Accessing credit without a traditional bank account presents unique challenges, but it's not impossible. Thousands of Americans manage their finances outside the conventional banking system, yet they still need access to personal loans for emergencies, medical expenses, home improvements, and other essential needs. Understanding how to secure personal loans with no bank account requires knowledge of alternative lending options, payment methods, and the documentation lenders require to verify your ability to repay.

Understanding Personal Loans Without Bank Accounts

Many people assume that having a checking or savings account is a mandatory requirement for any loan application. While most traditional lenders prefer borrowers with established bank accounts, alternative lending options exist for those without bank accounts. The banking requirement typically serves two purposes: verifying income through deposit history and providing a convenient method for disbursing funds and collecting payments.

Why Lenders Prefer Bank Accounts

Financial institutions use bank accounts as a risk assessment tool. Your banking history demonstrates financial responsibility, regular income deposits, and spending patterns that help lenders evaluate your creditworthiness. When you apply for personal loans with no bank account, lenders lose this valuable source of verification data.

Key reasons lenders value bank accounts include:

- Direct deposit capabilities for loan disbursement

- Automated payment processing for monthly installments

- Transaction history showing income stability

- Reduced risk of missed or late payments

- Lower administrative costs for payment processing

Without a traditional bank account, you'll need to demonstrate financial stability through alternative documentation. Pay stubs, tax returns, utility bill payment histories, and employment verification letters become critical components of your application.

Alternative Payment Methods for Loan Processing

Securing personal loans with no bank account means you'll need alternative methods for receiving funds and making payments. Several viable options exist that satisfy both borrower needs and lender requirements.

Prepaid Debit Cards

Many lenders now accept prepaid debit cards as substitutes for traditional bank accounts. These cards function similarly to checking accounts, allowing direct deposits and automatic withdrawals. Major prepaid card providers like Netspend, Green Dot, and Bluebird offer routing and account numbers that work with most lending platforms.

| Payment Method | Pros | Cons |

|---|---|---|

| Prepaid Debit Cards | FDIC insured, accepts direct deposit, wide acceptance | Monthly fees, limited features, potential load fees |

| Money Orders | No account needed, widely accepted, secure | Must purchase in person, tracking required, inconvenient |

| Cash Payments | Universal acceptance, immediate confirmation | Requires branch visits, no automatic payments, time-consuming |

| Check Cashing Services | Immediate access to funds, no account required | High fees (2-5% of loan amount), multiple visits needed |

Money Transfer Services

Services designed for consumers without bank accounts include Western Union, MoneyGram, and similar platforms. While these work for receiving loan funds, they're less practical for making regular monthly payments due to transaction fees and the need for repeated in-person visits.

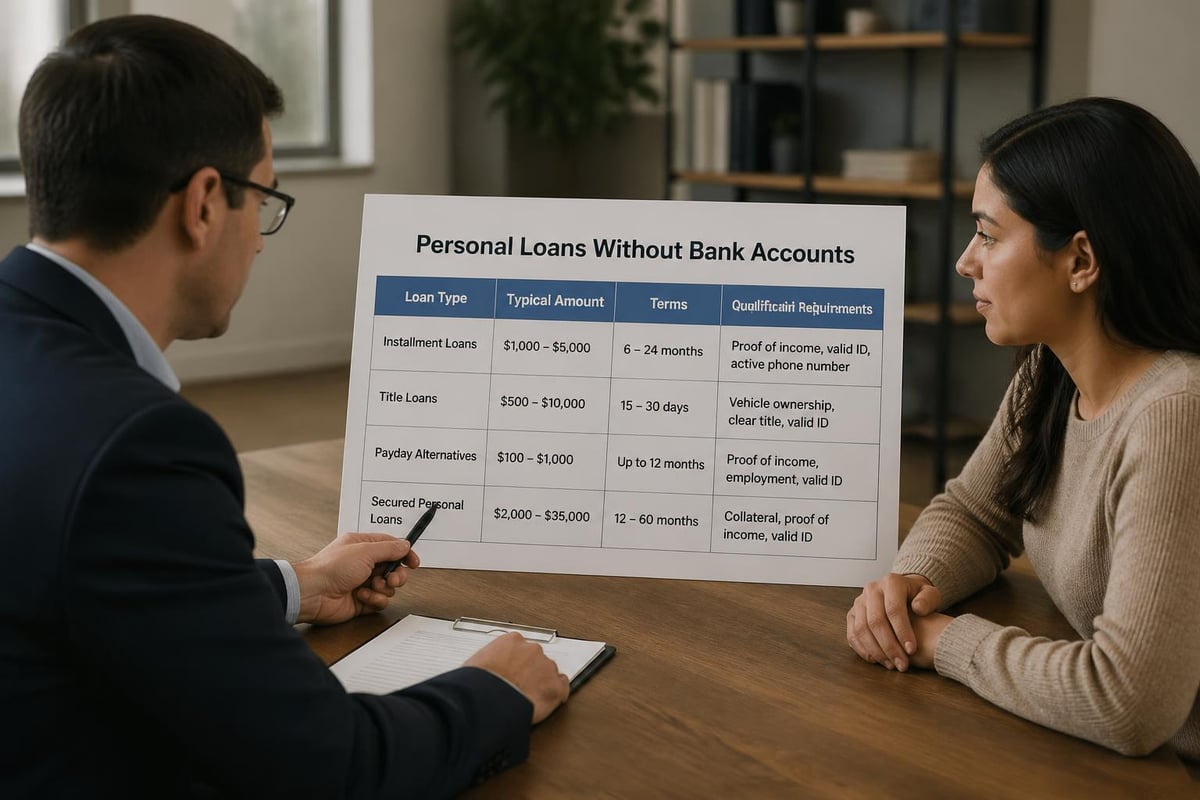

Types of Loans Available Without Banking Relationships

Not all personal loans with no bank account offer the same terms or serve the same purposes. Understanding your options helps you select the most appropriate financing for your situation.

Installment Loans

Traditional installment loans remain accessible to borrowers without bank accounts, though you may face higher interest rates or stricter requirements. These loans provide a lump sum upfront with fixed monthly payments over a predetermined period, typically ranging from six months to five years.

Common installment loan features:

- Fixed monthly payment amounts

- Predictable repayment schedules

- Loan amounts from $500 to $25,000

- Interest rates varying based on creditworthiness

- Secured or unsecured options available

Title Loans

Auto title loans use your vehicle as collateral, making them easier to obtain without a bank account. However, these loans carry significant risks, including extremely high interest rates (often 25% per month or 300% APR) and the possibility of losing your vehicle if you default.

Payday Alternative Loans (PALs)

Credit unions offer PALs as safer alternatives to traditional payday loans. These small-dollar loans (typically $200 to $1,000) come with more reasonable terms and lower fees. Understanding the requirements for these specialized loan products helps you determine eligibility even without traditional banking relationships.

Documentation Requirements for Non-Banked Borrowers

When applying for personal loans with no bank account, you'll need stronger alternative documentation to prove your identity, income, and residency. Lenders require this information to comply with federal regulations and assess your ability to repay.

Identity Verification

Acceptable forms of identification include:

- Valid government-issued photo ID (driver's license, passport, state ID)

- Social Security card or Individual Taxpayer Identification Number (ITIN)

- Birth certificate (when combined with other documents)

- Military ID or veteran identification card

Income Documentation

Without bank statements showing regular deposits, you must provide direct evidence of your earnings. Most lenders accept multiple forms of income verification to build a complete financial picture.

| Document Type | Verification Strength | Availability |

|---|---|---|

| Recent Pay Stubs (2-3 months) | High | Employed individuals |

| Tax Returns (1-2 years) | Very High | Self-employed, contractors |

| Employer Verification Letter | High | Currently employed borrowers |

| Social Security/Disability Statements | High | Benefit recipients |

| Court-Ordered Payment Records | Medium | Alimony, child support recipients |

Proof of Residency

Establishing your current address helps lenders contact you and verify your stability. Utility bills (electric, water, gas), lease agreements, mortgage statements, or property tax records all serve as acceptable proof of residency.

Finding Legitimate Lenders Who Accept Non-Banked Borrowers

Navigating the lending landscape without a bank account requires caution. Predatory lenders often target unbanked consumers with deceptive practices and exploitative terms.

Researching Lender Credentials

Before applying for personal loans with no bank account, verify that lenders hold appropriate licenses in your state. Check with your state's financial regulation department and review online complaint databases through the Consumer Financial Protection Bureau (CFPB).

Red flags indicating predatory lending:

- Guaranteed approval regardless of credit history

- Pressure to sign documents immediately

- Unclear or hidden fee structures

- Interest rates exceeding state usury limits

- Requests for upfront fees before loan approval

- No physical business address or license information

Regional and Community Lenders

Local lenders often demonstrate more flexibility with banking requirements than national institutions. Credit unions, community banks, and regional consumer finance companies may offer personal loans with no bank account when they can verify income and identity through alternative means.

Examining loan options from specialized lenders reveals that some institutions specifically design products for unbanked consumers. These lenders understand the documentation challenges and accept alternative verification methods.

Interest Rates and Fees for Non-Traditional Borrowers

Personal loans with no bank account typically carry higher costs than conventional loans. Lenders compensate for increased risk and administrative complexity by charging elevated interest rates and additional fees.

Understanding Cost Structures

Typical fee categories include:

- Origination fees (1-8% of loan amount)

- Monthly maintenance or service fees

- Late payment penalties

- Returned payment fees (for rejected money orders or cash payment issues)

- Early prepayment penalties (less common but possible)

Interest rates for borrowers without bank accounts often range from 15% to 36% APR for personal installment loans from reputable lenders. Predatory lenders may charge substantially more, sometimes exceeding 100% APR or higher.

Building Financial Stability While Repaying Your Loan

Securing personal loans with no bank account can serve as a stepping stone toward greater financial inclusion. Using your loan responsibly helps build credit and demonstrates your readiness for traditional banking services.

Creating a Payment Strategy

Without automatic bank withdrawals, you must develop a systematic approach to making timely payments. Set reminders on your phone, mark payment due dates on a physical calendar, and budget for the payment amount plus any processing fees.

Payment management best practices:

- Schedule payments 3-5 days before the due date to account for processing time

- Keep confirmation numbers or receipts for every payment

- Maintain a payment ledger tracking dates, amounts, and confirmation details

- Budget extra funds to cover transaction fees associated with non-bank payment methods

- Contact your lender immediately if you anticipate payment difficulties

Considering Banking Options

While you may currently operate without a bank account by choice or circumstance, establishing a banking relationship offers long-term benefits. Second-chance checking accounts, designed for people with past banking problems, provide entry points into traditional financial services.

Many credit unions and community banks offer basic checking accounts with minimal fees and no minimum balance requirements. These accounts can help you access better loan terms in the future and simplify financial management.

State-Specific Regulations Affecting Loan Availability

Where you live significantly impacts your ability to obtain personal loans with no bank account. States regulate consumer lending differently, with some imposing strict interest rate caps and licensing requirements while others allow more lender flexibility.

Regional Lending Environments

In states like Louisiana, Mississippi, Tennessee, and Georgia, consumer finance companies operate under specific state charters that permit personal installment loans to borrowers who might not qualify at traditional banks. These lenders often have more flexible policies regarding bank account requirements.

Exploring options available to consumers without traditional banking reveals significant variation in product availability by geographic location. Understanding your state's lending laws helps you identify legitimate loan products and recognize illegal lending practices.

| State | Interest Rate Cap | Special Provisions |

|---|---|---|

| Louisiana | 36% on loans under $1,500 | Licensed lenders may exceed cap with approval |

| Mississippi | No statutory cap | Regulations focus on licensing and disclosure |

| Tennessee | 24% for most consumer loans | Higher rates allowed for small loans under $2,500 |

| Georgia | Variable by loan type | Strict anti-predatory lending laws |

Alternative Financial Services and Their Loan Programs

Beyond traditional lenders, alternative financial service providers increasingly offer personal loans with no bank account. These companies understand that millions of Americans operate outside conventional banking and have developed products to serve this market.

Fintech and Online Lenders

Technology-driven lenders often demonstrate more flexibility with banking requirements. They may accept prepaid debit cards, digital wallets, or other electronic payment methods that traditional banks reject. However, online lenders still require income verification and identity documentation.

Community Development Financial Institutions (CDFIs)

CDFIs focus on serving underbanked communities and may offer more accessible loan products. These mission-driven organizations prioritize financial inclusion over profit maximization, often resulting in lower rates and more flexible requirements for borrowers without traditional bank accounts.

Managing Multiple Financial Obligations Without Banking Services

If you're juggling personal loans with no bank account alongside other financial responsibilities, organization becomes critical. Without the automatic tracking that bank statements provide, you need manual systems to monitor your obligations.

Creating a Financial Dashboard

Essential elements to track:

- All loan balances and current amounts owed

- Payment due dates for each obligation

- Payment confirmation numbers and dates

- Interest rates and fee schedules

- Contact information for each creditor

Keep physical or digital copies of all loan documents, payment receipts, and correspondence with lenders. This documentation protects you in case of disputes and helps you track your progress toward debt freedom.

Credit Building Opportunities Through Responsible Borrowing

Personal loans with no bank account can still contribute to building or rebuilding your credit history. Most reputable lenders report payment activity to the three major credit bureaus: Experian, Equifax, and TransUnion.

Maximizing Credit-Building Benefits

Making consistent on-time payments demonstrates financial responsibility to future lenders. Even if your current loan carries higher interest rates due to lack of a bank account, establishing a positive payment history opens doors to better financing terms later.

Request verification that your lender reports to credit bureaus before finalizing your loan agreement. Some smaller lenders or alternative financial service providers may not report activity, limiting your opportunity to build credit through the loan.

Accessing personal loans with no bank account requires more preparation and documentation than traditional borrowing, but viable options exist for consumers who need financing outside conventional banking channels. By understanding available loan types, preparing thorough documentation, and selecting reputable lenders, you can secure the funding you need while protecting yourself from predatory practices. Standard Financial specializes in working with borrowers facing unique financial situations, offering flexible personal loan options across Louisiana, Mississippi, Tennessee, and Georgia, including solutions for customers without traditional bank accounts. Visit a branch office near you to explore personalized financing options tailored to your specific circumstances.

No comment yet, add your voice below!