Financial emergencies don't wait for payday. Whether you're facing unexpected medical bills, urgent home repairs, or essential expenses that can't wait, cash loans provide a viable solution for accessing funds quickly. These short-term financing options have become increasingly popular among consumers who need immediate financial assistance. Understanding how these loans work, their various types, and the responsible borrowing practices associated with them can help you make informed decisions during times of financial stress.

Understanding the Fundamentals of Cash Loans

Cash loans represent a broad category of short-term financing designed to provide quick access to funds. Unlike traditional bank loans that may take weeks to process, these lending products typically offer expedited approval and funding, sometimes within the same business day. The streamlined application process and minimal documentation requirements make them particularly attractive for urgent financial needs.

The primary characteristic distinguishing cash loans from other financing options is their speed and accessibility. Lenders focus less on extensive credit checks and more on your ability to repay the loan based on current income. This approach opens opportunities for borrowers who might not qualify for conventional financing.

Types of Cash Loans Available

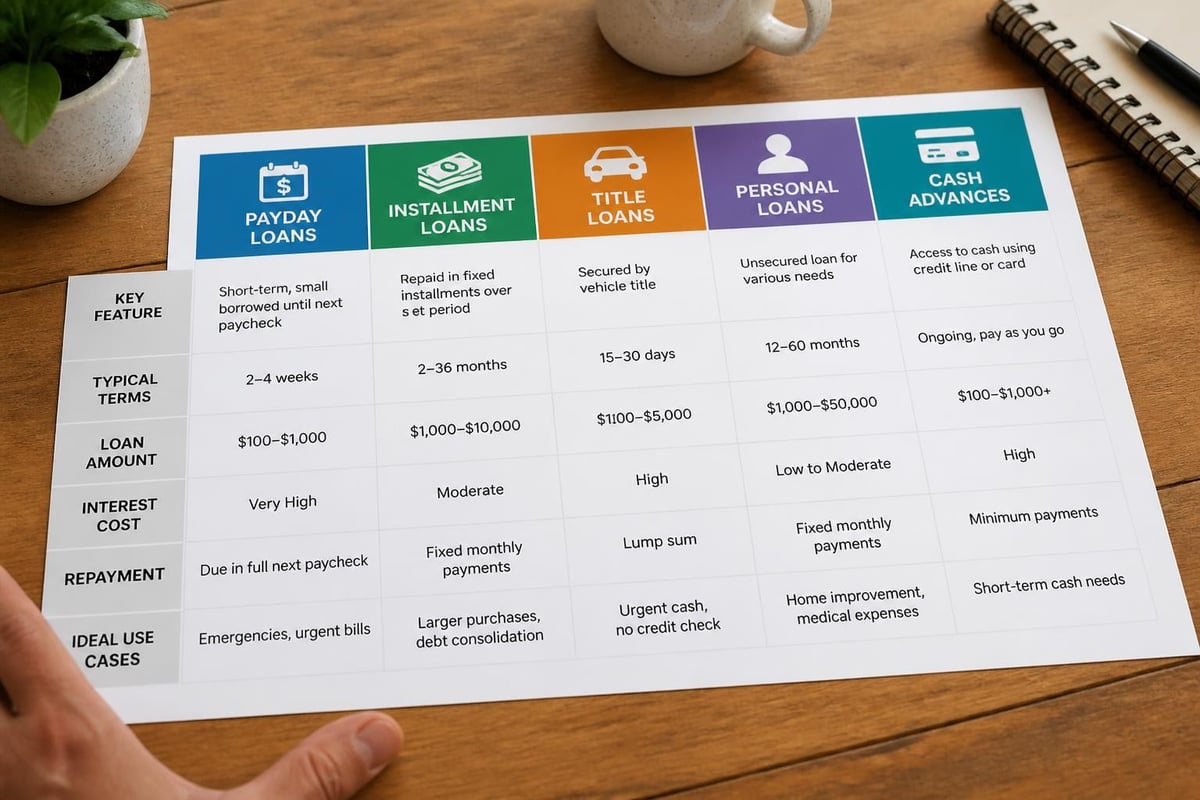

Several variations of cash loans serve different financial situations and borrower needs:

- Payday loans: Short-term loans typically due on your next payday

- Installment loans: Structured repayment plans spread over several months

- Title loans: Secured loans using your vehicle as collateral

- Personal loans: Unsecured personal loans based on creditworthiness and income

- Cash advances: Borrowing against credit card limits or future earnings

Each type serves specific purposes and comes with distinct terms, interest rates, and repayment structures. Understanding these differences helps borrowers select the most appropriate option for their circumstances.

The Application Process and Requirements

Applying for cash loans has become increasingly straightforward, particularly with online lending platforms. Most lenders require basic documentation including proof of income, identification, and banking information. The simplified process reflects the industry's focus on accessibility and speed.

Essential Documentation

When preparing your application, gather these key documents:

- Valid government-issued identification (driver's license or passport)

- Proof of steady income (recent pay stubs or bank statements)

- Active checking account information

- Social Security number

- Contact information including phone number and email address

The verification process typically takes minutes rather than days. Lenders use this information to assess your repayment capacity and determine loan amounts. While some lenders perform credit checks, many focus primarily on income verification.

Approval Timeline and Funding

The speed advantage becomes evident during the approval phase. Traditional bank loans might require multiple appointments and extensive waiting periods. Cash loans, conversely, often provide decisions within hours. Once approved, funds can appear in your account as quickly as the next business day, though timing varies by lender and banking institutions.

| Loan Type | Approval Time | Funding Speed | Documentation Level |

|---|---|---|---|

| Traditional Bank Loan | 3-7 days | 5-14 days | Extensive |

| Cash Loans | 1-24 hours | 1-3 days | Minimal |

| Payday Loans | Minutes-hours | Same/next day | Very minimal |

| Personal Installment | 24-48 hours | 1-5 days | Moderate |

Understanding Costs and Interest Rates

Financial transparency remains crucial when considering cash loans. The convenience and accessibility come with costs that borrowers must understand before committing. Interest rates and fees vary significantly across lenders and loan types, making comparison shopping essential.

Annual percentage rates (APR) on cash loans typically exceed those of traditional bank products. This reflects the higher risk lenders assume and the administrative costs of processing smaller, shorter-term loans. While payday loans can carry substantial costs, installment loans often provide more favorable terms with structured repayment plans.

Fee Structures to Consider

Beyond interest rates, borrowers should understand additional costs:

- Origination fees: Charged when the loan is issued

- Late payment penalties: Applied when payments are missed

- Rollover fees: Costs for extending or renewing loans

- Prepayment penalties: Sometimes charged for early repayment (less common)

Responsible lenders clearly disclose all fees upfront. Reading the loan agreement carefully protects you from unexpected charges and helps you calculate the true cost of borrowing.

Regulatory Framework and Consumer Protections

The cash loan industry operates under strict regulatory oversight designed to protect consumers. The Consumer Financial Protection Bureau provides comprehensive guidance on lending practices and borrower rights. These regulations aim to prevent predatory lending while maintaining access to credit for those who need it.

State laws vary considerably regarding cash loans. Some states impose interest rate caps, while others have specific licensing requirements for lenders. Understanding your state's regulations helps you identify legitimate lenders and recognize your rights as a borrower.

Your Rights as a Borrower

Federal and state laws protect consumers through various mechanisms:

- Truth in Lending Act: Requires clear disclosure of loan terms and costs

- Fair Debt Collection Practices Act: Regulates how lenders can collect debts

- Equal Credit Opportunity Act: Prohibits discrimination in lending decisions

- State usury laws: Cap maximum interest rates in many jurisdictions

These protections ensure transparency and fair treatment throughout the borrowing process. If you encounter violations, consumer protection agencies provide recourse for addressing grievances.

Benefits and Appropriate Use Cases

Cash loans serve legitimate financial needs when used responsibly. Their speed and accessibility make them valuable tools for specific situations. Understanding when these loans make sense helps borrowers avoid unnecessary debt while addressing urgent needs.

Emergency expenses represent the most appropriate use for cash loans. Unexpected medical bills, urgent vehicle repairs needed for work commuting, or essential home repairs preventing further damage justify short-term borrowing. The key consideration is whether the expense cannot wait and whether you have reasonable repayment capacity.

Strategic Borrowing Scenarios

Consider cash loans for these situations:

- Medical emergencies requiring immediate treatment

- Vehicle repairs essential for employment

- Preventing utility disconnections

- Covering essential expenses between paychecks

- Time-sensitive opportunities with clear returns

The common thread is urgency combined with necessity. Discretionary purchases or non-essential expenses rarely justify the costs associated with cash loans.

| Use Case | Appropriateness | Alternative Options |

|---|---|---|

| Medical Emergency | High | Payment plans, medical credit cards |

| Home Repair (urgent) | High | Home equity, contractor financing |

| Vacation | Low | Savings, credit cards |

| Debt Consolidation | Medium | Balance transfer cards, personal loans |

| Vehicle Repair (work-related) | High | Mechanic payment plans, credit cards |

Risks and Considerations

While cash loans provide valuable access to funds, they carry inherent risks that borrowers must consider. The most significant concern is the debt cycle that can develop when borrowers repeatedly roll over or renew loans. Understanding the pros and cons of cash advances helps borrowers make informed decisions.

High interest rates compound quickly on short-term loans. A loan that seems manageable initially can become burdensome if repayment extends beyond the original term. Borrowers must honestly assess their repayment capacity before accepting loan terms.

Warning Signs of Problem Borrowing

Recognize these red flags indicating potential debt problems:

- Borrowing to pay off previous loans

- Missing payments on other obligations to pay loan installments

- Taking maximum loan amounts without clear repayment plans

- Avoiding reading loan terms and conditions

- Feeling pressured or rushed by lenders

Credit score impacts vary depending on the lender and your repayment performance. While some cash loan providers don't report to credit bureaus, missed payments and defaults can negatively affect your credit rating when reported.

Alternatives to Consider

Before committing to cash loans, explore alternative financing options that might offer better terms or lower costs. Building a comprehensive financial strategy includes understanding all available resources during emergencies.

Short-Term Alternatives

Several options provide quicker access to funds without the high costs of traditional cash loans:

- Employer advances: Many companies offer paycheck advances to employees

- Credit union loans: Member-focused institutions often provide favorable terms

- Payment plans: Negotiate directly with service providers or creditors

- Community assistance programs: Local organizations may offer emergency funds

- Family or friend loans: Personal arrangements with clear repayment terms

Emergency savings funds represent the best long-term alternative. Even modest savings of $500 to $1,000 can cover many unexpected expenses without borrowing. Building this cushion should be a priority after resolving immediate financial needs.

Longer-Term Solutions

For non-urgent needs, consider these options:

- Traditional personal loans: Lower rates for qualified borrowers

- Credit cards: Better for smaller amounts with repayment flexibility

- Home equity lines: Leverage property value for larger needs

- Secured loans: Use assets as collateral for better terms

Each alternative has specific advantages and requirements. Comparing options based on your timeline, creditworthiness, and repayment ability ensures optimal decision-making.

Responsible Borrowing Practices

Successful cash loan experiences depend on responsible borrowing behaviors. Following established best practices protects your financial health while addressing immediate needs. Creating a repayment plan before accepting loan terms demonstrates financial maturity and preparedness.

Borrow only what you need rather than accepting the maximum offered amount. Larger loans mean higher interest costs and more challenging repayment obligations. Calculate your actual need and add a small buffer for unexpected costs.

Before You Borrow Checklist

Ask yourself these critical questions:

- Can this expense wait until next payday?

- Have I exhausted all lower-cost alternatives?

- Do I understand all fees and the total repayment amount?

- Can I afford the payments without sacrificing essentials?

- What happens if I cannot repay on time?

Reading and understanding loan agreements cannot be overemphasized. These documents contain crucial information about interest rates, fees, payment schedules, and lender rights. Never sign documents you don't fully understand.

Successful Repayment Strategies

Once you've secured a loan, focus on successful repayment:

- Set up automatic payments to avoid late fees

- Pay more than the minimum when possible to reduce interest

- Contact lenders immediately if you anticipate payment difficulties

- Track payment dates on calendars or through financial apps

- Prioritize loan repayment in your monthly budget

Proactive communication with lenders often yields solutions when financial difficulties arise. Many lenders offer hardship programs or modified payment plans rather than forcing defaults.

Building Financial Resilience

While cash loans address immediate needs, building long-term financial resilience prevents future borrowing necessity. This involves creating emergency savings, improving credit scores, and developing sustainable budgeting practices.

Emergency fund development should begin with small, consistent contributions. Even $25 per paycheck accumulates to meaningful amounts over time. Automated transfers to savings accounts make this process effortless and consistent.

Financial Health Improvement Steps

Strengthen your financial position through these actions:

- Create and maintain a realistic monthly budget

- Review and reduce unnecessary subscriptions and expenses

- Build credit through responsible credit card use

- Increase income through side jobs or skill development

- Seek financial counseling for debt management strategies

Financial literacy resources, including those from government agencies and nonprofit organizations, provide valuable guidance for improving money management skills. Investing time in financial education pays long-term dividends through better decision-making.

| Action Item | Time Commitment | Impact Level | Difficulty |

|---|---|---|---|

| Create Budget | 2-4 hours initially | High | Low-Medium |

| Build Emergency Fund | Ongoing | Very High | Medium |

| Review Credit Report | 1 hour annually | High | Low |

| Financial Education | 30 min weekly | Medium-High | Low |

| Increase Income | Varies | High | Medium-High |

Selecting the Right Lender

Choosing a reputable lender significantly impacts your borrowing experience. Not all cash loan providers operate with the same standards of transparency and customer service. Researching lenders before applying protects you from predatory practices and ensures fair treatment.

Licensing and accreditation serve as initial indicators of legitimacy. Verify that lenders hold appropriate state licenses and belong to industry associations promoting ethical practices. State banking departments maintain databases of licensed lenders you can check.

Evaluation Criteria for Lenders

Compare potential lenders using these factors:

- Transparency: Clear disclosure of all fees and terms

- Customer reviews: Experiences from previous borrowers

- Response time: Speed of customer service inquiries

- Flexibility: Willingness to work with borrowers during hardship

- Technology: User-friendly application and account management platforms

Physical branch locations offer advantages for borrowers who prefer in-person interactions. Local lenders often provide more personalized service and better understanding of community-specific financial challenges. Companies with regional presence in multiple states demonstrate stability and commitment to their markets.

Understanding cash loans empowers you to make informed financial decisions during challenging times. By recognizing appropriate use cases, comparing costs, and practicing responsible borrowing, these financing tools can serve as valuable resources rather than financial burdens. When you need quick access to funds for emergencies, medical expenses, home improvements, or other essential needs, Standard Financial offers flexible financing solutions with personalized service across Louisiana, Mississippi, Tennessee, and Georgia. Our experienced team works with clients from all credit backgrounds to find appropriate lending solutions that fit your specific situation and repayment capacity.

No comment yet, add your voice below!