When unexpected expenses arise or financial emergencies demand immediate attention, consumers often face critical decisions about borrowing options. The choice between different loan products can significantly impact your financial health for months or even years to come. Two common short-term borrowing solutions-installment loans and payday loans-serve different purposes and carry vastly different terms, costs, and consequences. Understanding the installment loan vs payday loan debate becomes essential for anyone seeking to navigate consumer lending responsibly, particularly for residents across Louisiana, Mississippi, Tennessee, and Georgia who need access to fast funding without compromising their long-term financial stability.

Understanding Installment Loans

Installment loans represent a traditional borrowing structure where consumers receive a lump sum upfront and repay it through scheduled payments over a predetermined period. These loans typically range from several months to several years, depending on the amount borrowed and the lender's terms.

How Installment Loans Work

The mechanics of installment loans follow a straightforward pattern. Borrowers apply for a specific amount, undergo a credit evaluation, and if approved, receive funds deposited into their bank account. What is an installment loan encompasses various types including personal loans, auto loans, and mortgages, all sharing the common feature of fixed payment schedules.

Key characteristics include:

- Fixed monthly payment amounts

- Predetermined repayment timeline

- Interest rates that remain constant or vary based on market conditions

- Loan amounts typically ranging from $1,000 to $50,000 or more

- Credit reporting to major bureaus affecting credit scores

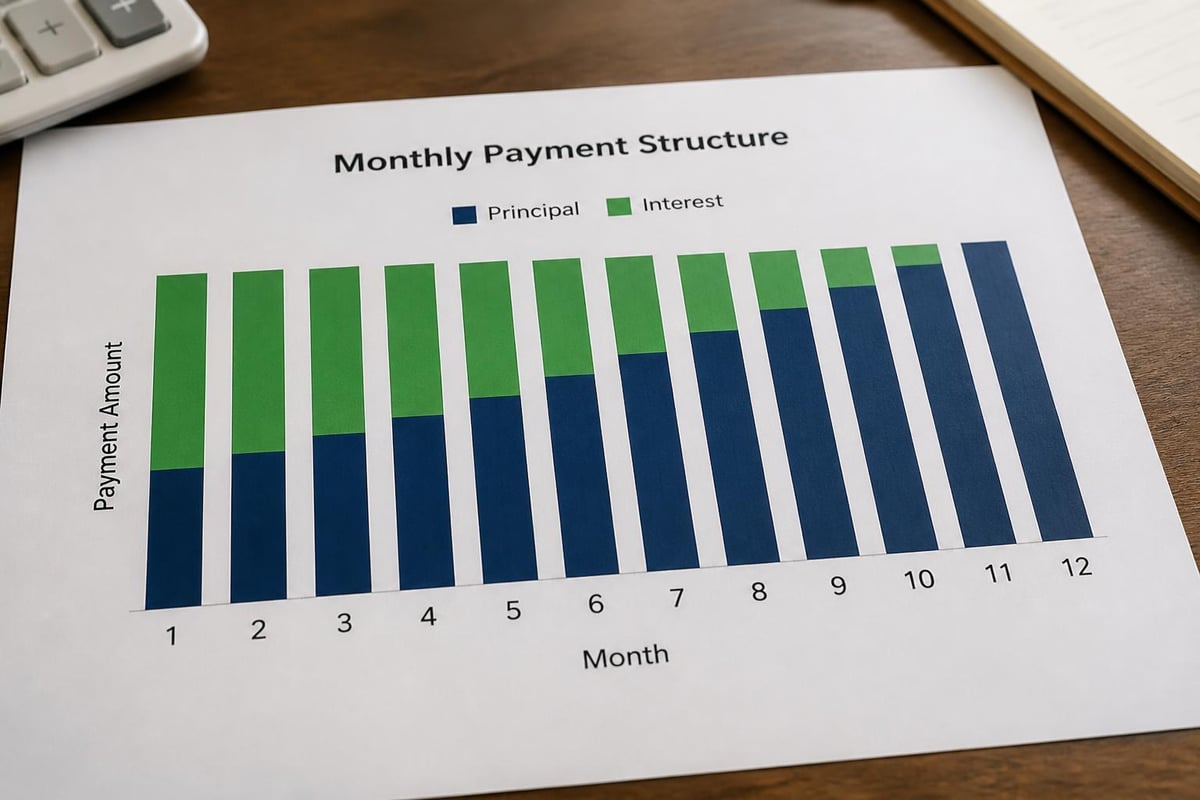

The payment structure creates predictability. Borrowers know exactly how much they owe each month, making budgeting more manageable compared to other credit products.

Benefits of Installment Loans

Installment loans offer several advantages for consumers who need financing for home improvements, medical expenses, education costs, or debt consolidation. The extended repayment period means lower monthly obligations compared to short-term alternatives.

Primary advantages include:

- Manageable payments: Spreading costs over months reduces financial strain

- Credit building potential: On-time payments improve credit scores

- Larger borrowing amounts: Access to more substantial funds for significant expenses

- Competitive interest rates: Lower APRs compared to payday alternatives

- Refinancing options: Ability to restructure terms if circumstances change

For individuals with past credit issues, installment loans from consumer lending specialists provide pathways to financial solutions while rebuilding creditworthiness. The structured approach encourages disciplined repayment habits.

Understanding Payday Loans

Payday loans operate on an entirely different model designed for immediate, short-term cash needs. These loans typically require repayment by the borrower's next payday, usually within two to four weeks of borrowing.

The appeal lies in accessibility and speed. Payday lenders often require minimal documentation, no credit checks, and can provide funds within hours. However, this convenience comes at a steep cost.

Payday Loan Structure

The typical payday loan process involves borrowing a small amount-usually between $100 and $1,000-and providing the lender with a post-dated check or authorization to electronically withdraw funds from your bank account on your next payday.

| Feature | Payday Loan Characteristics |

|---|---|

| Loan Amount | $100 – $1,000 |

| Repayment Term | 2 – 4 weeks |

| Typical Fee | $15 – $30 per $100 borrowed |

| Effective APR | 300% – 600% or higher |

| Credit Check | Usually none required |

| Credit Reporting | Rarely reported unless defaulted |

The legal distinctions between payday loans and installment loans highlight fundamental differences in how these products are regulated and structured under state and federal law.

The Payday Loan Trap

Many borrowers find themselves in a debt cycle because the entire loan amount plus fees becomes due on a single date. When borrowers cannot repay the full amount, they often roll over the loan, paying additional fees while the principal remains unchanged.

Research indicates that payday loans can exacerbate financial distress rather than provide sustainable solutions. The high-cost structure makes these loans particularly problematic for consumers already facing financial vulnerability.

Installment Loan vs Payday Loan: Direct Comparison

Examining the installment loan vs payday loan question requires looking beyond surface-level differences to understand how each product affects borrowers' financial lives.

Cost Analysis

The most striking difference between these lending products centers on cost. While installment loans charge interest over time, the total cost often remains substantially lower than payday loan fees.

Cost comparison example:

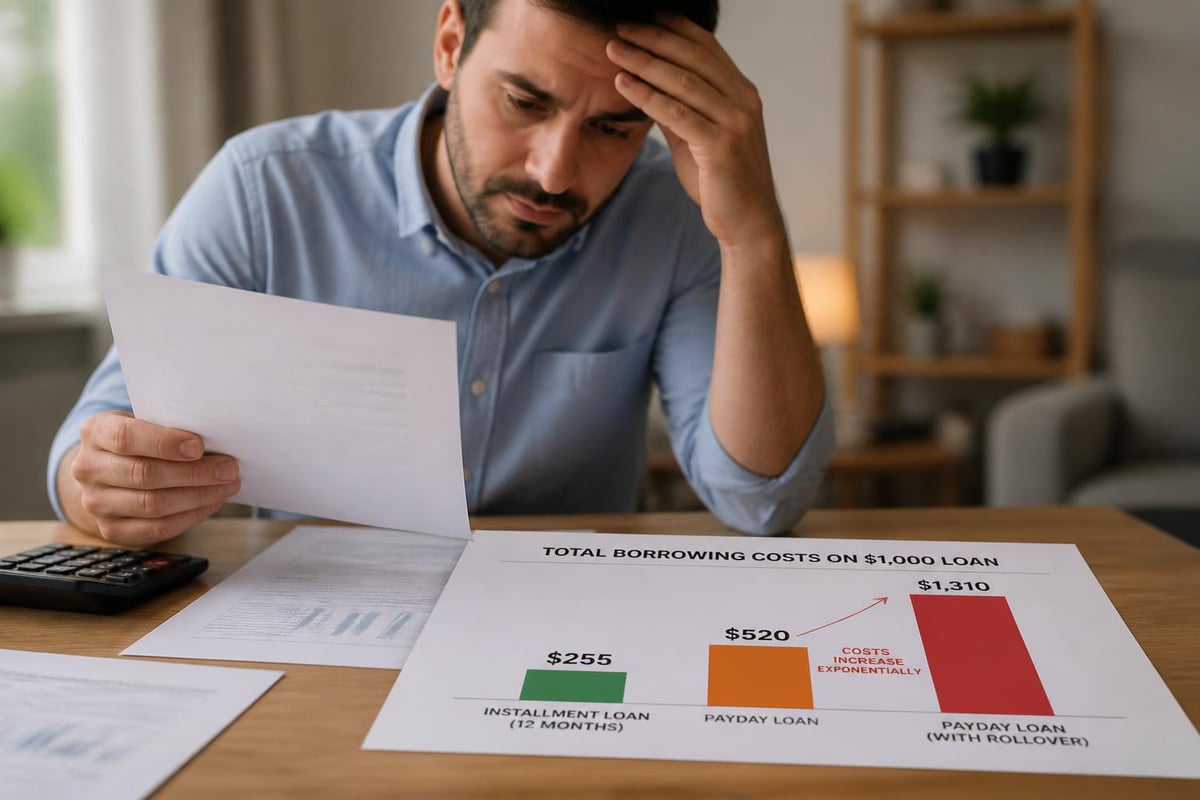

- $1,000 Installment Loan (12-month term, 25% APR): Total cost approximately $1,140

- $1,000 Payday Loan (2-week term, $15 per $100): Single payment of $1,150, but if rolled over just twice, total cost exceeds $1,450

The comparison of payday and installment loans demonstrates how seemingly small fees accumulate rapidly with payday products, especially when borrowers cannot repay on schedule.

Repayment Flexibility

Repayment structures represent another critical distinction in the installment loan vs payday loan analysis. Installment loans provide breathing room through extended terms, while payday loans demand immediate full repayment.

- Installment loans allow borrowers to absorb costs gradually

- Payday loans create pressure to repay everything at once

- Refinancing options exist for installment loans but rarely for payday products

- Payment flexibility accommodates changing financial circumstances with installment products

This flexibility proves especially valuable for individuals managing irregular income, unexpected expenses, or recovering from previous financial setbacks.

Credit Impact Differences

The impact on credit scores varies significantly between these borrowing options. Payday loan versus installment loan differences include how each product affects your credit profile and future borrowing capacity.

Installment loan credit effects:

- Positive payment history builds credit scores

- Diversifies credit mix, potentially improving scores

- Establishes track record for future lenders

- Creates opportunities for better rates on subsequent loans

Payday loan credit effects:

- Typically not reported to credit bureaus

- No credit-building benefits

- May appear on credit reports if sent to collections

- Can indicate financial distress to future lenders

For consumers seeking to establish or rebuild credit, installment loans offer strategic advantages that payday loans cannot match.

Regulatory Considerations

State regulations significantly impact the installment loan vs payday loan landscape, with varying restrictions across Louisiana, Mississippi, Tennessee, and Georgia. These regulations aim to protect consumers from predatory lending practices while maintaining access to credit.

State-Specific Rules

Each state implements different approaches to regulating short-term lending:

| State | Payday Loan Regulation | Installment Loan Regulation |

|---|---|---|

| Louisiana | Permitted with restrictions | Standard consumer protections |

| Mississippi | Permitted with fee caps | Licensed lender requirements |

| Tennessee | Permitted with regulations | Interest rate caps apply |

| Georgia | Effectively prohibited | Standard lending laws |

Understanding your state's specific requirements helps borrowers make informed decisions about which products are available and appropriately regulated.

Consumer Protection Laws

Federal and state laws provide various protections for borrowers. The Truth in Lending Act requires lenders to disclose all terms, fees, and annual percentage rates before finalizing any loan agreement.

Important protections include:

- Clear disclosure of all costs and terms

- Prohibition against certain collection practices

- Rights to dispute billing errors

- Protection from discrimination in lending

Studies examining interest rate caps on payday loans demonstrate how regulatory interventions can affect consumer access and welfare, highlighting the ongoing policy debates surrounding these lending products.

Making the Right Choice

Selecting between lending options requires honest assessment of your financial situation, repayment capacity, and long-term goals. The installment loan vs payday loan decision ultimately depends on individual circumstances.

When Installment Loans Make Sense

Installment loans prove ideal for planned expenses or situations where borrowers need substantial funds with manageable repayment terms. These products work best when you can commit to regular monthly payments over an extended period.

Optimal scenarios for installment loans:

- Home improvement projects with known costs

- Medical procedures or treatments not covered by insurance

- Educational expenses for career advancement

- Debt consolidation to reduce overall interest costs

- Major purchases requiring financing

The pros and cons of installment loans versus payday loans reveal how installment products align with structured financial planning and responsible borrowing practices.

Warning Signs You're Considering the Wrong Option

Certain circumstances suggest a borrowing product may create more problems than it solves. Recognizing these warning signs helps prevent financial mistakes.

Red flags include:

- Needing a loan to pay off another loan

- Unable to cover basic living expenses without borrowing

- Considering rolling over or extending short-term loans

- Borrowing without clear repayment plan

- Ignoring loan terms and total costs

Alternative Solutions

Before committing to either option in the installment loan vs payday loan comparison, consider alternatives that might better serve your financial needs.

Emergency Fund Building

Creating an emergency savings fund eliminates the need for many short-term loans. Even small regular deposits accumulate over time, providing a financial cushion for unexpected expenses.

Credit Union Products

Credit unions often offer small-dollar loan programs specifically designed as alternatives to payday loans. These products feature lower interest rates and more favorable terms than commercial payday lenders.

Payment Plans

Many service providers, including medical facilities, utilities, and educational institutions, offer payment plans that allow you to spread costs without interest or fees. Always inquire about this option before seeking external financing.

Employer Advances

Some employers provide paycheck advances or emergency assistance programs for employees facing financial hardships. These arrangements typically involve minimal or no fees compared to commercial lending products.

Long-Term Financial Health

The installment loan vs payday loan decision extends beyond immediate cash needs to encompass long-term financial trajectory. Choosing products that support rather than undermine financial stability becomes essential for building wealth and security.

Building Credit for Future Opportunities

Establishing positive credit history through responsible installment loan use creates opportunities for better rates on mortgages, auto loans, and other major purchases. This strategic approach to borrowing pays dividends throughout your financial life.

Breaking the Debt Cycle

Many consumers trapped in payday loan cycles discover that transitioning to installment products provides the first step toward financial freedom. The structured repayment schedule and lower costs make sustainable progress possible.

Financial Education Resources

Understanding personal finance fundamentals helps consumers make better decisions across all aspects of money management. Numerous free resources provide guidance on budgeting, saving, and responsible borrowing.

The installment loan vs payday loan comparison reveals fundamental differences in cost, structure, and impact on your financial future. Understanding these distinctions empowers you to choose borrowing solutions that align with your needs while protecting your long-term financial health. Whether you need funding for home improvements, medical expenses, education, or unexpected emergencies, Standard Financial offers flexible installment loan options with transparent terms and competitive rates across Louisiana, Mississippi, Tennessee, and Georgia. Our experienced team works with clients from all credit backgrounds to find financing solutions that support your goals without compromising your financial stability.

No comment yet, add your voice below!