Homeownership brings both pride and responsibility, and sometimes that responsibility includes necessary upgrades, repairs, or renovations. Whether you're planning a kitchen remodel, adding energy-efficient windows, or replacing an aging roof, funding these projects requires careful financial planning. Home improvement loans provide a structured way to finance renovations without depleting your savings, offering homeowners across the Southeast access to funds specifically designed for property upgrades. Understanding the types of financing available, qualification requirements, and how to choose the right loan product can help you make informed decisions that protect your financial stability while enhancing your home's value and comfort.

Understanding Home Improvement Financing Options

Home improvement loans encompass several distinct financial products, each designed to meet different renovation needs and borrower circumstances. The Consumer Financial Protection Bureau defines home improvement loans as loans made for the purpose of repairing, rehabilitating, remodeling, or improving a dwelling or the real property on which the dwelling is located.

Personal Loans for Home Projects

Personal loans represent one of the most accessible financing options for renovations. These unsecured loans don't require you to use your home as collateral, which means faster approval and less risk to your property. Loan amounts typically range from $1,000 to $50,000, with repayment terms spanning two to seven years.

Key advantages include:

- No home equity required

- Fixed interest rates and predictable monthly payments

- Quick funding, often within days

- Flexible use for any improvement project

- No appraisal or home inspection needed

Standard Financial specializes in personal loans for home improvements throughout Louisiana, Mississippi, Tennessee, and Georgia, offering flexible terms even for borrowers with past credit challenges.

Home Equity Lines of Credit

A home equity line of credit (HELOC) functions like a credit card secured by your home's equity. You can borrow up to your approved credit limit, pay it back, and borrow again during the draw period, which typically lasts 5-10 years.

HELOCs work best for:

- Ongoing projects with uncertain costs

- Multiple smaller renovations over time

- Borrowers who want payment flexibility

- Homeowners with significant equity

Interest rates are usually variable, meaning your payments can fluctuate based on market conditions. This requires careful budgeting to ensure you can handle potential rate increases.

Home Equity Loans

Unlike HELOCs, home equity loans provide a lump sum upfront with fixed interest rates and consistent monthly payments. You'll repay the loan over a set term, typically 5-30 years, making budgeting straightforward.

| Feature | Home Equity Loan | HELOC | Personal Loan |

|---|---|---|---|

| Collateral | Home equity | Home equity | None |

| Interest Rate | Fixed | Variable | Fixed |

| Disbursement | Lump sum | Revolving credit | Lump sum |

| Approval Time | 2-6 weeks | 2-6 weeks | 1-7 days |

| Typical Amount | $10,000-$200,000 | $10,000-$500,000 | $1,000-$50,000 |

Government-Backed Loan Programs

The U.S. Department of Housing and Urban Development offers specialized programs for home improvement financing. Title 1 loans help homeowners finance property improvements with more flexible qualification requirements, while 203(k) loans combine home purchase and renovation costs into a single mortgage.

These programs particularly benefit first-time homeowners or those in underserved communities who might struggle to qualify for conventional financing.

Qualification Requirements and Credit Considerations

Securing financing for home improvements requires meeting specific lender criteria, though requirements vary significantly based on the loan type and lender policies.

Credit Score Impact

Your credit score plays a substantial role in determining eligibility and interest rates. Most lenders categorize borrowers into tiers:

Excellent Credit (740+): Access to the lowest available rates and most favorable terms across all loan products. Borrowers in this range qualify for premium pricing and larger loan amounts.

Good Credit (670-739): Competitive rates with slightly higher pricing than excellent credit. Most lenders readily approve applications in this range with standard documentation.

Fair Credit (580-669): Higher interest rates reflect increased lender risk. Some lenders specialize in this market segment, offering approval when traditional banks decline applications.

Poor Credit (Below 580): Limited options with conventional lenders, but specialized consumer lenders like Standard Financial provide accessible financing with flexible underwriting.

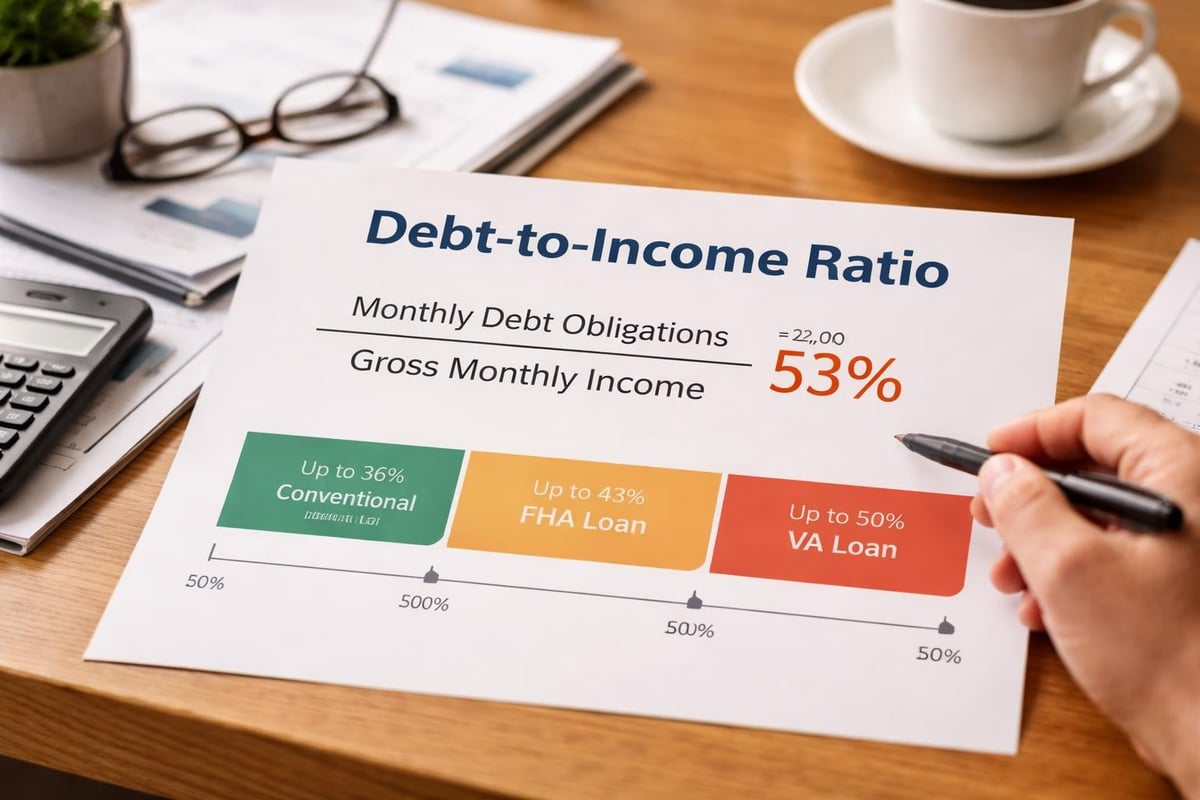

Income and Debt-to-Income Ratio

Lenders evaluate your ability to repay by analyzing your debt-to-income (DTI) ratio. This calculation divides your monthly debt payments by your gross monthly income.

DTI requirements typically include:

- Most lenders prefer DTI below 43%

- Some programs allow up to 50% with compensating factors

- Lower ratios improve approval odds and rates

- Self-employed borrowers need additional documentation

Documentation Requirements

Prepare these essential documents when applying:

- Proof of income (pay stubs, tax returns, W-2s)

- Identification (driver's license, passport)

- Proof of residence (utility bills, lease agreement)

- Bank statements (last 2-3 months)

- Project estimates (contractor bids, scope of work)

- Property information (for secured loans)

Comparing Interest Rates and Terms

Interest rates represent the cost of borrowing money, expressed as an annual percentage. The rate you receive depends on multiple factors including creditworthiness, loan type, loan amount, and repayment term.

Current Rate Environment in 2026

The lending landscape in 2026 shows varied rates across different products. Personal loans for home improvements typically range from 6% to 36% APR, depending on credit profiles and lender policies. Secured options using home equity generally offer lower rates, from 5% to 15%, reflecting reduced lender risk.

Rate-influencing factors include:

- Federal Reserve policy decisions

- Regional economic conditions in the Southeast

- Individual credit history and score

- Loan amount and repayment term

- Collateral type and value

Term Length Considerations

Shorter loan terms mean higher monthly payments but less total interest paid over the life of the loan. Longer terms reduce monthly obligations but increase overall interest costs.

A $25,000 loan at 10% APR demonstrates this relationship:

| Term Length | Monthly Payment | Total Interest Paid | Total Amount Repaid |

|---|---|---|---|

| 3 years | $806 | $4,016 | $29,016 |

| 5 years | $531 | $6,860 | $31,860 |

| 7 years | $406 | $9,784 | $34,784 |

Choose terms that balance affordable monthly payments with minimizing long-term interest costs.

Strategic Planning for Home Improvement Projects

Successful renovation financing starts with thorough project planning and realistic budgeting. Rushing into borrowing without proper preparation often leads to cost overruns and financial stress.

Prioritizing Renovation Projects

Not all home improvements offer equal value or urgency. According to research on home improvement loan trends, homeowners increasingly focus on projects that combine immediate functionality with long-term value enhancement.

High-priority projects typically include:

- Essential repairs (roof, foundation, HVAC)

- Safety upgrades (electrical, plumbing)

- Energy efficiency improvements

- Accessibility modifications

- Kitchen and bathroom updates

Lower-priority cosmetic upgrades:

- Paint and finishes

- Landscaping enhancements

- Luxury amenities

- Entertainment spaces

Creating a Comprehensive Budget

Accurate budgeting prevents borrowing shortfalls and helps you select appropriate loan amounts. Include these components:

- Materials costs (with 10-15% contingency)

- Labor expenses (contractor fees, permits)

- Professional services (architects, engineers)

- Temporary housing (if needed during work)

- Financing costs (interest, fees, insurance)

Contractors should provide detailed written estimates breaking down all project components. Request multiple bids to ensure competitive pricing and identify potential red flags.

Understanding Loan Approval Timelines

The speed at which you access funds varies significantly based on loan type and lender processes. Understanding these timelines helps you plan project starts and contractor schedules appropriately.

Unsecured Personal Loan Process

Personal loans offer the fastest path to funding. Online applications take 10-20 minutes to complete, with initial decisions often rendered within hours. Once approved, funds typically transfer to your bank account within one to seven business days.

Application steps include:

- Complete online or in-person application

- Submit required documentation

- Await underwriting decision

- Review and sign loan agreement

- Receive funds via direct deposit

This streamlined process makes personal loans ideal for time-sensitive projects or when contractors require immediate deposits.

Secured Loan Timelines

Home equity products involve more extensive evaluation due to collateral requirements. The complete process typically spans two to six weeks and includes:

- Initial application and documentation review

- Property appraisal scheduling and completion

- Title search and verification

- Underwriting analysis

- Closing appointment and fund disbursement

Plan project timelines accordingly, especially if weather-dependent work has seasonal deadlines.

Regional Considerations for Southeast Homeowners

Homeowners in Louisiana, Mississippi, Tennessee, and Georgia face unique considerations when financing improvements. Regional factors influence both project priorities and financing accessibility.

Climate-Related Improvements

The Southeast's humid subtropical climate creates specific maintenance and upgrade needs. Hurricane preparedness in coastal Louisiana and Mississippi drives demand for:

- Storm-resistant roofing materials

- Impact-resistant windows and doors

- Flood mitigation systems

- Generator installation

- Structural reinforcement

These improvements often qualify for insurance discounts, improving long-term affordability.

Property Value Dynamics

Real estate markets across the Southeast show varied appreciation rates. Studies examining home improvement loan distribution reveal regional patterns that affect renovation return on investment. Research your local market to ensure improvements align with buyer preferences and neighborhood standards.

Avoiding Common Financing Mistakes

Many homeowners encounter preventable problems when financing renovations. Learning from these common errors protects your financial health and project success.

Borrowing More Than Necessary

The temptation to borrow extra "just in case" can lead to unnecessary debt. Excess loan proceeds often get diverted to non-essential purchases, leaving you paying interest on funds that didn't improve your home.

Solution: Request quotes from multiple contractors, add a reasonable 10-15% contingency, and borrow only the calculated amount.

Neglecting Total Cost Analysis

Focusing solely on monthly payments while ignoring total interest costs creates long-term financial burden. A loan with lower monthly payments but extended terms may cost thousands more over its lifetime.

Solution: Compare total repayment amounts across different term options and choose the shortest term you can comfortably afford.

Skipping Contractor Verification

Reputable contractors carry proper licensing, insurance, and bonding. Hiring unverified workers to save money often results in substandard work, code violations, or abandoned projects.

Verification checklist:

- State contractor license (active status)

- General liability insurance

- Workers' compensation coverage

- References from recent clients

- Written contracts with detailed scopes

- Payment schedules tied to milestones

Underestimating Timeline Impacts

Projects frequently take longer than anticipated. If you've arranged temporary housing or time-sensitive financing, delays create additional costs and stress.

Solution: Build timeline buffers into your planning and maintain financial reserves for extended project durations.

Equity Preservation and Long-Term Value

Strategic renovations should enhance your home's market value while serving your immediate needs. Not all improvements offer equal returns, and understanding value dynamics helps prioritize projects wisely.

High-Return Improvements

Certain renovations consistently deliver strong returns when you eventually sell:

- Minor kitchen updates (appliances, countertops, cabinets)

- Bathroom remodels (fixtures, tile, vanities)

- Curb appeal enhancements (entry doors, garage doors, landscaping)

- Energy-efficient upgrades (windows, insulation, HVAC)

- Functional additions (extra bedroom, finished basement)

These projects appeal to broad buyer demographics and address common pain points that influence purchase decisions.

Over-Improvement Risks

Investing more than neighborhood values support creates "over-improvement" situations where you cannot recoup renovation costs at resale. A $100,000 kitchen in a $200,000 neighborhood rarely recovers its investment.

Prevention strategies:

- Research comparable home sale prices

- Align improvement quality with neighborhood standards

- Focus on functional necessity over luxury

- Consult real estate professionals before major projects

Refinancing and Consolidation Opportunities

Existing home improvement debt doesn't need to remain constant. Refinancing opportunities may improve terms, reduce rates, or simplify multiple payments into single monthly obligations.

When Refinancing Makes Sense

Consider refinancing your home improvement loan when:

- Interest rates have dropped significantly since origination

- Your credit score has improved substantially

- You want to extend terms to lower monthly payments

- Multiple debts could consolidate at a better overall rate

Calculate break-even points by comparing current remaining interest against new loan costs, including any origination or prepayment fees.

Standard Financial Refinancing Solutions

Consumer lenders specializing in refinancing can restructure existing obligations to better fit current financial circumstances. Flexible underwriting accommodates borrowers whose situations have changed since their original loan, whether through income fluctuations, credit recovery, or evolving family needs.

Responsible Borrowing Practices

Maintaining financial health while pursuing home improvements requires disciplined borrowing and repayment strategies.

Borrowing Within Your Means

Financial advisors generally recommend keeping total housing costs (mortgage, insurance, taxes, and home improvement loan payments) below 28% of gross monthly income. This guideline ensures adequate funds remain for other expenses, savings, and unexpected costs.

Monthly budget allocation framework:

- Housing (including loan payment): 28% maximum

- Transportation: 15-20%

- Food and household: 10-15%

- Utilities: 5-10%

- Savings and emergency fund: 10-15%

- Discretionary spending: 5-10%

- Other debt: 10-15%

Building Emergency Reserves

Before committing to renovation financing, establish or maintain an emergency fund covering 3-6 months of essential expenses. This financial cushion protects you if income disruption occurs during loan repayment.

Understanding Prepayment Options

Many personal loans allow prepayment without penalties, enabling you to reduce interest costs by paying more than the minimum or paying off the balance early. Review your loan agreement to understand prepayment rights and restrictions.

Accelerated repayment strategies include:

- Bi-weekly payments (26 half-payments yearly instead of 12 full payments)

- Rounding up (pay $550 instead of $531, applying excess to principal)

- Windfall application (directing bonuses, tax refunds, or gifts to loan balance)

- Budget surplus allocation (routing monthly spending remainder to debt)

These approaches reduce total interest paid and shorten loan terms without formally refinancing.

Access and Equity in Home Improvement Lending

Research reveals concerning disparities in access to home improvement financing across different communities. Analysis of Home Mortgage Disclosure Act data highlights how demographic factors influence approval rates and terms offered to borrowers.

Addressing Historical Barriers

Traditional lending institutions have historically underserved certain communities, creating obstacles to home maintenance and value preservation. These barriers include:

- Stricter underwriting for minority borrowers

- Limited branch presence in certain neighborhoods

- Documentation requirements that disadvantage self-employed applicants

- Credit scoring models that penalize non-traditional credit histories

Consumer lenders committed to financial inclusion actively work to overcome these barriers through flexible underwriting, community presence, and specialized products for underserved markets.

Alternative Credit Evaluation

Progressive lenders consider factors beyond traditional credit scores, including:

- Consistent payment history on rent and utilities

- Employment stability and income trajectory

- Cash reserves and savings patterns

- Co-borrower or co-signer creditworthiness

- Relationship history with the financial institution

This comprehensive evaluation provides opportunities for creditworthy borrowers who might not meet conventional standards.

Protecting Yourself From Predatory Lending

Unfortunately, home improvement financing attracts predatory lenders who exploit desperate homeowners. Recognizing warning signs protects you from harmful loan products.

Red Flags to Avoid

Pressure tactics: Legitimate lenders allow time for careful consideration. High-pressure sales tactics demanding immediate decisions signal problematic lending practices.

Excessive fees: While all loans involve costs, excessive origination fees, processing charges, or prepayment penalties indicate potential exploitation.

Unclear terms: Professional lenders provide clear, written explanations of all loan terms, rates, and fees. Vague or constantly changing terms suggest deceptive practices.

Unsolicited offers: Be extremely cautious with unexpected contact from lenders you haven't researched, especially those guaranteeing approval without reviewing your financial situation.

Balloon payments: Loans requiring large final payments create refinancing dependence and potential property loss if you cannot pay or refinance when due.

Verification Steps

Before signing any loan agreement:

- Research the lender through Better Business Bureau and state regulators

- Review all documents thoroughly before signing

- Understand the total cost of borrowing, not just monthly payments

- Verify licensing and registration in your state

- Compare offers from multiple reputable lenders

- Consult with trusted advisors if anything seems unclear

Making Your Decision

Choosing the right home improvement financing requires balancing multiple factors specific to your situation, project needs, and financial goals.

Decision Framework

Evaluate options using these criteria:

| Priority | Questions to Consider |

|---|---|

| Affordability | Can I comfortably make monthly payments? Does this fit my budget? |

| Timeline | How quickly do I need funds? When does the project need to start? |

| Flexibility | Might project costs change? Do I need access to additional funds? |

| Risk Tolerance | Am I comfortable using my home as collateral? What happens if I cannot pay? |

| Total Cost | What will I pay in total interest? How does this compare to alternatives? |

Working With Experienced Lenders

Partnering with established consumer lenders brings expertise, transparency, and support throughout the borrowing process. Look for institutions with:

- Strong regional presence and community connections

- Flexible qualification criteria that consider full financial pictures

- Clear communication about terms, rates, and fees

- Responsive customer service during application and repayment

- Positive customer reviews and regulatory compliance records

These characteristics indicate lender commitment to ethical practices and customer success.

Home improvement financing opens doors to necessary repairs and valuable upgrades that enhance both comfort and property value. Whether you need funds for essential maintenance or exciting renovations, understanding your options empowers informed decisions aligned with your financial circumstances and goals. Standard Financial serves homeowners throughout Louisiana, Mississippi, Tennessee, and Georgia with flexible personal loan solutions designed for renovation projects of all sizes, offering accessible financing even for those with past credit challenges. Our experienced team provides personalized guidance to help you find the right financing solution for transforming your house into the home you envision.

No comment yet, add your voice below!