Finding reliable financing when your credit history isn't perfect can feel overwhelming. Many borrowers with past credit challenges discover that bad credit installment loans online direct lenders provide a practical pathway to securing funds without traditional banking obstacles. These specialized lenders focus on your current financial situation rather than past mistakes, offering structured repayment plans that help rebuild credit while meeting immediate financial needs. Understanding how direct lenders operate and what to expect from the application process empowers you to make informed decisions about your financial future.

Understanding Bad Credit Installment Loans

Bad credit installment loans differ significantly from traditional bank loans in their approval criteria and structure. These loans allow borrowers to receive a lump sum upfront and repay it through fixed monthly payments over a predetermined period. The installment structure creates predictability in budgeting, since you know exactly how much you'll pay each month until the loan is satisfied.

Direct lenders specializing in bad credit borrowers evaluate applications using alternative criteria beyond credit scores. They consider your current income, employment stability, debt-to-income ratio, and overall financial picture. This comprehensive approach means that past credit issues don't automatically disqualify you from approval.

Key features of these loans include:

- Fixed monthly payments throughout the loan term

- Loan amounts typically ranging from $1,000 to $10,000

- Repayment periods from 6 months to 5 years

- Interest rates based on individual risk assessment

- Direct communication with the funding source

The term "direct lender" is crucial because it means you're working with the actual company providing the funds, not a broker or intermediary. This direct relationship often results in faster processing, clearer communication, and potentially better terms since there's no middleman markup.

How Online Direct Lenders Evaluate Applications

The application process with bad credit installment loans online direct lenders has evolved significantly in recent years. Most lenders now offer completely digital experiences, from initial application to fund disbursement. This technological advancement benefits borrowers who need quick decisions and fast access to funds.

Application Requirements

Direct lenders typically require specific documentation to process your application efficiently. Being prepared with these items accelerates approval timelines and demonstrates financial responsibility.

Standard documentation includes:

- Valid government-issued identification

- Proof of steady income (pay stubs, bank statements, or tax returns)

- Active checking or savings account information

- Current contact information and address verification

- Social Security number for identity verification

Approval Factors Beyond Credit Scores

While your credit score remains a consideration, direct lenders weight other factors heavily. Your current income relative to your monthly obligations often matters more than past payment history. Lenders want confidence that you can afford the monthly payment without financial strain.

Employment history plays a significant role in approval decisions. Borrowers with stable employment for six months or longer typically receive more favorable consideration. Self-employed individuals can qualify by providing tax returns or bank statements showing consistent income patterns.

| Evaluation Factor | Weight in Decision | What Lenders Look For |

|---|---|---|

| Income Verification | High | Steady monthly earnings exceeding $1,500 |

| Debt-to-Income Ratio | High | Total debt payments below 45% of income |

| Employment Stability | Medium | 6+ months with current employer |

| Credit Score | Medium | Typically accept scores below 580 |

| Banking Relationship | Low | Active account in good standing |

Understanding how installment loans work for bad credit borrowers helps set realistic expectations about approval odds and loan terms you might receive.

Comparing Interest Rates and Terms

Interest rates on bad credit installment loans online direct lenders vary significantly based on multiple factors. Borrowers should expect higher rates than those with excellent credit, but competitive shopping can still yield substantial savings over the life of the loan.

Rate Ranges in 2026

The current lending environment shows APRs for bad credit installment loans typically ranging from 18% to 36%, though some lenders charge higher rates depending on state regulations and individual risk profiles. These rates reflect the increased risk lenders assume when working with borrowers who have challenged credit histories.

Factors influencing your specific rate:

- Credit score (higher scores receive better rates)

- Loan amount requested

- Repayment term length

- Income level and stability

- State lending regulations

- Existing relationship with the lender

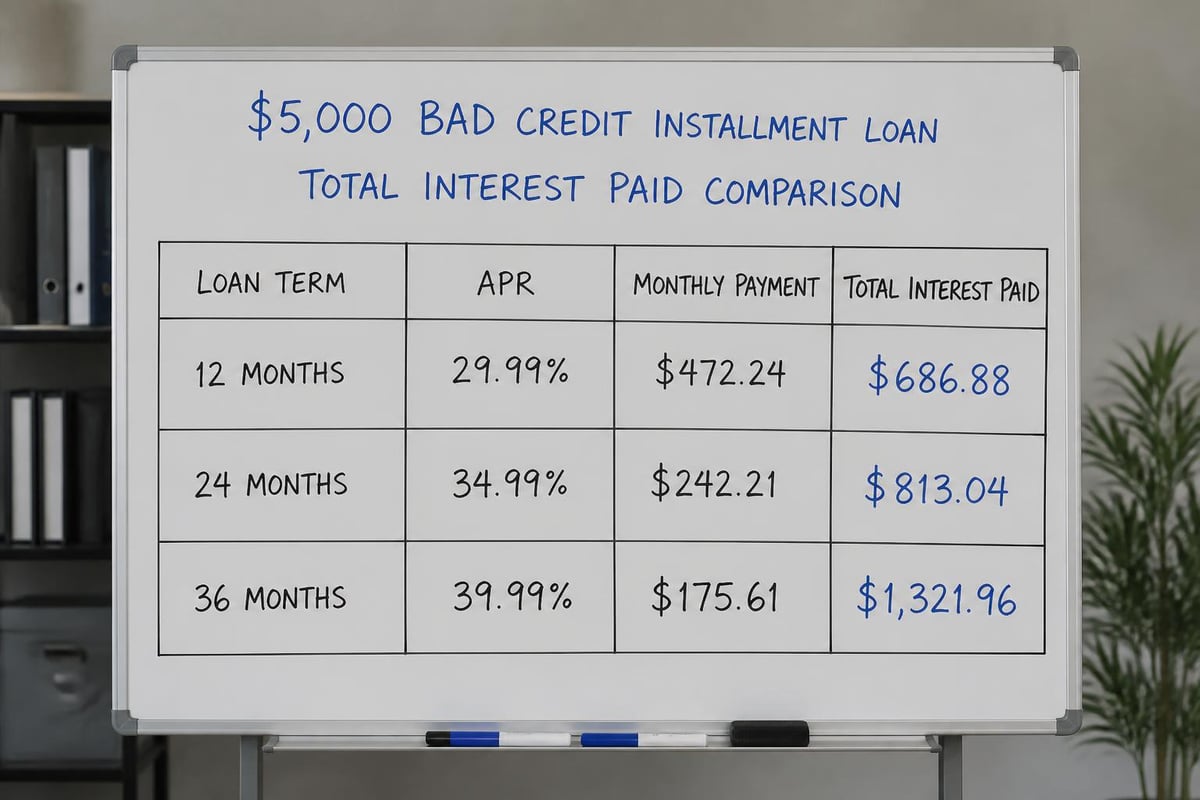

Shorter repayment terms generally come with lower interest rates but higher monthly payments. A 12-month loan might carry a 22% APR while a 36-month loan could be 28% APR. The total interest paid differs dramatically based on this choice.

Understanding the True Cost

Looking beyond the APR to the total amount you'll repay provides clarity on the loan's true cost. A $5,000 loan at 24% APR over 24 months results in monthly payments of approximately $261 and total repayment of $6,264. That same loan extended to 36 months at 26% APR drops the monthly payment to $186 but increases total repayment to $6,696.

Benefits of Working With Direct Lenders

Choosing bad credit installment loans online direct lenders over broker networks or storefront operations offers distinct advantages. The direct relationship eliminates confusion about who holds your loan and where to direct questions or concerns.

Faster Processing and Funding

Direct lenders control their entire approval pipeline, enabling quicker decisions. Many online direct lenders provide approval decisions within minutes and fund approved loans within one business day. This speed proves invaluable when facing urgent expenses like medical bills, car repairs, or unexpected home maintenance.

Traditional banks often take weeks to process loan applications, requiring multiple rounds of documentation and in-person meetings. Direct lenders streamline this process through automated verification systems and digital document submission.

Transparent Communication

Working directly with the funding source eliminates the confusion that occurs when brokers shop your application to multiple lenders. You know exactly who's reviewing your information, what terms they're offering, and how to contact them with questions. This transparency builds trust and simplifies the borrowing experience.

Additional benefits include:

- Single point of contact for all loan-related questions

- Clearer understanding of repayment expectations

- Ability to negotiate terms directly

- Simplified refinancing options with the same lender

- Consistent customer service experience

Credit Building Opportunities

Responsible repayment of installment loans helps rebuild damaged credit. Direct lenders typically report payment activity to major credit bureaus, meaning your on-time payments contribute positively to your credit history. Over time, this positive reporting can improve your score and expand your future financing options.

Making payments early or paying more than the minimum demonstrates financial responsibility and reduces total interest paid. Some borrowers use strategies recommended by personal finance experts to accelerate debt repayment and credit improvement simultaneously.

Application Strategy for Success

Approaching bad credit installment loans online direct lenders with a strategic mindset increases approval odds and improves the terms you receive. Preparation and understanding what lenders seek separates successful applicants from those who face repeated rejections.

Pre-Application Steps

Before submitting applications, take time to understand your current financial position. Pull your credit reports from all three bureaus to identify any errors that might be unfairly lowering your score. Disputing inaccuracies can sometimes boost your score quickly, leading to better loan terms.

Calculate your debt-to-income ratio by dividing your total monthly debt payments by your gross monthly income. If this ratio exceeds 45%, consider ways to reduce it before applying. Paying down existing balances or increasing income through side work improves this crucial metric.

- Review credit reports for errors and dispute inaccuracies

- Calculate current debt-to-income ratio

- Gather required documentation in digital format

- Research lender-specific requirements and preferences

- Determine realistic loan amount needed

- Identify comfortable monthly payment range

Choosing the Right Loan Amount

Borrowing only what you genuinely need demonstrates financial prudence to lenders and keeps your monthly obligations manageable. Requesting excessive amounts raises red flags about your ability to repay and often results in denial or less favorable terms.

Consider your specific need carefully. If you need $3,500 for car repairs, requesting $5,000 "just in case" increases your debt burden unnecessarily. Precision in loan requests shows lenders you've thought carefully about your financial needs.

Comparing Multiple Direct Lenders

While having too many credit inquiries can temporarily lower your score, shopping for loans within a concentrated timeframe (typically 14-45 days) usually counts as a single inquiry for scoring purposes. Use this window to compare offerings from several direct lenders.

| Comparison Factor | Why It Matters | What to Compare |

|---|---|---|

| APR | Total borrowing cost | Lowest rate for your situation |

| Monthly Payment | Budget impact | Affordability over loan term |

| Loan Term Options | Flexibility | Range of repayment periods offered |

| Funding Speed | Urgency of need | Time from approval to disbursement |

| Customer Reviews | Service quality | Borrower satisfaction ratings |

| Prepayment Penalties | Flexibility | Ability to pay off early without fees |

Common Pitfalls to Avoid

Understanding potential mistakes helps borrowers navigate the bad credit installment loan landscape more successfully. Many applicants unknowingly sabotage their chances through preventable errors.

Avoiding Predatory Lenders

Not all online lenders operate with borrower interests in mind. Predatory lenders disguise themselves as legitimate operations while charging excessive fees and unreasonable terms. Warning signs include pressure to act immediately, requests for upfront fees before approval, and unwillingness to clearly explain terms.

Red flags indicating predatory practices:

- Guaranteed approval regardless of credit or income

- Requests for payment before loan disbursement

- Vague or confusing loan terms

- No physical address or phone contact information

- Pressure tactics to sign immediately

- Fees that seem excessive compared to loan amount

Legitimate bad credit installment loans online direct lenders clearly state their terms, provide multiple contact methods, and comply with state lending regulations. They never guarantee approval or request upfront payments.

Understanding State Regulations

Lending laws vary significantly by state, affecting maximum interest rates, loan amounts, and term lengths. Some states cap APRs at 36%, while others allow higher rates. Understanding your state's regulations helps you recognize when a lender's terms exceed legal limits.

Borrowers in Louisiana, Mississippi, Tennessee, and Georgia benefit from specific state protections governing consumer lending practices. Familiarizing yourself with these regulations ensures you're working with compliant lenders offering legal loan products.

Reading the Fine Print

Loan agreements contain crucial details about your obligations and rights. Many borrowers skip these documents, assuming standard terms apply. This oversight can lead to surprise fees, prepayment penalties, or misunderstood payment schedules.

Pay special attention to sections covering late payment fees, returned payment charges, and any penalties for early repayment. Understanding these provisions prevents costly mistakes and helps you budget accurately for loan repayment.

Alternative Uses for Installment Loans

While many borrowers seek bad credit installment loans online direct lenders for emergency expenses, these financial tools serve multiple purposes. Understanding various applications helps you maximize the value of borrowed funds.

Home Improvement Financing

Installing new HVAC systems, repairing roofs, or updating electrical systems protects your home's value and your family's safety. Installment loans provide the upfront capital for these projects with repayment terms that don't strain monthly budgets.

Unlike credit cards with variable rates, installment loans lock in fixed rates and payments. This predictability helps homeowners budget for improvements while knowing exactly when the obligation ends.

Medical Expense Management

Healthcare costs continue rising, and many procedures or treatments aren't fully covered by insurance. Installment loans help bridge the gap between what insurance pays and what you owe, preventing medical debt from damaging your credit or forcing delayed treatment.

Medical providers increasingly work with patients who can demonstrate financing arrangements. Having approved loan funds gives you leverage to negotiate better payment terms or cash discounts with healthcare providers.

Education and Career Development

Investing in professional certifications, specialized training, or continuing education can significantly boost earning potential. When these programs don't qualify for traditional student loans, installment loans fill the financing gap.

The structured repayment schedule aligns well with education financing, since you can complete training and potentially increase income before the loan fully matures. This creates a positive return on investment that justifies the borrowing cost.

Debt Consolidation Strategy

Borrowers juggling multiple high-interest debts sometimes use installment loans to consolidate balances into a single monthly payment. This strategy works when the consolidation loan's APR is lower than the weighted average of existing debts and when you commit to not accumulating new debt.

Successful debt consolidation requires discipline and planning. Resources about installment loans for bad credit can help you evaluate whether this strategy makes financial sense for your situation.

Building Long-Term Financial Health

Securing a loan represents just one step in improving your overall financial picture. Borrowers who view bad credit installment loans online direct lenders as part of a broader financial strategy position themselves for lasting success.

Creating a Repayment Plan

Before accepting any loan offer, map out your repayment strategy. Identify which expenses you can reduce to ensure comfortable monthly payments. Building a small buffer into your budget prevents missed payments when unexpected expenses arise.

Successful repayment strategies include:

- Setting up automatic payments to avoid missed deadlines

- Paying slightly more than the minimum when possible

- Maintaining an emergency fund separate from loan proceeds

- Tracking payment history to monitor credit improvement

- Communicating with lenders immediately if payment difficulties arise

Monitoring Credit Progress

Regular credit monitoring helps you track improvement resulting from on-time installment loan payments. Free credit monitoring services provide monthly updates showing how your score changes over time. Watching this upward trajectory provides motivation to continue responsible financial behaviors.

Most borrowers see noticeable credit score improvements within 6-12 months of consistent, on-time installment loan payments. This improvement expands future financing options and reduces borrowing costs as you qualify for better rates.

Planning for Future Financial Needs

Once you've successfully repaid an installment loan, you've established a positive relationship with that direct lender. Many lenders offer better terms to returning customers with proven repayment histories. This relationship becomes valuable when future financing needs arise.

Consider how today's borrowing decision affects tomorrow's opportunities. Choosing responsible loan amounts, making consistent payments, and eventually paying off the loan completely creates a foundation for improved financial flexibility.

Navigating the landscape of bad credit installment loans online direct lenders requires careful research, realistic self-assessment, and strategic decision-making, but the right loan can provide crucial financial support while helping rebuild your credit profile. If you're looking for a lender that understands the challenges of past credit issues and offers flexible financing solutions tailored to your needs, Standard Financial serves borrowers across Louisiana, Mississippi, Tennessee, and Georgia with transparent terms and personalized service designed to help you achieve your financial goals.

No comment yet, add your voice below!