Improving your credit score by 100 points may seem like a monumental task, but with the right strategies and commitment, it's entirely achievable. Whether you're looking to qualify for better loan terms, secure lower interest rates, or simply improve your financial standing, understanding how to raise your credit score 100 points can open doors to opportunities you might have thought were out of reach. The journey requires patience, discipline, and a comprehensive approach that addresses the key factors influencing your credit health. For individuals across Louisiana, Mississippi, Tennessee, and Georgia who have faced credit challenges, this improvement can be particularly transformative for accessing personal loans and financing options.

Understanding What Influences Your Credit Score

Before diving into specific strategies, you need to understand the five primary factors that determine your credit score. Payment history accounts for 35% of your FICO score, making it the most significant component. Even a single late payment can damage your score substantially, while consistent on-time payments demonstrate reliability to lenders.

Credit utilization represents 30% of your score and measures how much of your available credit you're actually using. Keeping this ratio below 30% is recommended, but maintaining it under 10% can yield even better results.

The remaining factors include length of credit history (15%), credit mix (10%), and new credit inquiries (10%). Each plays a role in your overall score, and addressing weaknesses across all categories creates the most substantial improvement.

The Time Factor in Credit Score Improvement

When considering how to raise your credit score 100 points, timing matters considerably. While overnight improvements are rare, strategic actions can produce visible results within weeks. Most significant increases occur over three to six months as positive behaviors compound and negative items age.

Understanding that credit score improvements typically take several months helps set realistic expectations. However, certain circumstances-such as correcting major reporting errors or paying off high-balance accounts-can trigger faster improvements.

Immediate Actions to Boost Your Credit Score

Check Your Credit Reports for Errors

Obtaining your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) is your first critical step. Federal law entitles you to one free report from each bureau annually through AnnualCreditReport.com.

Review each report meticulously for:

- Incorrect personal information

- Accounts that don't belong to you

- Duplicate accounts

- Incorrect payment statuses

- Outdated negative information (most items should disappear after seven years)

- Incorrect credit limits or balances

Disputing errors can yield quick results. If a creditor cannot verify disputed information within 30 days, they must remove it from your report. This single action has helped many consumers raise their scores significantly.

Pay Down High Credit Card Balances

Your credit utilization ratio exerts tremendous influence on your score. If you're carrying high balances relative to your credit limits, paying them down should be your top priority.

Strategic paydown approaches include:

- Avalanche method: Target cards with the highest utilization percentages first

- Snowball method: Pay off smallest balances completely to reduce the number of accounts with balances

- Balance distribution: Spread balances across multiple cards to keep individual utilization low

| Strategy | Best For | Primary Benefit |

|---|---|---|

| Avalanche | Maximum score impact | Reduces utilization ratios fastest |

| Snowball | Psychological motivation | Quick wins build momentum |

| Distribution | Multiple high-balance cards | Optimizes per-card utilization |

For example, if you have a $5,000 credit limit and a $4,500 balance, your utilization is 90%. Paying down $2,500 drops it to 40%, which can trigger immediate score improvements when your creditor reports to the bureaus.

Building Positive Payment History

Set Up Automatic Payments

Payment history is the single most important factor when learning how to raise your credit score 100 points. Missing even one payment can drop your score by 50 to 100 points, while establishing a consistent payment record builds trust with lenders.

Automatic payments eliminate the risk of forgetfulness. Set them up for at least the minimum payment on all revolving accounts. You can always make additional payments manually, but automation ensures you never miss a due date.

Request Higher Credit Limits

Increasing your available credit while maintaining the same balances instantly improves your utilization ratio. Contact your credit card issuers and request limit increases, especially if you've been a customer for over six months and have made consistent payments.

Many issuers conduct soft credit pulls for existing customers, which won't impact your score. A successful increase from $3,000 to $5,000 on a card with a $1,500 balance drops your utilization from 50% to 30% without paying a dollar extra.

Become an Authorized User

If you have a trusted family member or friend with excellent credit, becoming an authorized user on their account can boost your score. Their positive payment history and low utilization get reported to your credit file, potentially adding years of positive history instantly.

Requirements for maximum benefit:

- The primary cardholder must have a long history with the account

- The account must maintain low utilization

- The account must have perfect payment history

- The card issuer must report authorized users to credit bureaus

This strategy has helped many people increase their scores quickly, though it requires finding someone willing to extend this trust.

Managing Your Credit Mix and Accounts

Diversify Your Credit Portfolio

Lenders want to see you can manage different types of credit responsibly. While you shouldn't open accounts solely for diversification, maintaining a healthy mix of revolving credit (credit cards) and installment loans (auto loans, personal loans, mortgages) demonstrates financial maturity.

If your credit profile consists only of credit cards, a personal loan for debt consolidation or home improvements can add diversity. Conversely, if you only have installment loans, responsibly managing a credit card shows you can handle revolving credit.

Avoid Closing Old Credit Cards

Length of credit history contributes 15% of your score. Closing old accounts, especially your oldest ones, can hurt your score in two ways: it reduces your average account age and decreases your total available credit, raising your utilization ratio.

Keep old accounts active by using them occasionally for small purchases you pay off immediately. Even annual usage can prevent closure due to inactivity while preserving your credit history length.

Strategic Debt Management Approaches

Prioritize Collections and Charge-Offs

Outstanding collections and charge-offs severely damage your credit score. While raising your score by 100 points in a month is challenging, addressing these negative items can accelerate improvement.

Contact collection agencies to negotiate:

- Pay-for-delete agreements: The collector removes the item in exchange for payment

- Settlement offers: Pay less than the full amount owed

- Payment plans: Spread payments over time to manage cash flow

Always get agreements in writing before making payments. Once resolved, these items stop actively harming your score, though the history remains for seven years from the original delinquency date.

Consider Debt Consolidation

Consolidating multiple high-interest debts into a single personal loan can improve your credit score through several mechanisms. It reduces your credit card utilization to zero if you pay off revolving accounts, adds an installment loan to your credit mix, and simplifies payment management.

For residents of Louisiana, Mississippi, Tennessee, and Georgia dealing with past credit challenges, debt consolidation through consumer lending options can provide both immediate score benefits and long-term financial relief.

Monitoring and Maintaining Progress

Track Your Score Regularly

Many credit card issuers and financial institutions now offer free credit score monitoring. Take advantage of these tools to track your progress and identify what's working. Scores typically update monthly when creditors report new information.

Key metrics to monitor:

- Overall credit score trend

- Credit utilization percentage

- Number of on-time payments

- Average age of accounts

- Total number of hard inquiries

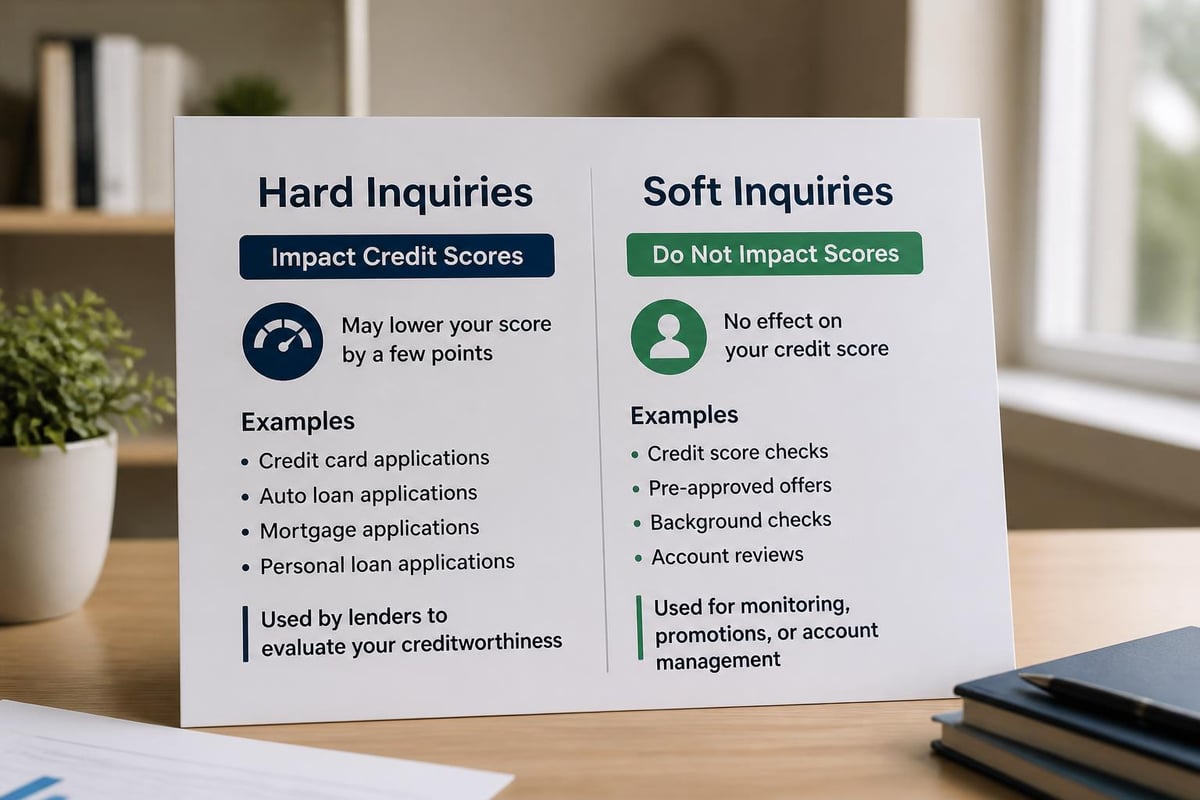

Understand Soft vs. Hard Inquiries

When you're working on how to raise your credit score 100 points, managing inquiries becomes important. Hard inquiries occur when you apply for credit and can lower your score by a few points. Multiple hard inquiries in a short period signal risk to lenders.

However, credit scoring models recognize rate shopping. Multiple inquiries for the same type of loan (mortgage, auto, student) within 14-45 days typically count as a single inquiry. Soft inquiries from checking your own score or pre-qualification offers don't affect your score at all.

Advanced Strategies for Accelerated Improvement

Utilize Credit Builder Loans

Credit builder loans are specifically designed to help people establish or rebuild credit. Unlike traditional loans where you receive money upfront, you make payments into a savings account. Once you've completed all payments, you receive the funds.

These loans report to credit bureaus, building positive payment history while you save money. They're particularly valuable for people with thin credit files or those recovering from past financial difficulties.

Negotiate with Creditors

If you have late payments or other negative marks from creditors with whom you otherwise have a good relationship, consider requesting goodwill adjustments. Write a letter explaining the circumstances that led to the late payment and highlight your otherwise positive history.

While creditors aren't obligated to remove accurate information, many will consider goodwill requests for valued customers, especially for isolated incidents. Success isn't guaranteed, but strategies to boost your credit score often include negotiation as a component.

Time Your Applications Strategically

When you need to apply for credit, timing matters. Apply when your utilization is lowest-ideally right after you've paid down balances but before you've made new purchases. Most creditors report to bureaus once monthly, typically on the same date each month.

Coordinate major purchases and applications around these reporting dates to present the best possible credit profile to lenders.

Common Mistakes to Avoid

Opening Too Many New Accounts

While diversifying credit is beneficial, opening multiple accounts in a short period triggers red flags. Each application creates a hard inquiry, and new accounts lower your average account age. Space out applications by at least six months when possible.

Ignoring Small Balances

Even small balances on multiple cards can hurt your score. Having balances across five cards looks worse than having the same total balance concentrated on one or two cards. Consider which cards to pay off completely versus which to pay down strategically.

Closing Accounts After Paying Them Off

Many people instinctively close credit cards after paying them off, but this reduces available credit and can spike utilization ratios on remaining cards. Keep paid-off accounts open and use them occasionally to maintain the credit line.

| Mistake | Impact | Better Approach |

|---|---|---|

| Multiple new accounts | Hard inquiries, reduced account age | Space applications 6+ months apart |

| Balances on all cards | Multiple accounts with utilization | Pay some cards to $0, consolidate others |

| Closing paid-off cards | Reduced available credit | Keep accounts open with occasional use |

| Paying only minimums | High utilization persists | Pay above minimum, target high-utilization cards |

The Role of Professional Credit Repair

When to Consider Professional Help

While many credit improvement strategies are DIY-friendly, professional credit repair services can help in complex situations. If your credit report contains multiple errors, identity theft issues, or you lack time to manage the dispute process, professionals bring expertise and persistence.

Legitimate credit repair services:

- Never guarantee specific results

- Don't charge fees before providing services

- Inform you of your rights to dispute items yourself

- Provide written contracts with clear terms

Be wary of companies making unrealistic promises. Raising your credit score by 100 points in a year is achievable through legitimate means, but it requires consistent effort across multiple areas.

Self-Directed vs. Professional Approaches

You have the same legal rights as credit repair companies to dispute inaccurate information. The Fair Credit Reporting Act gives you the power to challenge items on your credit report. However, professionals understand the nuances of credit law and can navigate complex situations more efficiently.

For straightforward cases-correcting clear errors, paying down balances, establishing payment history-self-directed approaches work well. Complex situations involving bankruptcy, foreclosure, or identity theft may benefit from professional guidance.

Creating Your Personalized Action Plan

Assess Your Starting Point

Begin by obtaining all three credit reports and your credit scores. Identify which factors are most negatively impacting your score. Someone with high utilization but perfect payment history needs a different strategy than someone with low utilization but multiple late payments.

Create a priority list based on:

- Errors or inaccuracies requiring disputes

- High-utilization accounts to pay down

- Upcoming payment due dates to ensure perfect history

- Opportunities to add positive information (authorized user, credit builder loan)

- Negative items to negotiate or settle

Set Realistic Milestones

Understanding how to get your credit score up 100 points fast involves setting achievable interim goals. If you're starting at 580, your first milestone might be reaching 620 within three months, then 680 by month six.

Track progress monthly and adjust strategies based on results. If paying down credit cards produces significant improvements, prioritize that approach. If disputes remove errors that boost your score, focus on thoroughly reviewing all reports for additional inaccuracies.

Maintain Long-Term Habits

The strategies that help you raise your credit score 100 points are the same habits that maintain excellent credit long-term. Treat credit building as a permanent lifestyle change rather than a temporary project.

Sustainable credit habits include:

- Setting up automatic minimum payments on all accounts

- Reviewing credit reports quarterly

- Keeping utilization below 30% at all times

- Only applying for credit when necessary

- Maintaining diverse account types with positive history

These practices not only help you achieve your initial 100-point goal but position you for continued credit health and access to favorable lending terms.

Improving your credit score by 100 points transforms your financial opportunities, from qualifying for better interest rates to accessing financing for important life needs. The journey requires commitment to payment discipline, strategic debt management, and regular monitoring of your credit profile. If you're in Louisiana, Mississippi, Tennessee, or Georgia and need financing while working on credit improvement, Standard Financial specializes in helping clients with past credit challenges access personal loans for home improvements, medical expenses, education, and more. Our flexible financing plans and refinancing options can support your financial goals while you build toward excellent credit.

No comment yet, add your voice below!