to lenders even if your score doesn't immediately increase.

Negotiate before you pay. Collection agencies often accept less than the full amount owed. Request a "pay-for-delete" agreement in writing before making payment. While not all collectors agree to this, some will remove the negative item from your credit report in exchange for payment.

The Seven-Year Rule

Most negative information automatically falls off your credit report after seven years from the date of first delinquency. Paying an old collection can sometimes restart the clock on how long it appears on your report, so research the age of the debt before taking action.

For debts within the statute of limitations in your state, prioritize those most recently reported. Recent negative items hurt your score more than older ones. As negative items age, their impact diminishes, so a three-year-old collection hurts less than a three-month-old one.

Legitimate debts still deserve attention, and managing resumed student loan payments has become particularly important for many consumers in recent years. Working with creditors to establish payment plans often prevents further credit damage and demonstrates good faith effort.

Keep Old Accounts Open

The average age of your credit accounts significantly influences your credit score. Closing old accounts, especially your oldest credit card, reduces your average account age and can hurt your score. It also reduces your total available credit, increasing your utilization ratio.

Even if you don't use an old credit card regularly, keep it active with a small recurring charge like a streaming subscription. Pay it off monthly to maintain the account in good standing without carrying a balance. This preserves your credit history length and available credit.

Managing old accounts effectively:

- Set up a small automatic monthly charge on unused cards

- Automate full payment of that charge to prevent interest charges

- Check statements quarterly to catch any fraudulent activity

- Store unused cards securely at home rather than carrying them

- Verify the issuer won't close accounts due to inactivity

Card issuers may close accounts that remain inactive for extended periods (typically 6-12 months). Before that happens, they usually send a warning notice. If you receive such a notice, make a small purchase to demonstrate activity and preserve the account.

Monitor Your Progress Regularly

Tracking your credit score allows you to see which strategies are working and adjust your approach accordingly. Many credit card issuers now provide free FICO score access to cardholders, updating monthly. Third-party services also offer free credit monitoring with various score models.

Understanding that different scoring models exist helps set realistic expectations. FICO scores range from 300-850, while VantageScore uses the same range but calculates differently. A score of 670-739 is generally considered good, 740-799 very good, and 800+ exceptional. The broader societal benefits of improving credit scores extend beyond individual financial gains to community-wide economic stability.

Create a tracking spreadsheet noting your score, utilization ratio, payment history, and any new accounts or inquiries each month. This documentation helps you identify patterns and maintain motivation as you see progress. Most people following these strategies see meaningful improvement within 3-6 months, though individual results vary based on starting point and specific issues.

Use Statement Dates to Your Advantage

Credit card companies report your balance to credit bureaus on your statement closing date, not your payment due date. This distinction matters when you're focused on how to improve credit score fast through utilization management.

Making payments before your statement closes means a lower balance gets reported, even if you weren't carrying a balance month-to-month. For example, if you charge $2,000 during your billing cycle and your statement closes on the 15th with payment due on the 10th of the next month, paying that $2,000 on the 14th results in a $0 balance being reported.

Strategic Payment Timing

Call your credit card issuers or check online to find your statement closing dates. Note these dates for all cards and schedule payments a day or two before closing. This strategy requires no additional money, just better timing of payments you'd make anyway.

Some people maintain utilization under 10% by making multiple payments throughout the month rather than waiting for the due date. This approach works particularly well if you use credit cards for daily purchases to earn rewards but want to maintain excellent credit scores simultaneously.

Understand Geographic and Industry Considerations

Credit needs and opportunities vary by region and circumstance. In states like Louisiana, Mississippi, Tennessee, and Georgia, where many consumers work in industries with seasonal income fluctuations or face unexpected expenses, understanding flexible financing options becomes particularly important.

Regional economic factors influence lending practices and credit accessibility. Working with lenders who understand local markets and challenges can provide better outcomes than national institutions with rigid criteria. Community-focused lenders often have more flexibility in working with clients who have past credit issues but demonstrate current financial responsibility.

Higher credit scores enhance mortgage opportunities and reduce interest rates on all types of borrowing. For residents planning home purchases or improvements in growing Southern markets, credit score improvement translates directly to better buying power and lower monthly payments.

The Role of Income Stability

While income doesn't directly affect credit scores, it influences debt-to-income ratios that lenders consider alongside your credit score. Stable employment history and consistent income make lenders more willing to approve applications despite lower credit scores.

Document income stability by maintaining records of employment, pay stubs, and tax returns. When applying for credit, being able to demonstrate reliable income sometimes compensates for a score that's still improving. This proves particularly valuable for essential financing needs that can't wait for perfect credit scores.

Improving your credit score quickly requires strategic action across multiple areas: reducing utilization, ensuring perfect payment timing, correcting errors, and building positive history through diverse account types. These proven strategies can show results within weeks while building long-term financial health over months. If you're facing immediate financing needs while working to improve your credit, Standard Financial specializes in helping clients throughout Louisiana, Mississippi, Tennessee, and Georgia access flexible personal loans for home improvements, medical expenses, education, and refinancing, even with past credit challenges. Our local teams understand that credit scores tell only part of your financial story and work with you to find solutions that fit your situation.

No comment yet, add your voice below!