Understanding your financial standing requires more than just knowing your bank balance. A credit profile check serves as a comprehensive snapshot of your borrowing history, payment patterns, and overall creditworthiness. This review process examines the detailed information maintained by credit bureaus about your financial behavior, providing insights that can significantly impact your ability to secure loans, obtain favorable interest rates, and achieve your financial goals. Whether you're planning a home renovation, consolidating debt, or preparing for a major purchase, knowing what appears in your credit profile empowers you to make informed decisions and take control of your financial future.

What a Credit Profile Check Reveals About Your Financial History

A credit profile check uncovers the complete record of your credit activities across multiple dimensions. This examination goes far beyond a simple three-digit score, diving into the granular details that shape your financial reputation.

The Core Components Examined

When you conduct a credit profile check, you'll discover several critical categories of information. Personal identification data forms the foundation, including your name, current and previous addresses, Social Security number, date of birth, and employment history. This section ensures the credit file belongs to you and helps prevent identity confusion.

Account information represents the most substantial portion of any credit profile. This includes:

- Credit card accounts with limits, balances, and payment history

- Installment loans such as auto financing or personal loans

- Mortgages and home equity lines of credit

- Student loan obligations

- Retail credit accounts from department stores

Each account listing shows the date opened, credit limit or loan amount, current balance, and a detailed payment history indicating whether you've paid on time, late, or missed payments entirely.

Payment Patterns and Their Impact

The Consumer Financial Protection Bureau’s guide to checking your credit report emphasizes that payment history carries tremendous weight in credit evaluations. A credit profile check reveals not just whether you pay, but how consistently you meet your obligations.

Payment records typically extend seven years into the past. Late payments are categorized by severity: 30 days late, 60 days late, 90 days late, and beyond. Each level of delinquency creates a more negative impact on your profile.

| Payment Status | Impact Level | Duration on Report |

|---|---|---|

| On-time payments | Positive | Entire account life |

| 30 days late | Moderate negative | 7 years |

| 60 days late | Significant negative | 7 years |

| 90+ days late | Severe negative | 7 years |

| Charge-off/Collection | Critical negative | 7 years |

Why Regular Credit Profile Checks Matter for Borrowers

Conducting periodic reviews of your credit profile serves multiple strategic purposes that extend well beyond simple curiosity about your credit score.

Error Detection and Correction

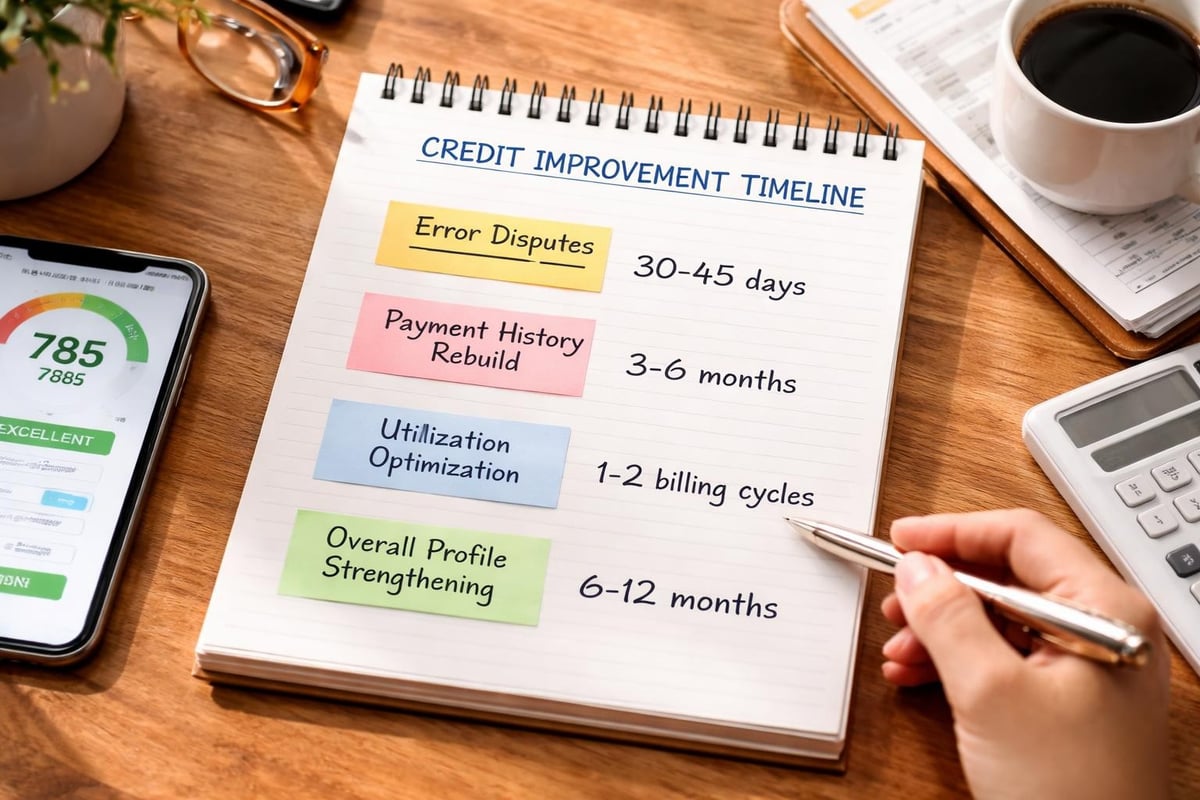

Credit reporting errors occur more frequently than most consumers realize. A credit profile check can uncover mistakes such as accounts that don't belong to you, incorrect payment statuses, duplicate entries, or outdated information that should have been removed. According to Consumer Reports’ guidance on reading credit reports, identifying and disputing these errors can lead to significant improvements in your credit standing.

Standard Financial clients in Louisiana, Mississippi, Tennessee, and Georgia often discover that correcting even minor errors opens doors to better financing terms. A misreported late payment or an account incorrectly shown as open when it's actually closed can make a measurable difference in loan approval decisions.

Identity Theft Prevention

Regular credit profile checks serve as an early warning system for identity theft. Unfamiliar accounts, inquiries you didn't authorize, or addresses where you've never lived signal potential fraud. The sooner you detect these red flags, the faster you can take corrective action to minimize damage to your financial reputation.

Key warning signs to watch for:

- Accounts opened in your name without your knowledge

- Credit inquiries from lenders you never contacted

- Addresses or employers you don't recognize

- Sudden, unexplained drops in your credit score

Loan Preparation and Planning

Before applying for any significant financing-whether for medical expenses, education, or home improvements-a credit profile check provides crucial preparation time. Understanding your current standing allows you to address weaknesses, gather explanations for legitimate issues, and set realistic expectations about loan terms you're likely to receive.

How to Access and Interpret Your Credit Profile

Obtaining your credit information has become increasingly accessible, though understanding what you receive requires some guidance.

Official Sources for Credit Profile Checks

Federal law entitles you to one free credit report annually from each of the three major credit bureaus: Equifax, Experian, and TransUnion. The official website for accessing these reports provides a centralized platform for requesting your information without cost or obligation.

Beyond these annual reports, you may also access your credit profile through:

- Credit monitoring services that provide ongoing access to your information

- Credit card issuers who often provide free credit score tracking to cardholders

- Lenders when you apply for credit, though this triggers an inquiry

- Specialized credit counseling organizations offering guidance alongside access

The CFPB’s resource on obtaining credit scores clarifies the distinction between free credit reports and credit scores, noting that while reports detail your credit history, scores provide a numerical summary of your creditworthiness.

Reading Your Credit Profile Effectively

A credit profile check generates a detailed document that can initially seem overwhelming. Focus on these priority areas first:

Account Review Section: Examine each listed account for accuracy. Verify that balances match your records, payment statuses are correct, and no fraudulent accounts appear. Pay particular attention to accounts marked as delinquent, in collections, or charged off.

Inquiry Section: Credit inquiries fall into two categories-hard inquiries from credit applications and soft inquiries from background checks or pre-approval offers. Hard inquiries can temporarily lower your score, so verify that all listed inquiries correspond to applications you actually submitted.

Public Records: This section includes bankruptcies, tax liens, and civil judgments. These items carry severe negative weight and remain on your profile for extended periods, though recent changes to reporting standards have removed most tax liens and civil judgments from credit reports.

| Credit Profile Section | Information Included | Review Priority |

|---|---|---|

| Personal Information | Name, addresses, employment | High – verify accuracy |

| Account Details | All credit accounts and loans | Critical – check each entry |

| Payment History | Record of on-time and late payments | Critical – dispute errors |

| Inquiries | Credit applications and checks | Medium – verify authenticity |

| Public Records | Bankruptcies, liens, judgments | High – confirm accuracy |

Understanding Who Can Access Your Credit Profile

The Fair Credit Reporting Act governs who may legally conduct a credit profile check on you and under what circumstances. This federal legislation establishes strict parameters for credit information access, protecting consumer privacy while allowing legitimate business needs.

Permissible Purposes for Credit Checks

Lenders represent the most common entities accessing credit profiles. When you apply for a personal loan, mortgage, or credit card, the creditor performs a credit profile check to assess risk and determine appropriate terms. This inquiry requires your explicit or implied consent through the application process.

Other authorized parties include:

- Employers conducting background checks with your written permission

- Landlords evaluating rental applications

- Insurance companies determining policy rates in states where permitted

- Government agencies for licensing or benefit determination

- Collection agencies pursuing legitimate debts

Understanding who can legally access your credit information helps you recognize unauthorized access attempts and protect your privacy rights.

Hard vs. Soft Inquiries

Not all credit profile checks impact your credit score equally. Hard inquiries occur when you apply for credit, and the lender reviews your full credit profile to make a lending decision. These inquiries remain visible on your credit report for two years and may temporarily reduce your score by a few points.

Soft inquiries happen when you check your own credit, when creditors pre-screen you for offers, or when existing creditors review your account. These inquiries don't affect your credit score and may not be visible to other parties reviewing your profile.

Strategic timing of credit applications helps minimize the impact of hard inquiries. Clustering similar applications-such as mortgage shopping-within a short window (typically 14-45 days) allows credit scoring models to count them as a single inquiry.

Improving What a Credit Profile Check Reveals

Once you understand your current credit standing, you can implement targeted strategies to strengthen your profile over time.

Addressing Negative Items Strategically

A credit profile check may reveal legitimate negative information that can't simply be disputed away. Focus on demonstrating improvement through consistent positive behavior moving forward.

For accounts in collections, consider these approaches:

- Negotiate payment arrangements that fit your budget while satisfying the debt

- Request pay-for-delete agreements where collectors remove the item after payment

- Document all agreements in writing before making payments

- Prioritize recent debts as newer negative items impact scores more heavily

Past credit issues shouldn't permanently derail your financial goals. Standard Financial specializes in working with clients across Louisiana, Mississippi, Tennessee, and Georgia who have experienced credit challenges, recognizing that credit profiles don't tell complete stories about people's circumstances or potential.

Building Positive Credit History

Positive information strengthens your credit profile more effectively than the absence of negative items. If your credit profile check reveals thin or limited credit history, consider these building strategies:

Secured credit cards require deposits but report to credit bureaus just like traditional cards, establishing payment history without requiring strong existing credit. Use the card for small, regular purchases and pay the full balance monthly.

Credit-builder loans offered by some financial institutions allow you to make payments into a savings account while simultaneously building credit history. Once you complete payments, you receive the saved funds plus any interest earned.

Authorized user status on someone else's well-managed account can add positive payment history to your profile, though this strategy requires trust and careful selection of the primary account holder.

Optimizing Credit Utilization

Credit utilization-the ratio of your current balances to available credit limits-significantly influences credit scores. A credit profile check showing high utilization across credit cards signals potential financial stress to lenders.

Target keeping utilization below 30% on individual cards and overall. Even better, maintain utilization under 10% for optimal impact. This doesn't mean avoiding credit use entirely; it means managing balances strategically through payment timing and limit increases.

Common Misconceptions About Credit Profile Checks

Several persistent myths surround credit profiles and checking them, leading consumers to make decisions based on incomplete or incorrect information.

Myth: Checking your own credit damages your score. Reality: Personal credit profile checks count as soft inquiries and have zero impact on your credit score. You should review your credit regularly without concern about score damage.

Myth: Closing old accounts improves your credit profile. Reality: Closing accounts, particularly older ones, can actually harm your credit by reducing available credit (increasing utilization) and shortening your average account age. Keep old accounts open and occasionally active unless they carry fees.

Myth: You only have one credit score. Reality: Multiple credit scoring models exist, and each of the three major bureaus maintains separate files. A credit profile check from one bureau may reveal different information or scores than another bureau's report.

Myth: Paying off collections removes them from your profile. Reality: Unless you negotiate specific removal terms, paid collections typically remain on your credit report for seven years from the original delinquency date. However, newer scoring models give less weight to paid collections than unpaid ones.

The FDIC’s explanation of credit reports and scores clarifies these and other common confusions, providing authoritative guidance on credit fundamentals.

Special Considerations for Loan Applicants

When preparing to apply for personal loans, refinancing, or specialized financing for home improvements, medical expenses, or education, a credit profile check becomes particularly valuable.

Pre-Application Profile Review

Conduct a thorough credit profile check at least 60-90 days before submitting loan applications. This timeline provides adequate opportunity to dispute errors, address minor issues, and understand the terms you're likely to receive.

Document any circumstances that explain legitimate negative items-job loss, medical emergencies, divorce, or other life events that temporarily impacted your ability to meet obligations. While these explanations don't erase negative information, they provide context that lending specialists can consider when evaluating your application.

Understanding Lender Perspectives

Lenders conducting credit profile checks evaluate multiple factors simultaneously. They don't simply approve or deny based on a single score threshold. Instead, they consider:

- Debt-to-income ratio showing your current obligations relative to income

- Payment trends indicating whether your credit management is improving or declining

- Credit mix demonstrating experience managing different types of credit

- Recent activity revealing current financial behavior and stability

Standard Financial's approach recognizes that credit profiles represent moments in time, not permanent judgments. A credit profile check showing past difficulties doesn't automatically disqualify borrowers who demonstrate current stability and commitment to meeting their obligations.

State-Specific Considerations

Credit reporting and lending practices can vary by state. Residents of Louisiana, Mississippi, Tennessee, and Georgia should be aware of state-specific protections and regulations that may affect how credit information is used and reported.

Some states impose additional restrictions on how far back certain negative information can be considered for employment or housing purposes. Understanding these protections helps you advocate for fair treatment when negative items appear on your credit profile check.

Maintaining Long-Term Credit Profile Health

Sustainable credit management requires ongoing attention rather than sporadic interventions when you need financing.

Establishing Regular Review Habits

Create a systematic schedule for credit profile checks. Consider staggering requests from the three major bureaus throughout the year-requesting one every four months ensures continuous monitoring while maximizing your free annual reports.

Set calendar reminders to review your credit at consistent intervals. This routine transforms credit monitoring from a reactive task you perform only when problems arise into a proactive habit supporting long-term financial health.

Recommended review schedule:

- January: Request report from Bureau A, review for errors, document findings

- May: Request report from Bureau B, compare with previous report, note changes

- September: Request report from Bureau C, assess progress toward goals

- Quarterly: Check free credit scores from credit card issuers or monitoring services

Documenting Your Credit Journey

Maintain records of your credit profile checks over time. This documentation serves multiple purposes: tracking improvement, providing evidence for disputes, and demonstrating responsibility to future lenders.

Keep copies of dispute letters, creditor communications, and confirmation of corrected errors. If you need to explain credit issues to a lender, contemporaneous documentation proves far more credible than unsupported verbal explanations.

Responding to Life Changes

Major life events warrant immediate credit profile checks. Marriage, divorce, job changes, relocations, and identity theft attempts all justify out-of-cycle credit reviews to ensure your profile accurately reflects your current circumstances.

After experiencing financial hardship, conduct a credit profile check once the immediate crisis passes. Understanding how the situation affected your credit helps you develop realistic timelines for recovery and plan appropriate next steps for rebuilding.

Regular credit profile checks empower you to understand your financial standing, correct errors, and make informed decisions about your borrowing needs. Whether you're planning a major purchase, consolidating existing debts, or simply maintaining financial awareness, knowing what appears in your credit profile puts you in control of your financial future. If you're ready to explore financing options tailored to your unique situation-even if your credit history includes challenges-Standard Financial offers personalized lending solutions across Louisiana, Mississippi, Tennessee, and Georgia, with flexible terms designed to help you achieve your goals regardless of past credit issues.

No comment yet, add your voice below!