Finding a personal loan bank low interest option can make the difference between manageable monthly payments and financial strain. With interest rates fluctuating throughout 2026, borrowers across Louisiana, Mississippi, Tennessee, and Georgia are searching for affordable financing solutions. Whether you need funds for home improvements, medical expenses, or educational costs, understanding how to secure the lowest possible rate requires knowledge of current market conditions, lender requirements, and your own financial position. The right personal loan can provide the flexibility you need without overwhelming your budget.

Understanding Personal Loan Interest Rates in 2026

Banks and financial institutions calculate personal loan rates based on multiple risk factors. Your credit score remains the primary determinant, but lenders also evaluate your income stability, existing debt obligations, and employment history.

The Federal Reserve's monetary policy decisions throughout recent years have created opportunities for borrowers to find competitive rates. Recent rate cuts by the Federal Reserve have influenced the lending landscape, though individual rates vary significantly based on borrower qualifications.

What Constitutes a Low Interest Rate

A personal loan bank low interest rate in 2026 typically falls below the national average. According to current market trends from Bankrate, average rates range from 6% to 36% depending on creditworthiness and loan terms.

Factors that define competitive rates include:

- APR below 10% for excellent credit (720+)

- APR between 10-15% for good credit (680-719)

- APR between 15-20% for fair credit (640-679)

- Specialized programs for credit challenges

The gap between highest and lowest rates demonstrates why comparison shopping matters tremendously for your financial health.

How Banks Determine Your Interest Rate

Financial institutions use sophisticated underwriting models to assess lending risk. Understanding these factors empowers you to negotiate better terms and improve your application strength.

Credit Score Impact

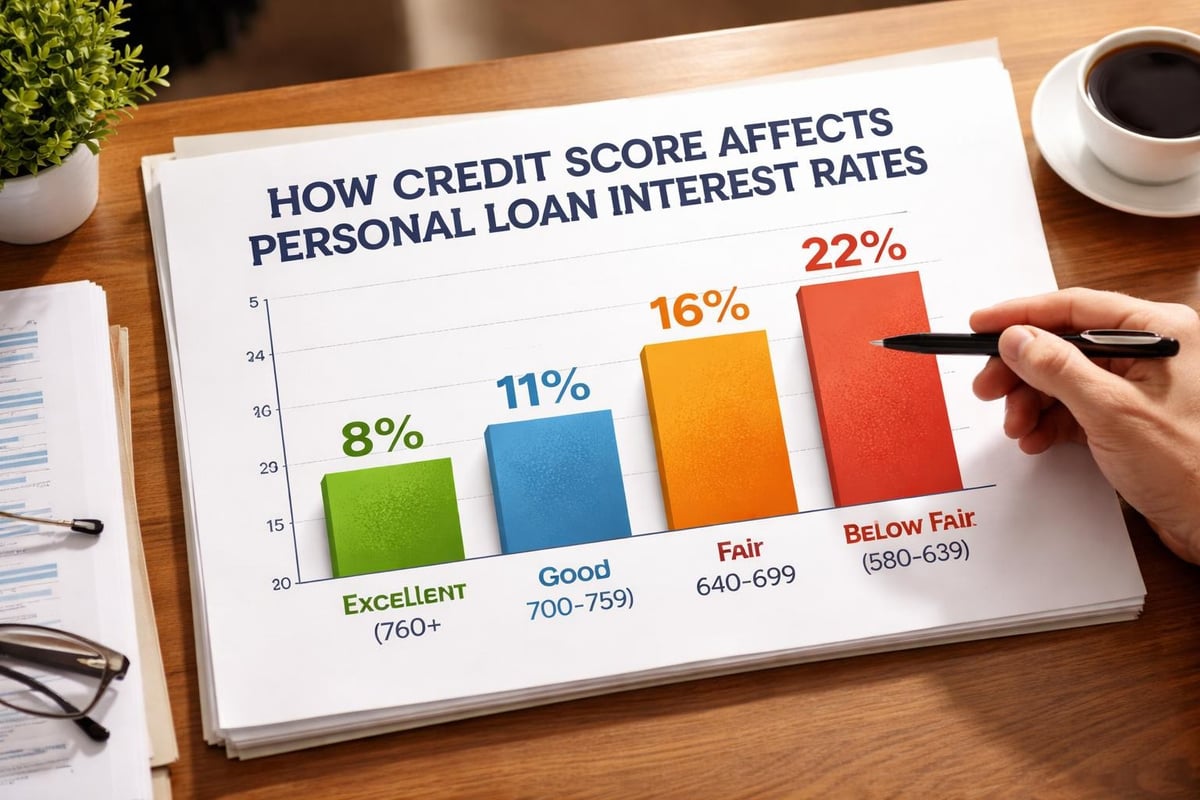

Your FICO score serves as a shorthand for creditworthiness. Banks categorize applicants into risk tiers, with each tier receiving different rate offerings.

| Credit Score Range | Typical APR Range | Risk Classification |

|---|---|---|

| 720-850 | 6-10% | Excellent |

| 680-719 | 10-15% | Good |

| 640-679 | 15-20% | Fair |

| 580-639 | 20-28% | Poor |

| Below 580 | 28-36% | Very Poor |

Remember that these ranges represent general market conditions. Individual lenders may offer better or worse terms based on their specific criteria and business objectives.

Debt-to-Income Ratio Considerations

Banks calculate your debt-to-income (DTI) ratio by dividing monthly debt payments by gross monthly income. A DTI below 36% typically qualifies for the best personal loan bank low interest options.

Higher ratios signal greater financial stress, prompting lenders to increase rates or reduce loan amounts. Paying down existing debts before applying can significantly improve your rate eligibility.

Employment and Income Stability

Lenders prefer borrowers with consistent employment history. Two years in the same field or with the same employer demonstrates stability and reduces perceived risk.

Income verification requirements typically include:

- Recent pay stubs covering 30-60 days

- Tax returns for self-employed applicants

- Bank statements showing regular deposits

- Employment verification letters

Seasonal workers or commission-based earners may face additional scrutiny but can still qualify with proper documentation.

Strategies to Secure the Lowest Personal Loan Rates

Proactive preparation dramatically improves your chances of accessing personal loan bank low interest financing. These actionable strategies help position your application for success.

Improve Your Credit Score Before Applying

Even small credit score improvements can shift you into a better rate tier. Focus on these high-impact actions three to six months before applying.

- Pay down credit card balances below 30% of available credit limits

- Dispute inaccuracies on credit reports through annual free reports

- Avoid new credit inquiries that temporarily lower scores

- Make all payments on time to build positive payment history

- Keep old accounts open to maintain credit history length

These steps require discipline but deliver measurable financial benefits through reduced interest costs over your loan term.

Compare Multiple Lenders

Rate shopping within a focused timeframe minimizes credit score impact. Most scoring models treat multiple inquiries within 14-45 days as a single event.

Comparing personal loan offers from various institutions reveals significant rate differences. Regional banks, credit unions, and online lenders each offer distinct advantages.

Consider these lender types:

- Traditional banks: Established relationships may yield rate discounts

- Credit unions: Non-profit structure often means lower rates

- Online lenders: Lower overhead can translate to competitive pricing

- Specialized consumer lenders: Flexible approval for credit challenges

Don't limit yourself to the most familiar names. Smaller institutions frequently offer superior personal loan bank low interest terms to attract new customers.

Understand APR vs. Interest Rate

The Annual Percentage Rate (APR) includes both interest charges and fees, providing a complete cost picture. A loan advertising a low interest rate may carry high origination fees that increase the true borrowing cost.

| Fee Type | Typical Range | Impact on APR |

|---|---|---|

| Origination Fee | 1-8% of loan | Increases APR |

| Application Fee | $0-100 | Minimal impact |

| Prepayment Penalty | Varies | Limits flexibility |

| Late Payment Fee | $25-50 | Avoidable cost |

Always compare APRs rather than interest rates alone when evaluating personal loan bank low interest options. This ensures accurate cost comparison across lenders.

Loan Terms That Affect Your Interest Rate

Beyond borrower qualifications, loan structure significantly influences the rate you'll receive. Understanding these variables helps you optimize your borrowing strategy.

Loan Amount Considerations

Lenders often reserve their best rates for specific loan amount ranges. Very small loans (under $3,000) and very large loans (over $50,000) may carry higher rates due to administrative costs or increased risk exposure.

The sweet spot for many lenders falls between $10,000 and $35,000, where competitive pricing attracts quality borrowers while maintaining manageable risk profiles.

Repayment Period Impact

Shorter loan terms generally qualify for lower interest rates because lenders face reduced long-term risk. However, shorter terms mean higher monthly payments that may strain your budget.

Common term lengths and rate relationships:

- 12-24 months: Lowest rates but highest monthly payments

- 36-48 months: Balanced approach for moderate loans

- 60-72 months: Higher rates but smaller monthly obligations

- 84+ months: Reserved for larger amounts with premium pricing

Calculate total interest paid across different terms. Sometimes a slightly higher rate on a shorter term costs less overall than a lower rate stretched over many years.

Secured vs. Unsecured Loans

Unsecured personal loans require no collateral but carry higher interest rates to compensate for increased lender risk. Exploring unsecured loan options reveals competitive rates for qualified borrowers.

Secured loans backed by savings accounts, vehicles, or other assets offer reduced rates because collateral protects the lender. Consider this option if you need the lowest possible personal loan bank low interest rate and possess valuable assets.

Regional Considerations for Southern Borrowers

Financial institutions operating in Louisiana, Mississippi, Tennessee, and Georgia understand regional economic patterns and adjust their lending criteria accordingly.

State Regulations and Rate Caps

Each state maintains different consumer protection laws affecting maximum allowable interest rates and fees. These regulations create variation in available loan products across state lines.

Louisiana and Mississippi enforce stricter usury laws compared to Tennessee and Georgia, potentially limiting very high-rate products while encouraging competitive personal loan bank low interest offerings.

Local Economic Factors

Regional employment trends, cost of living variations, and housing market conditions influence lender risk assessments. Strong job markets in metropolitan areas like Nashville, Atlanta, and New Orleans may yield more competitive rate offerings.

Rural borrowers sometimes face fewer local options but benefit from online lender competition. Distance from branch offices matters less in the digital lending environment.

Building Relationships with Community Banks

Regional financial institutions value customer relationships and may offer rate discounts for existing account holders. Establishing checking or savings accounts three to six months before loan applications can unlock preferential pricing.

Relationship banking benefits include:

- Interest rate discounts of 0.25-0.50%

- Waived origination or application fees

- Flexible underwriting for borderline credit

- Personalized service throughout the loan process

These advantages particularly benefit borrowers with past credit challenges who need understanding underwriters.

Refinancing to Lower Your Interest Rate

Existing loan holders can reduce costs by refinancing when rates drop or credit improves. This strategy requires careful analysis to ensure savings exceed any fees.

When Refinancing Makes Sense

Calculate your breakeven point by dividing refinancing costs by monthly payment reduction. If you plan to keep the loan longer than this period, refinancing delivers net savings.

Understanding refinancing opportunities helps you identify optimal timing. Credit score improvements of 50+ points or market rate decreases of 2% or more signal strong refinancing potential.

Avoiding Refinancing Pitfalls

Some lenders advertise low rates but extend loan terms, increasing total interest despite lower monthly payments. Maintain or reduce your original payoff timeline to maximize savings.

Watch for prepayment penalties on existing loans that could eliminate refinancing benefits. Review your current loan agreement before proceeding with applications.

Special Programs for Credit Challenges

Past financial difficulties don't permanently disqualify you from personal loan bank low interest access. Specialized programs help borrowers rebuild credit while securing necessary funding.

Credit-Builder Loan Features

These products report positive payment history while providing funds, creating a path toward better rates on future borrowing. Initial rates may exceed prime offerings but remain reasonable compared to alternative financial products.

Successful repayment demonstrates creditworthiness to future lenders, potentially qualifying you for standard personal loan bank low interest rates within 12-24 months.

Co-Signer Benefits

Adding a co-signer with strong credit can dramatically improve your rate eligibility. The co-signer accepts equal responsibility for repayment, reducing lender risk and unlocking better pricing.

This arrangement benefits both parties when the primary borrower makes consistent on-time payments, building credit history without negative impact to the co-signer.

Alternative Qualification Methods

Some lenders emphasize income stability and employment history over credit scores. These institutions may approve borrowers with past issues at reasonable rates when traditional metrics show improvement.

Alternative underwriting considers:

- Bank account history and savings patterns

- Rent and utility payment consistency

- Educational background and career trajectory

- References from employers or community members

This comprehensive approach recognizes that credit scores don't tell complete financial stories.

Maximizing Your Loan Application Success

Strong applications receive better offers. Attention to detail and thorough preparation signal responsibility to underwriters reviewing your file.

Documentation Best Practices

Complete applications with all requested documentation move through approval faster and receive more favorable consideration. Missing information raises questions and may trigger additional verification requirements.

Organize documents digitally for easy submission. Include cover letters explaining any credit report items that might concern underwriters, demonstrating awareness and responsibility.

Timing Your Application Strategically

Apply when your financial picture looks strongest. Recent raises, completed debt payoffs, or credit score improvements deserve 30-60 days to fully reflect in credit reports before submitting applications.

Avoid applying during periods of employment transition, major purchases, or other financial stress that could complicate underwriting decisions.

Negotiating Rate Reductions

Don't accept the first offer without discussion. Lenders often have flexibility, especially for well-qualified borrowers or those with competing offers.

Present lower rates from competitors and ask your preferred lender to match or beat them. Loyalty to existing banking relationships provides leverage in these negotiations.

Using Personal Loans Responsibly

Accessing personal loan bank low interest financing represents only the first step. Responsible usage ensures positive financial outcomes and protects your credit standing.

Borrowing Only What You Need

Lenders may approve amounts exceeding your request, but larger balances mean higher interest costs. Stick to your original purpose and avoid unnecessary debt.

Create detailed budgets showing how loan proceeds will be allocated. This discipline prevents impulse spending and keeps you focused on repayment.

Setting Up Automatic Payments

Late payments damage credit scores and may trigger penalty fees and rate increases. Automatic withdrawals from checking accounts guarantee on-time payments and protect your financial reputation.

Schedule withdrawals shortly after paydays to ensure sufficient funds. Monitor accounts regularly to catch any issues before they affect payment processing.

Securing a personal loan bank low interest rate requires understanding lender criteria, preparing strong applications, and comparing multiple offers to find optimal terms. Your credit profile, income stability, and chosen loan structure all influence the rates available to you. Whether you're financing home improvements, covering medical expenses, or pursuing educational opportunities, Standard Financial offers flexible financing solutions across Louisiana, Mississippi, Tennessee, and Georgia, including specialized programs for borrowers with past credit challenges. Contact us today to explore your personal loan options and discover how competitive rates can help you achieve your financial goals.

No comment yet, add your voice below!