Managing significant expenses without depleting your savings often requires a structured financing solution. Monthly payment loans provide consumers across Louisiana, Mississippi, Tennessee, and Georgia with a predictable way to cover everything from home improvements to medical bills. These loans transform large expenses into manageable monthly installments, making essential purchases and services accessible while maintaining financial stability. Understanding how these lending products work empowers borrowers to make informed decisions that align with their budget and long-term financial goals.

Understanding the Foundation of Monthly Payment Loans

Monthly payment loans, commonly known as installment loans, offer borrowers a lump sum upfront with repayment spread across a predetermined schedule. Unlike revolving credit that fluctuates with usage, these loans maintain consistent payment amounts throughout the term. Installment loans represent one of the most established forms of consumer financing, providing transparency and predictability that helps families budget effectively.

The structure involves three primary components: principal, interest, and term length. The principal represents the actual amount borrowed, while interest compensates the lender for providing access to funds. Term length determines how many months you'll make payments, directly influencing both payment size and total interest paid.

Key Features That Define Monthly Payment Loans

These financing products share several distinguishing characteristics:

- Fixed payment amounts that remain constant throughout the loan term

- Predetermined repayment schedule with specific due dates

- Closed-end structure where the account closes upon final payment

- Fully amortizing payments that cover both principal and interest

- Transparent terms disclosed before signing any agreement

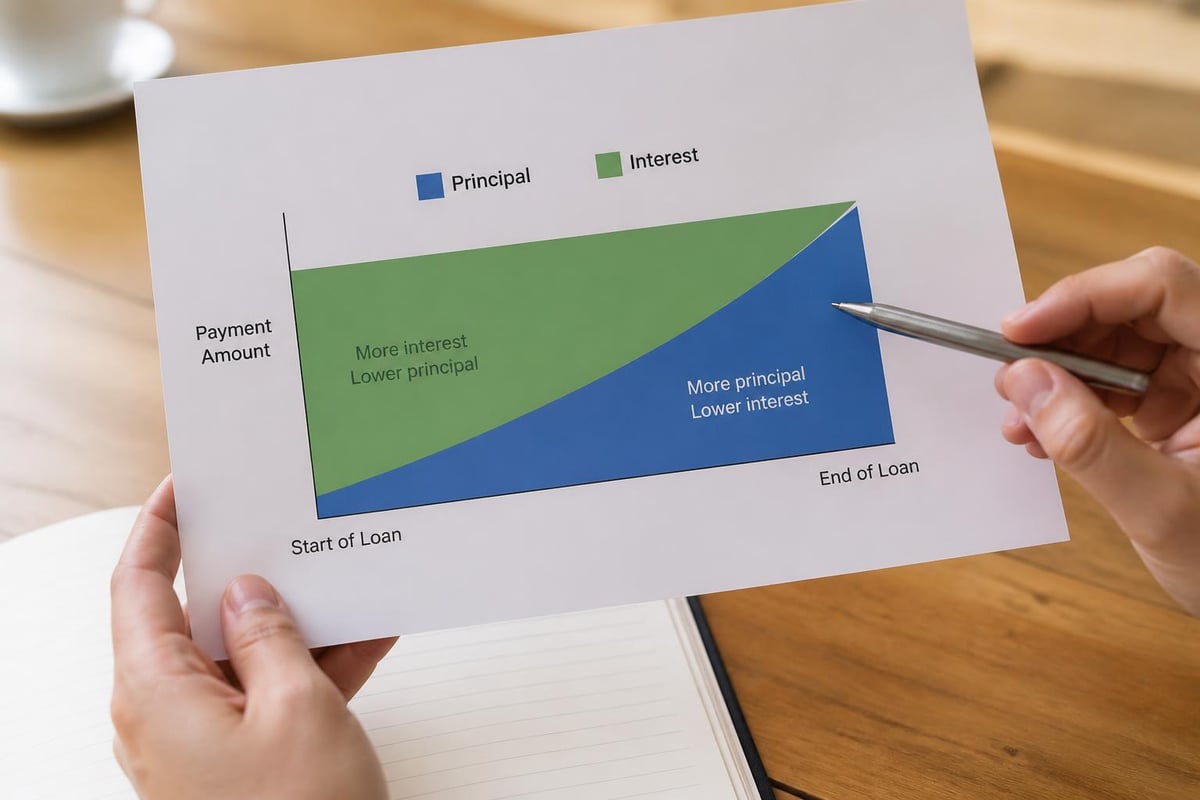

Most lenders calculate payments using an amortization schedule that ensures the loan is completely paid off by the final payment date. Early payments primarily cover interest charges, while later payments apply more toward the principal balance. This structure provides certainty that each payment brings you closer to complete ownership or debt elimination.

Types of Monthly Payment Loans Available to Consumers

The consumer lending market offers various monthly payment loan products designed for different financial needs and circumstances.

Personal Loans for General Use

Personal loans provide unsecured financing for almost any purpose. Borrowers receive funds directly and choose how to allocate them across expenses like debt consolidation, medical procedures, or educational costs. These loans typically range from $1,000 to $50,000 with terms between 12 and 84 months.

Advantages include:

- No collateral required

- Faster approval than secured loans

- Flexible use of proceeds

- Fixed interest rates in most cases

Auto Loans and Vehicle Financing

Vehicle financing represents one of the most common forms of monthly payment loans. The automobile serves as collateral, often resulting in lower interest rates compared to unsecured options. Terms typically extend from 36 to 72 months, though longer terms have become increasingly available.

| Loan Term | Typical Use Case | Monthly Payment Impact |

|---|---|---|

| 36 months | Used vehicles, quick payoff | Higher payments, less interest |

| 48-60 months | New vehicles, balanced approach | Moderate payments, moderate interest |

| 72+ months | Premium vehicles, budget constraints | Lower payments, higher total interest |

Home Improvement Loans

Dedicated home improvement financing helps homeowners upgrade, repair, or expand their properties without tapping home equity. These monthly payment loans typically offer amounts sufficient for kitchen remodels, roof replacements, or HVAC system upgrades.

The predictable payment structure helps homeowners budget for necessary improvements while potentially increasing property value. Many borrowers prefer these over home equity loans because they avoid placing their home at direct risk.

Medical Financing Options

Healthcare expenses can emerge unexpectedly, and monthly payment loans designed for medical purposes help patients access necessary treatments without delay. These specialized loans may cover procedures ranging from dental work to elective surgeries not fully covered by insurance.

Some medical financing programs offer promotional periods with reduced or zero interest, making them attractive for patients who can repay within specific timeframes.

How Monthly Payment Loans Compare to Alternative Financing

Understanding how these loans stack up against other borrowing options helps consumers select the most appropriate solution.

Monthly Payment Loans vs. Credit Cards

Credit cards offer revolving credit with variable payments based on outstanding balances. In contrast, monthly payment loans provide fixed amounts and unchanging payment schedules. Credit card interest rates frequently exceed those of personal loans, particularly for borrowers with less-than-perfect credit histories.

Key differences:

- Payment predictability: Loans offer consistency, cards vary monthly

- Interest rate structure: Loans typically provide lower fixed rates

- Borrowing flexibility: Cards allow repeated borrowing up to limits

- Credit utilization impact: Installment loans don't affect utilization ratios the same way

Payday Loans vs. Structured Monthly Payment Loans

Payday loans and cash advances typically require full repayment within two weeks to one month, creating potential financial strain. Monthly payment loans distribute repayment across months or years, reducing the burden of each individual payment. Recent reports show that payday borrowers continue facing significant rollover fees despite protective measures.

For consumers seeking alternatives to payday lending, payday alternative loans from federal credit unions offer more manageable terms. Standard monthly payment loans from established consumer lenders provide even greater flexibility and typically charge significantly lower interest rates.

Buy Now, Pay Later Options

The rise of Buy Now, Pay Later services has introduced short-term installment options for retail purchases. While these products divide purchases into payments, they typically span only weeks or months rather than the extended terms traditional monthly payment loans offer.

BNPL fees can accumulate when payments are missed, potentially negating the convenience. Consumers should evaluate whether BNPL fits their financial situation before committing to multiple payment plans simultaneously.

Determining Your Monthly Payment Amount

Several factors influence the specific payment amount you'll make each month throughout your loan term.

Principal Amount Borrowed

The starting loan balance directly affects payment size. Borrowing $5,000 results in lower payments than borrowing $15,000, assuming identical interest rates and terms. Carefully assess how much you actually need rather than borrowing the maximum approved amount.

Interest Rate Assessment

Your interest rate reflects the cost of borrowing and significantly impacts both monthly payments and total repayment amount. Rates vary based on:

- Credit score and credit history

- Debt-to-income ratio

- Employment stability

- Loan type and collateral status

- Current market conditions

Borrowers with stronger credit profiles typically qualify for lower rates, reducing the cost of monthly payment loans over time.

Term Length Considerations

Loan term represents the number of months you'll make payments. Shorter terms mean higher monthly payments but less total interest paid. Longer terms reduce payment size but increase total interest costs.

| Loan Amount | 36-Month Payment | 60-Month Payment | Total Interest (36 mo) | Total Interest (60 mo) |

|---|---|---|---|---|

| $10,000 at 8% | $313 | $203 | $1,272 | $2,164 |

| $10,000 at 12% | $332 | $222 | $1,968 | $3,346 |

| $10,000 at 16% | $352 | $243 | $2,696 | $4,616 |

Selecting the appropriate term balances immediate affordability with long-term cost efficiency.

Qualifying for Monthly Payment Loans

Lenders evaluate multiple factors when considering applications for monthly payment loans.

Credit Score Requirements

While specific thresholds vary by lender, credit scores influence both approval decisions and rate offers. Many consumer lenders work with borrowers across the credit spectrum, including those with past credit challenges. Some lenders specialize in serving customers rebuilding their credit, offering monthly payment loans designed to improve financial standing through consistent repayment.

Income and Employment Verification

Demonstrating stable income assures lenders of your repayment capacity. Most lenders require:

- Recent pay stubs or income statements

- Employment verification

- Bank account information

- Identification documents

Self-employed borrowers may need additional documentation like tax returns or profit-and-loss statements.

Debt-to-Income Ratio Analysis

Lenders calculate your debt-to-income (DTI) ratio by dividing monthly debt obligations by gross monthly income. Lower ratios indicate greater capacity to handle additional monthly payment loans. Most lenders prefer DTI ratios below 40%, though flexibility exists based on other compensating factors.

Managing Your Monthly Payment Loan Successfully

Responsible loan management protects your credit and financial wellbeing while ensuring you meet your obligations.

Budgeting for Consistent Payments

Incorporate your loan payment into monthly budgets as a non-negotiable expense alongside housing, utilities, and food. Setting up automatic payments from your checking account eliminates the risk of missed due dates and potential late fees.

Budgeting strategies include:

- Aligning payment due dates with your income schedule

- Creating a separate account dedicated to loan payments

- Building a small buffer for financial emergencies

- Reviewing your budget monthly for optimization opportunities

Building Credit Through Timely Payments

Monthly payment loans provide excellent opportunities to establish or rebuild credit. Payment history represents the most significant factor in credit score calculations. Consistent on-time payments demonstrate reliability to future lenders.

Some borrowers strategically use these loans specifically for credit building, selecting manageable amounts they can comfortably repay. The installment account adds diversity to credit profiles that may consist primarily of revolving credit.

Refinancing Opportunities

As your financial situation improves or market rates change, refinancing existing monthly payment loans might reduce your interest rate or adjust your term. Refinancing can lower monthly payments, accelerate payoff timelines, or both depending on your goals.

Consider refinancing when:

- Your credit score has improved significantly

- Market interest rates have decreased

- Your income has increased substantially

- You want to consolidate multiple loans

Regional Considerations for Southern State Borrowers

Consumers in Louisiana, Mississippi, Tennessee, and Georgia benefit from competitive lending markets with numerous options for monthly payment loans.

State-Specific Lending Regulations

Each state maintains its own consumer protection laws governing lending practices. These regulations may affect maximum interest rates, fee structures, and disclosure requirements. Working with established lenders familiar with regional regulations ensures compliance and fair treatment.

Local Economic Factors

Regional employment patterns, cost of living variations, and economic conditions influence loan terms and availability. Lenders with physical branch locations in these states often understand local market conditions better than national online-only competitors.

Community-Focused Lending

Regional lenders frequently demonstrate greater flexibility for borrowers with unique circumstances or credit challenges. Branch-based operations enable face-to-face consultations that help borrowers explore options and find suitable monthly payment loans for their specific needs.

Common Uses for Monthly Payment Loans in the Southeast

Borrowers throughout Louisiana, Mississippi, Tennessee, and Georgia utilize these loans for various purposes that reflect regional priorities and challenges.

Home Improvement and Repair

Older housing stock throughout the region often requires ongoing maintenance and upgrades. Monthly payment loans finance projects like:

- Roof repairs after storm damage

- HVAC replacement in humid climates

- Foundation work addressing soil conditions

- Energy efficiency improvements reducing utility costs

Medical and Dental Expenses

Healthcare costs continue rising nationwide, and medical financing helps families access necessary care. Monthly payment loans cover everything from emergency procedures to planned treatments not fully covered by insurance plans.

Educational Investment

Whether funding certification programs, technical training, or college expenses, education loans structure tuition and related costs into manageable monthly obligations. These investments in human capital often generate returns through enhanced earning potential.

Vehicle Purchase and Repair

Both urban and rural residents throughout the Southeast rely heavily on personal vehicles for transportation. Monthly payment loans make vehicle acquisition affordable while auto repair loans keep existing vehicles operational when unexpected mechanical issues arise.

Avoiding Common Pitfalls with Monthly Payment Loans

Understanding potential challenges helps borrowers navigate the lending process successfully.

Borrowing More Than Necessary

The temptation to borrow the maximum approved amount can lead to unnecessarily high payments and interest costs. Carefully calculate actual needs and borrow only that amount, leaving borrowing capacity for genuine emergencies.

Ignoring Total Loan Cost

Focusing exclusively on monthly payment size without considering total repayment amount can prove costly. A longer-term loan with lower payments might cost thousands more in interest compared to a shorter-term alternative.

Missing Payment Obligations

Late or missed payments trigger multiple negative consequences:

- Late fees adding to your balance

- Negative credit reporting

- Potential rate increases on variable products

- Damage to lender relationships

Contact your lender immediately if payment difficulties arise. Many offer hardship programs or payment arrangements that protect your credit while addressing temporary financial challenges.

Failing to Read Loan Agreements

All loan terms appear in your agreement, including interest rates, payment schedules, fees, and prepayment policies. Review these documents thoroughly before signing. Ask questions about unclear provisions and understand all obligations before committing.

Monthly payment loans provide structured, predictable financing that helps consumers manage significant expenses while maintaining financial stability. By understanding loan types, comparing options carefully, and managing repayment responsibly, borrowers can leverage these products to achieve their goals without overwhelming their budgets. If you're considering financing for home improvements, medical expenses, education, or other needs across Louisiana, Mississippi, Tennessee, or Georgia, Standard Financial offers flexible solutions tailored to your unique situation, including options for those rebuilding their credit.

No comment yet, add your voice below!