Navigating the financial landscape with less-than-perfect credit can feel overwhelming, but understanding your options is the first step toward financial stability. Subprime personal loans serve millions of Americans who need access to credit but don't qualify for traditional prime lending products. These specialized financial tools provide opportunities for individuals with credit scores below 670 to secure funding for essential expenses, emergencies, and opportunities that can't wait for credit repair. While they come with higher costs, subprime personal loans can be valuable resources when used strategically and obtained from reputable lenders who prioritize transparency and responsible lending practices.

Understanding Subprime Personal Loans

Subprime personal loans are credit products designed specifically for borrowers who fall outside the traditional prime lending criteria. These loans typically serve individuals with credit scores ranging from 300 to 669, though exact thresholds vary by lender. The term "subprime" simply indicates that the borrower presents higher risk based on credit history, not their worth as a person or their potential for financial recovery.

Key Characteristics of Subprime Lending

The defining features of subprime personal loans set them apart from conventional financing:

- Higher interest rates reflecting increased lender risk

- Smaller loan amounts to minimize exposure

- Shorter repayment terms in many cases

- More flexible qualification criteria beyond just credit scores

- Potentially higher fees including origination and prepayment penalties

Financial institutions offering these products must carefully balance risk management with the mission of providing access to credit for underserved populations. Regulatory guidance on subprime lending helps ensure lenders maintain sound practices while serving this market segment.

Who Qualifies for Subprime Personal Loans

Qualification extends beyond simple credit score thresholds. Lenders evaluate multiple factors to determine both eligibility and loan terms for applicants seeking subprime personal loans.

Common Borrower Profiles

Several situations may lead qualified individuals to seek subprime financing options:

- Limited credit history – young adults or immigrants new to credit

- Past financial hardships – bankruptcy, foreclosure, or repossession

- Medical debt collections impacting credit reports

- High credit utilization from maxed-out credit cards

- Recent missed payments or charge-offs

- Thin credit files with few tradelines

The southeastern United States, including Louisiana, Mississippi, Tennessee, and Georgia, has seen particular growth in subprime lending as financial institutions recognize the need to serve diverse communities with varying credit profiles. Many borrowers in these regions use subprime personal loans for essential purposes like home repairs after storm damage, medical expenses, or education costs.

Application Requirements

While credit standards are more flexible, lenders still require documentation to assess ability to repay:

| Document Type | Purpose | Examples |

|---|---|---|

| Income Verification | Confirm repayment capacity | Pay stubs, tax returns, bank statements |

| Identity Proof | Prevent fraud | Driver's license, passport, state ID |

| Residence Verification | Establish stability | Utility bills, lease agreement, mortgage statement |

| Employment Confirmation | Assess job security | Employer letter, recent pay stubs |

Most lenders require minimum income thresholds and evaluate debt-to-income ratios to ensure borrowers can manage new payment obligations alongside existing financial responsibilities.

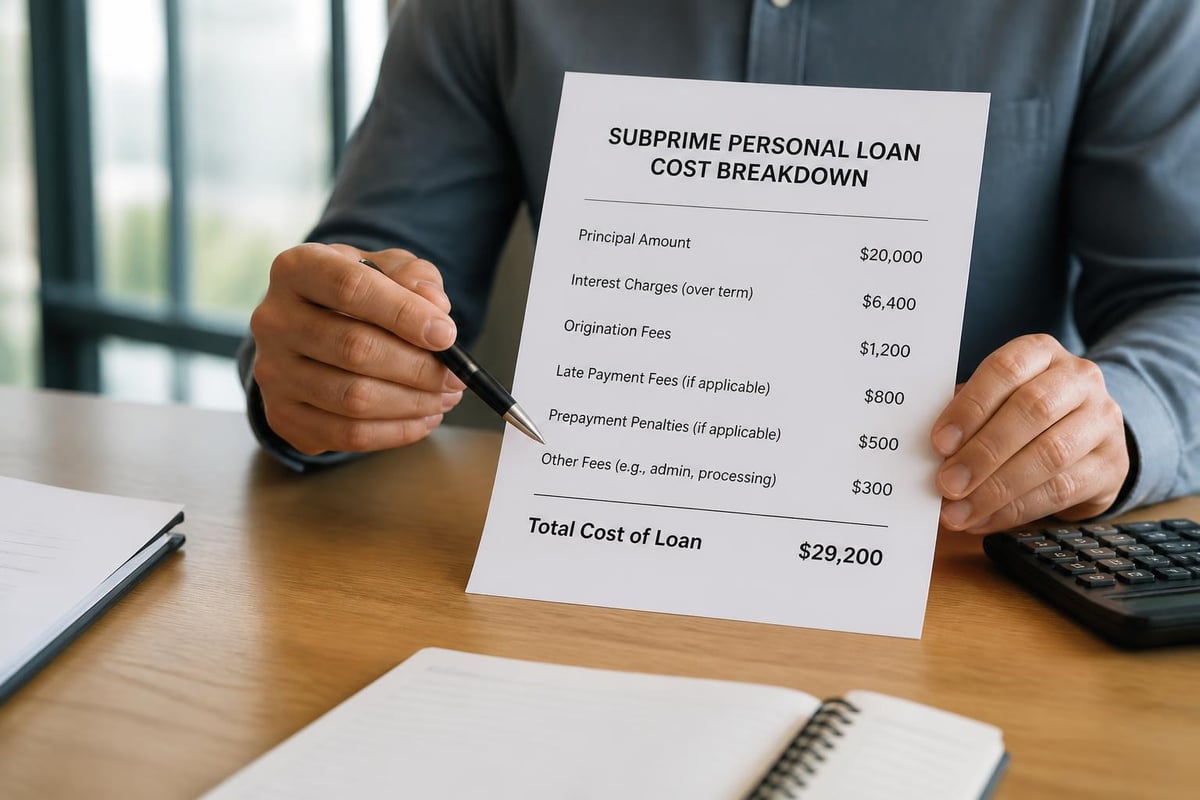

Interest Rates and Terms Explained

The cost structure of subprime personal loans differs significantly from prime lending products. Understanding these differences helps borrowers make informed decisions and avoid predatory lending situations.

APR Ranges in 2026

Annual percentage rates for subprime personal loans typically fall within specific ranges based on credit quality and lender type. Traditional banks usually charge between 18% and 35% APR for subprime borrowers, while online lenders may range from 25% to 36%. Credit unions often provide the most competitive rates, sometimes as low as 12% to 28% for members with subprime credit.

The impact of subprime loans on credit scores depends largely on payment behavior rather than the loan type itself. Consistent on-time payments can actually help rebuild credit over time, making the higher initial cost a worthwhile investment in financial future.

Fee Structures

Beyond interest rates, various fees add to the total cost of borrowing:

- Origination fees ranging from 1% to 8% of loan amount

- Late payment penalties typically $15 to $50 per occurrence

- Prepayment penalties on some contracts (though increasingly rare)

- Insufficient funds fees if payments bounce

- Document fees for processing and administration

Comparing Loan Options and Lenders

Not all subprime personal loans are created equal. Borrowers benefit from understanding the landscape of available options and how to identify reputable lenders.

Types of Subprime Lenders

Three primary categories serve the subprime market, each with distinct characteristics:

Traditional Banks and Credit Unions typically offer the most competitive terms for subprime borrowers who meet their criteria. They maintain physical branches, provide relationship banking, and often have more flexibility in underwriting decisions. Credit unions particularly excel at working with members who have credit challenges.

Online Lenders provide quick application processes and funding, often within 24 to 48 hours. They use alternative data and automated underwriting systems to evaluate applications. While convenient, borrowers should carefully review terms as rates and fees can be higher than traditional institutions.

Finance Companies specialize in subprime lending and understand the unique needs of this market. These lenders often have multiple branch locations in communities they serve, offering personalized service and flexible financing plans for various purposes including home improvements, medical expenses, and education costs.

Red Flags to Avoid

Protecting yourself from predatory lending requires vigilance:

- Guaranteed approval claims regardless of credit

- Pressure tactics to sign immediately

- Unclear terms or refusal to provide written documentation

- Triple-digit APRs exceeding state usury limits

- Advance fee requests before loan approval

- Balloon payments that create refinancing traps

Legitimate lenders comply with state and federal regulations, clearly disclose all terms, and provide borrowers time to review contracts before signing. The legal definition of subprime loans helps establish baseline understanding of these financial products.

Strategic Uses for Subprime Personal Loans

When obtained from reputable sources and used wisely, subprime personal loans can serve important financial needs and even contribute to credit improvement.

Appropriate Borrowing Purposes

The most effective uses align with improving financial stability or addressing essential needs:

| Purpose | Benefits | Considerations |

|---|---|---|

| Emergency Expenses | Avoid worse alternatives like payday loans | Ensure genuine emergency, not discretionary spending |

| Medical Bills | Prevent collections, negotiate payment plans | Compare with hospital payment programs |

| Home Repairs | Maintain property value and safety | Get multiple contractor quotes first |

| Debt Consolidation | Simplify payments, potentially lower total interest | Requires discipline to avoid new debt |

| Education Costs | Investment in earning potential | Consider federal student loans first |

| Vehicle Repairs | Maintain transportation for work | Verify repair necessity and cost reasonableness |

Borrowers in the southeastern states often face specific challenges that make subprime personal loans particularly valuable. Hurricane preparedness and recovery, aging housing stock requiring repairs, and medical expenses in states with limited Medicaid expansion create legitimate financing needs that these products can address.

Credit Building Strategy

Using subprime personal loans strategically can accelerate credit improvement:

- Make payments early or on time every month without exception

- Set up automatic payments to prevent missed due dates

- Keep loan accounts open for the full term to build payment history

- Avoid applying for multiple loans simultaneously to minimize hard inquiries

- Monitor credit reports quarterly to track progress and dispute errors

The compound effect of consistent positive payment history typically produces noticeable credit score improvements within 6 to 12 months, potentially qualifying borrowers for better terms on future financing needs.

Application Process and Approval Timeline

Understanding what to expect during the application journey helps borrowers prepare properly and avoid unnecessary delays.

Step-by-Step Application

The process follows a generally consistent pattern across most lenders:

- Research and comparison – Evaluate multiple lenders for best terms

- Pre-qualification – Check rates without hard credit inquiry (when available)

- Formal application – Submit complete information and documentation

- Underwriting review – Lender evaluates risk and determines approval

- Offer review – Examine loan terms, APR, fees, and payment schedule

- Contract signing – Read carefully and sign if acceptable

- Funding – Receive proceeds via direct deposit or check

Traditional lenders may require in-person visits to branch offices for final document signing, while online lenders typically complete the entire process digitally. Borrowers should expect the full process to take anywhere from same-day approval for online lenders to several business days for traditional institutions.

Documentation Preparation Tips

Being prepared accelerates approval and demonstrates financial responsibility:

- Gather recent pay stubs covering at least 30 days

- Prepare tax returns from the previous year

- Compile bank statements showing income deposits and spending patterns

- List current debts with creditor names, balances, and monthly payments

- Document residence history for the past two years

- Have references available if required by lender

Complete and accurate applications process faster and receive better consideration than those requiring multiple follow-up requests for missing information.

Managing Your Subprime Personal Loan

Successfully navigating repayment requires planning, discipline, and proactive communication with your lender.

Payment Best Practices

Establishing strong payment habits from day one protects your credit and financial wellbeing:

- Create a dedicated loan payment fund separate from general checking

- Schedule payments for right after payday when funds are available

- Pay more than the minimum when possible to reduce total interest

- Contact your lender immediately if payment difficulties arise

- Track your loan balance monthly to monitor progress

Many borrowers find success with biweekly payment strategies that result in one extra payment annually, significantly reducing interest costs over the loan term. Understanding installment loan mechanics helps borrowers optimize their repayment approach.

Refinancing Opportunities

As credit improves, refinancing becomes a powerful tool for reducing costs:

When to Consider Refinancing:

- Credit score has increased by 50+ points

- Income has significantly improved

- At least 6-12 months of perfect payment history established

- Current interest rates have decreased

- Debt-to-income ratio has improved substantially

Borrowers who successfully rebuild credit through responsible subprime personal loan management often qualify for prime lending products within 18 to 24 months, creating opportunities to refinance at dramatically lower rates and save thousands in interest charges.

Regional Considerations for Southern Borrowers

The unique economic and regulatory landscape of Louisiana, Mississippi, Tennessee, and Georgia creates specific factors that subprime borrowers should understand.

State Regulatory Differences

Each state maintains distinct lending regulations that affect loan availability and terms:

| State | Maximum APR | Key Regulations | Consumer Protections |

|---|---|---|---|

| Louisiana | 36% for small loans | License requirements for lenders | Cooling-off periods |

| Mississippi | 36% standard cap | Deferred presentment regulations | Database monitoring |

| Tennessee | 24% for installment loans | Size restrictions on certain loans | Disclosure requirements |

| Georgia | 60% maximum (varies by type) | Industrial Loan Act provisions | Anti-predatory measures |

These variations mean that identical borrowers may receive different offers depending on their state of residence. Working with lenders who maintain physical presence across multiple states often provides advantages in terms of understanding regional nuances and offering appropriate products.

Economic Factors Affecting Borrowing

Regional economic conditions influence both the need for and availability of subprime personal loans. The southeastern states have experienced diverse economic trajectories, with urban areas showing strong growth while rural communities face ongoing challenges. Natural disaster recovery remains a periodic consideration, particularly in coastal Louisiana and Mississippi where hurricane preparation and rebuilding create cyclical financing needs.

Employment stability varies significantly by industry and location, making lender familiarity with local economic conditions valuable when underwriting decisions consider factors beyond simple credit scores.

Alternative and Complementary Options

Subprime personal loans represent one tool in a broader financial toolkit. Exploring alternatives and complementary strategies ensures optimal financial decision-making.

Other Financing Paths

Several alternatives merit consideration depending on specific circumstances:

- Credit union membership for access to share-secured loans

- Family loans with formal written agreements

- Payment plans directly with service providers

- Credit builder loans specifically designed for score improvement

- Secured personal loans using savings or assets as collateral

- Nonprofit lending programs serving specific communities or purposes

Each option presents distinct advantages and limitations. Credit union loans typically offer the best combination of reasonable rates and flexible underwriting for members with credit challenges, while family loans eliminate interest costs but risk damaging relationships if not managed properly.

Building Long-Term Financial Health

Subprime personal loans work best as part of comprehensive financial improvement strategy:

- Create realistic budgets tracking all income and expenses

- Build emergency savings even if starting with $25 monthly

- Address root causes of credit challenges to prevent recurrence

- Seek financial counseling from nonprofit agencies when needed

- Educate yourself on credit, budgeting, and money management

- Set specific goals for credit score targets and timelines

The historical context of subprime lending reveals both its potential benefits and risks. Learning from past lending crises while recognizing the legitimate need for credit access helps borrowers make informed decisions that serve their long-term interests rather than creating additional financial burdens.

Subprime personal loans provide essential financial access for millions of Americans working to overcome credit challenges and achieve their goals. Understanding how these products work, what they cost, and how to use them strategically enables borrowers to make confident decisions that improve rather than harm their financial futures. If you're facing credit challenges but need financing for home improvements, medical expenses, education, or other important needs, Standard Financial offers flexible financing plans with transparent terms at branch locations throughout Louisiana, Mississippi, Tennessee, and Georgia, helping clients build better financial futures regardless of past credit issues.

No comment yet, add your voice below!