The gig economy has transformed how millions of Americans earn their living, with platforms like Uber, DoorDash, Upwork, and TaskRabbit creating unprecedented flexibility. However, this freedom comes with financial challenges, particularly when seeking traditional financing. Banks and lenders have historically relied on W-2 forms and steady paychecks to evaluate creditworthiness, leaving independent contractors at a disadvantage. Understanding how to navigate the lending landscape as a gig worker can unlock access to capital for emergencies, business investments, or personal needs.

Understanding the Unique Financial Position of Gig Workers

Gig workers face distinct challenges when applying for financing. Traditional employment verification doesn't exist in the same format, making standard loan applications difficult to complete. Your income fluctuates monthly, sometimes dramatically, based on demand, platform algorithms, and personal availability.

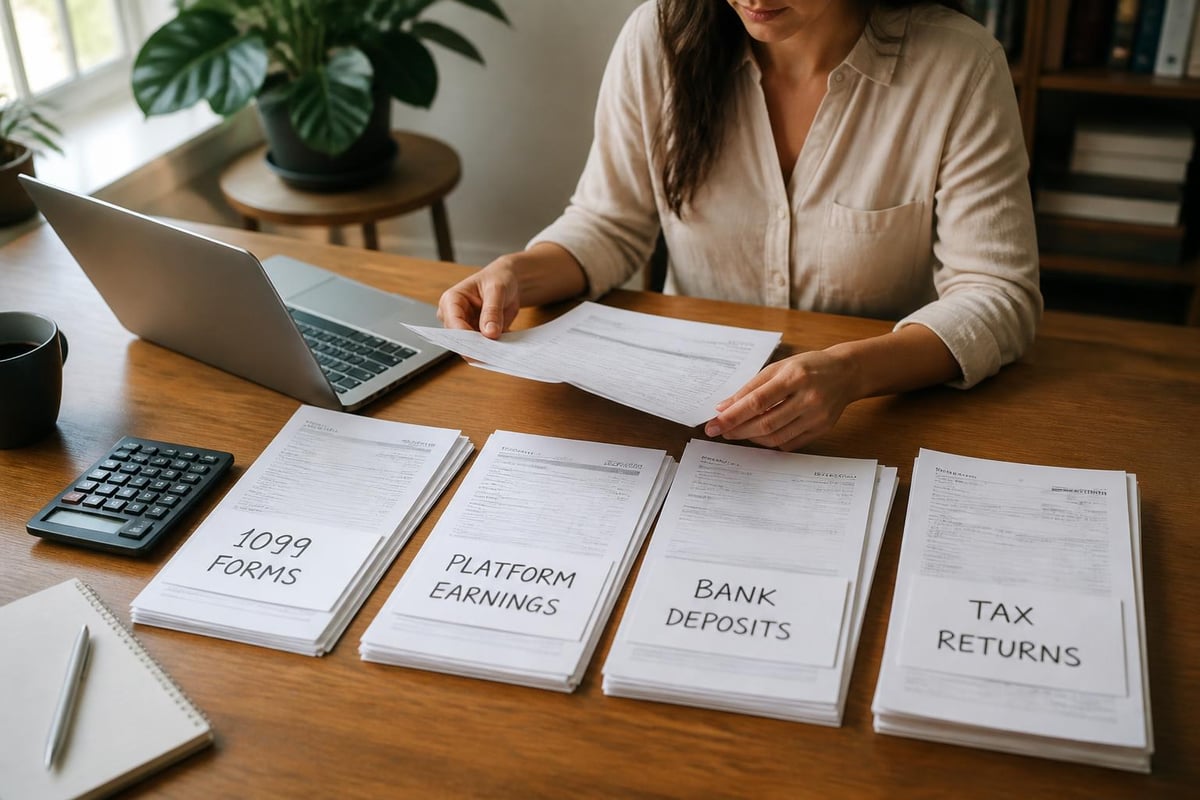

Financial institutions have adapted slowly to this shift in the workforce. Many lenders still require pay stubs from the past 60 days or employer contact information. For someone earning through multiple platforms, assembling documentation becomes a complex puzzle of 1099 forms, platform earnings statements, and bank deposit records.

Income Documentation Strategies

Successful loan applications start with organized financial records. Maintain detailed spreadsheets tracking your monthly earnings from each platform. Download monthly statements from all gig platforms you use, as these provide official documentation of your income streams.

Essential documents for gig worker loan applications include:

- 1099-NEC or 1099-K forms from the previous tax year

- Bank statements showing consistent deposits from gig platforms

- Platform-specific earnings reports (most apps provide monthly summaries)

- Tax returns for the past two years

- Profit and loss statements if you track business expenses

Creating a professional income verification package strengthens your application significantly. Consider preparing a one-page summary showing your average monthly earnings, calculated over 6-12 months, to demonstrate income consistency despite normal fluctuations.

Types of Loans Available to Independent Contractors

The lending market has evolved to accommodate non-traditional workers. While loans for gig workers were once nearly impossible to obtain, multiple options now exist with varying terms, requirements, and approval processes.

Personal Loans from Traditional Lenders

Personal loans remain the most versatile option for gig workers needing substantial funds. These unsecured loans typically range from $1,000 to $50,000 with repayment terms between one and seven years. Interest rates vary based on credit scores, income verification, and lender policies.

Traditional banks have become more flexible, though credit unions often provide better terms for members with non-traditional income. Some institutions now accept platform earnings statements as official income verification, particularly if supported by consistent bank deposits over several months.

Alternative Lending Options

The fintech revolution has created specialized lenders focusing specifically on gig economy workers. These platforms understand variable income patterns and evaluate applications differently than traditional banks. Alternative lenders for gig workers consider factors like platform ratings, completed gigs, and earning trends rather than solely examining tax returns.

| Loan Type | Typical Amount | Approval Speed | Documentation Required |

|---|---|---|---|

| Personal Loan | $1,000-$50,000 | 2-7 days | Tax returns, bank statements, ID |

| Payday Alternative | $200-$1,000 | Same day | Bank account, ID, income proof |

| Cash Advance | $100-$5,000 | Within hours | Platform earnings access |

| Line of Credit | $500-$25,000 | 1-5 days | Credit history, income verification |

Merchant Cash Advances and Specialized Products

Some platforms offer cash advances specifically designed for gig workers. These products provide quick access to funds based on your average platform earnings, with repayment structured as a percentage of future earnings rather than fixed monthly payments.

This flexibility accommodates the reality of variable income. During slower months, you pay less. During busy periods, the repayment accelerates. While convenient, carefully review the effective interest rates, as they can be substantially higher than traditional personal loans.

Qualification Requirements and Approval Factors

Securing loans for gig workers requires understanding how lenders evaluate non-traditional income. The approval process differs significantly from standard employment situations, focusing on different metrics and documentation standards.

Credit Score Considerations

Your credit score remains crucial regardless of employment type. Most lenders prefer scores above 580 for approval, though better rates require scores exceeding 670. Gig workers with excellent credit (720+) often qualify for terms comparable to traditionally employed borrowers.

However, some specialized lenders prioritize income verification and bank account activity over credit scores. This creates opportunities for workers rebuilding credit or new to the credit system. Demonstrating consistent earnings over six months can offset a lower credit score in many cases.

Income Stability Metrics

Lenders evaluate income stability differently for independent contractors. Rather than verifying employment duration with a single employer, they examine:

Key income evaluation factors:

- Average monthly earnings over the past 6-12 months

- Consistency of deposits from gig platforms

- Diversification across multiple income sources

- Upward or downward earning trends

- Seasonal variations in your specific gig type

Demonstrating multiple income streams actually strengthens applications. A rideshare driver who also does food delivery and occasional freelance work shows income diversification that reduces risk from any single platform's algorithm changes or market shifts.

Debt-to-Income Ratio Calculations

Lenders calculate your debt-to-income ratio by dividing monthly debt obligations by monthly gross income. For gig workers, determining "monthly income" requires averaging earnings over several months. Most lenders use a 6-12 month average to smooth out natural fluctuations.

Target a debt-to-income ratio below 43% for optimal approval odds. If your average monthly earnings total $4,000, monthly debt payments should stay under $1,720. This includes existing credit cards, auto loans, student loans, and the potential new loan payment.

Strategies for Improving Loan Approval Odds

Gig workers can take specific steps to strengthen loan applications and secure better terms. Preparation and strategic timing make substantial differences in both approval likelihood and interest rates offered.

Building a Strong Financial Profile

Establish and maintain a dedicated business checking account for gig income. This separation simplifies income documentation and demonstrates financial organization to lenders. Consistent deposits into a single account create a clear earnings pattern that underwriters appreciate.

Maintain at least six months of operating expenses in savings before applying for non-essential loans. This emergency fund demonstrates financial stability and reduces lender risk perception. While challenging with variable income, this cushion also protects you during slower earning periods.

Timing Your Application Strategically

Apply for loans for gig workers during your peak earning season when recent months show higher-than-average income. If you drive rideshare primarily during summer tourism, apply in August or September when your three-month average reflects strong earnings.

Avoid applications immediately after slow months or seasonal dips. Wait until you've accumulated 2-3 months of solid earnings that bring your average up to typical levels. This patience can mean the difference between approval and rejection or significantly impact your interest rate.

Working with Co-Signers or Co-Borrowers

A co-signer with traditional employment and strong credit can dramatically improve approval odds and loan terms. This person agrees to repay the loan if you default, reducing lender risk. Family members often serve this role, though they should understand the serious financial commitment involved.

Alternatively, a co-borrower with steady W-2 income can combine their employment verification with your gig earnings to meet income requirements. This approach works well for married couples or partners where one works traditionally and the other independently.

Managing Loan Repayment with Variable Income

Successfully repaying loans requires different strategies when income fluctuates monthly. Planning for variability prevents missed payments and protects your credit score throughout the loan term.

Creating a Variable Income Budget

Structure your budget around your lowest-earning months rather than your average. If your income ranges from $2,500 to $6,000 monthly, budget based on $2,500. Allocate surplus earnings from better months into a designated loan payment account.

This reserve account smooths income fluctuations, ensuring you can make payments during inevitable slow periods. Treat deposits into this account as non-negotiable expenses during high-earning months, building a buffer that protects your payment history.

Monthly budgeting priorities for gig workers with loans:

- Essential expenses (housing, utilities, food, insurance)

- Loan payment plus one extra payment buffer

- Emergency fund contribution (target 6 months expenses)

- Business expenses (vehicle maintenance, equipment, platform fees)

- Discretionary spending from remaining funds

Automated Payment Systems

Set up automatic payments from your reserve account on your loan due date. This automation eliminates the risk of forgotten payments while you focus on earning. Most lenders offer small interest rate discounts (typically 0.25%) for enrolling in autopay.

Monitor your reserve account balance weekly to ensure sufficient funds. If a particularly slow month depletes the buffer, prioritize rebuilding it immediately when earnings recover. This system requires discipline but provides stability that protects your credit.

Regional Considerations for Southeastern Gig Workers

Gig workers in Louisiana, Mississippi, Tennessee, and Georgia face unique regional factors affecting their financing needs and opportunities. Understanding local market conditions helps optimize your approach to securing loans for gig workers in these states.

Market-Specific Opportunities

The Southeast has experienced significant gig economy growth, particularly in metropolitan areas like New Orleans, Memphis, Nashville, Atlanta, and Jackson. Tourist destinations create seasonal earning opportunities that impact income documentation strategies. If you work in tourism-heavy areas, lenders familiar with regional patterns may better understand your seasonal fluctuations.

Local credit unions in these states often provide more flexible terms than national banks. They understand regional economic patterns and may offer specialized products for independent contractors. Membership requirements vary, but many allow anyone living or working in specific counties to join.

State-Specific Lending Regulations

Interest rate caps and lending regulations differ across southeastern states. Louisiana, Mississippi, Tennessee, and Georgia each maintain different maximum allowable interest rates for various loan types. These regulations protect borrowers but also influence which lenders operate in each state.

| State | Max Interest Rate (Personal Loans) | Notable Regulations |

|---|---|---|

| Louisiana | 36% APR (small loans) | Licensing requirements for lenders |

| Mississippi | No statutory limit | Fewer consumer protections |

| Tennessee | 24% simple interest | Cap varies by loan amount |

| Georgia | Varies by loan type | Strict payday lending restrictions |

Understanding your state's protections helps evaluate whether loan terms comply with local law and represent fair market rates.

Alternative Financial Solutions Beyond Traditional Loans

While loans provide immediate capital access, gig workers should explore complementary financial tools that support income stability and reduce borrowing needs over time.

Platform-Specific Advances

Many gig platforms now offer built-in cash advance features. Uber, DoorDash, and Instacart provide same-day or instant pay options, allowing you to access earnings immediately rather than waiting for weekly deposits. While these typically charge small fees ($0.50-$2.99 per transfer), they provide emergency cash without formal loan applications.

Some platforms have partnered with financial service companies to offer specialized cash advances for gig workers based on your earning history with that specific platform. These products often feature lower rates than traditional payday loans while offering faster approval than conventional personal loans.

Income Smoothing Tools

Several fintech apps help gig workers manage variable income through automated savings and income prediction. These tools analyze your earning patterns, predict upcoming slow periods, and automatically set aside funds during high-earning weeks to cover expenses during lower-earning times.

While not loans themselves, these services reduce the need for emergency borrowing by creating self-funded buffers. Some integrate directly with gig platforms, pulling earning data automatically to provide accurate predictions and recommendations.

Building Long-Term Financial Stability

Accessing loans for gig workers solves immediate needs, but sustainable financial health requires strategic planning that accounts for income variability and prepares for future opportunities.

Establishing Business Credit

Separate your personal and business finances completely. Apply for a business credit card using your gig work as a sole proprietorship. Use this card exclusively for business expenses like vehicle maintenance, equipment purchases, or platform fees.

Building business credit creates additional financing options beyond personal loans. After 12-24 months of responsible business credit card use, you may qualify for business lines of credit with higher limits and more favorable terms than personal products.

Tax Planning for Better Loan Qualification

Work with a tax professional familiar with gig economy workers. Proper tax planning maximizes legitimate deductions while maintaining sufficient reported income for loan qualification. Balance reducing tax liability with demonstrating strong earnings for future financing needs.

Quarterly estimated tax payments, while painful in the moment, prevent year-end tax surprises that could require emergency loans. They also demonstrate financial organization and planning ability to lenders reviewing your tax returns during the application process.

Diversification and Income Growth

Strategically expand your gig portfolio to reduce platform dependence and increase total earnings. Research which combinations work well together. Rideshare and food delivery pair naturally with overlapping availability. Freelance services like writing, design, or consulting can fill gaps between active gigs.

Higher total income improves loan qualification and provides more financial cushion for unexpected expenses or slower periods. Document all income sources consistently to present a complete financial picture when applying for financing.

Navigating the lending landscape as a gig worker requires understanding how your unique income situation affects approval odds and knowing which documentation strengthens your application. Whether you need funds for a vehicle repair, medical expense, home improvement, or educational opportunity, options exist even with variable earnings and non-traditional employment. Standard Financial understands the challenges faced by independent contractors and offers flexible personal loan solutions across Louisiana, Mississippi, Tennessee, and Georgia, working with clients to find financing options that accommodate their unique financial situations, even when past credit issues are a concern.

No comment yet, add your voice below!