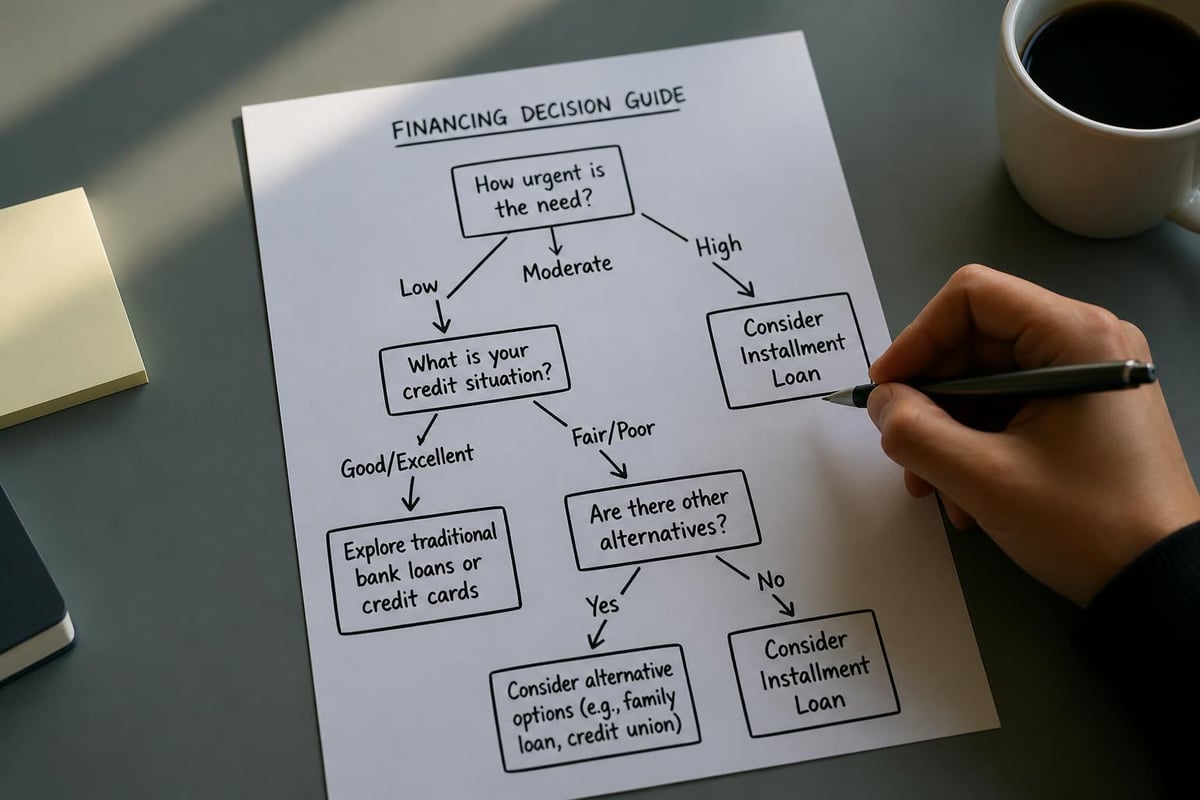

Finding financial solutions when you're facing credit challenges can feel overwhelming. Many borrowers search for no credit check installment loans guaranteed approval when traditional banks turn them away. While the term "guaranteed approval" is misleading in the lending industry, there are legitimate options available for consumers with less-than-perfect credit histories. Understanding how these loans actually work, what lenders really evaluate, and how to protect yourself from predatory practices is essential before moving forward with any financing decision.

Understanding No Credit Check Installment Loans

No credit check installment loans represent a category of personal financing that uses alternative underwriting methods to evaluate borrowers. Instead of relying exclusively on FICO scores and traditional credit bureau reports, these lenders assess your ability to repay based on current income, employment stability, and banking history.

The installment structure means you'll repay the loan through fixed monthly payments over a predetermined period. This differs significantly from payday loans, which typically require full repayment within two weeks. Installment terms commonly range from three months to five years, depending on the loan amount and lender policies.

How Alternative Underwriting Works

Lenders who offer these products typically conduct soft credit inquiries that won't damage your credit score. They focus instead on verifiable income sources and current financial capacity. Some use proprietary algorithms that analyze:

- Bank account transaction history

- Employment verification and length of service

- Debt-to-income ratio calculations

- Payment history on utility bills and rent

- Recent financial behavior patterns

This approach allows people with limited credit history or past financial setbacks to access funding. As explained by OppLoans, their bank partners assess applicants without relying solely on FICO scores, making loans accessible to a broader range of consumers.

The Truth About Guaranteed Approval Claims

The phrase "guaranteed approval" attracts desperate borrowers, but legitimate lenders cannot and do not guarantee approval to every applicant. Responsible lending requires evaluating each borrower's ability to repay, as required by federal lending regulations and state consumer protection laws.

Why Legitimate Lenders Cannot Guarantee Approval

Financial institutions must comply with regulations designed to prevent predatory lending and ensure borrower protection. These requirements mean lenders must verify:

Basic eligibility criteria:

- Minimum age requirements (typically 18 years old)

- Proof of steady income source

- Active checking account in good standing

- Valid contact information and identification

- Residency in states where the lender operates

Even with flexible underwriting standards, lenders must ensure you can afford the loan payments without creating financial hardship. According to Finder.com, legitimate lenders don't offer guaranteed approval, and such promises often signal predatory lending practices.

Red Flags to Watch For

When you encounter claims of no credit check installment loans guaranteed approval, exercise caution. Warning signs of predatory or fraudulent lenders include:

- Upfront fees before loan approval

- Pressure to act immediately without reviewing terms

- Lack of state licensing information

- No physical business address or customer service contact

- Guaranteed approval regardless of financial situation

- Interest rates exceeding state usury limits

Always verify a lender's credentials through your state's financial regulatory agency before sharing personal information or making payments.

Loan Amounts and Repayment Terms

The structure of no credit check installment loans varies considerably based on lender policies, state regulations, and individual borrower qualifications. Understanding typical offerings helps set realistic expectations.

Typical Loan Parameters

| Loan Feature | Common Range | Factors Affecting Terms |

|---|---|---|

| Loan Amount | $500 – $5,000 | Income level, state laws, lender policies |

| Repayment Period | 3 – 36 months | Loan amount, borrower preference, lender options |

| APR Range | 36% – 299% | Credit risk assessment, state regulations |

| Payment Frequency | Monthly | Some offer bi-weekly options |

| Origination Fees | 0% – 8% | Lender policies, loan amount |

Smaller loan amounts typically carry higher interest rates due to the fixed costs of loan origination and servicing. A $500 loan creates the same administrative burden as a $5,000 loan, so lenders compensate through higher APRs on smaller balances.

How Repayment Schedules Work

Installment loans provide predictable payment schedules that make budgeting easier than revolving credit or payday loans. Your monthly payment amount remains consistent throughout the loan term, with each payment allocated between principal reduction and interest charges.

Early in the loan term, a larger portion goes toward interest. As you progress through the repayment schedule, more of each payment reduces your principal balance. Many lenders allow early payoff without prepayment penalties, which can save significant interest charges.

Application Process and Approval Timeline

The streamlined application process represents one of the primary advantages of no credit check installment loans guaranteed approval searches. Most lenders have moved to digital platforms that expedite every stage from application to funding.

Step-by-Step Application Journey

1. Online Application Submission

Most applications require 5-10 minutes to complete. You'll provide personal identification information, employment details, income documentation, and banking information for deposit and payment processing.

2. Initial Review and Alternative Credit Assessment

Lenders review your application using their proprietary underwriting models. This typically involves soft credit inquiries and verification of the information you provided. Many lenders reach a preliminary decision within minutes.

3. Documentation Verification

You may need to submit supporting documents such as recent pay stubs, bank statements, or identification copies. Digital document upload through secure portals has replaced fax machines and mail delays.

4. Final Approval and Loan Agreement

Once approved, you'll receive loan terms including the exact interest rate, payment amount, payment schedule, and total repayment amount. Review these documents carefully before signing electronically.

5. Funding Disbursement

After accepting terms, funds typically transfer to your bank account within one to three business days. Some lenders offer same-day funding for approved applications submitted during business hours.

What Impacts Your Approval Odds

While these loans accommodate borrowers with credit challenges, certain factors still influence approval decisions:

- Income stability: Consistent employment or benefit payments demonstrate repayment capacity

- Banking relationship: Accounts in good standing without recent overdrafts signal financial responsibility

- Debt obligations: Excessive existing debt may limit additional borrowing capacity

- State regulations: Some states impose stricter lending requirements than others

- Previous loan performance: Past defaults or charge-offs with the same lender typically result in denial

Comparing Alternative Lending Options

No credit check installment loans represent just one solution for borrowers with credit challenges. Understanding all available options helps you select the most appropriate and affordable financing.

Alternative Financing Comparison

| Option | Pros | Cons | Best For |

|---|---|---|---|

| Credit Union Loans | Lower rates, member benefits | Membership required, harder approval | Those with membership eligibility |

| Secured Personal Loans | Lower rates, larger amounts | Requires collateral, risk of loss | Borrowers with assets to pledge |

| Payment Plans | No interest, direct arrangement | Limited availability, strict terms | Medical bills, retail purchases |

| Family Loans | Flexible terms, low/no interest | Relationship risks, informal structure | Those with supportive family |

| Cash Advances | Immediate access | Very high fees, short repayment | True emergencies only |

As discussed on CashAmericaToday, no credit check installment loans offer speed and simplicity that traditional loans cannot match, particularly for borrowers facing urgent financial needs.

When Installment Loans Make Sense

These loans work best for specific financial situations:

- Emergency expenses that cannot wait for credit repair

- Consolidating multiple payday loans into manageable payments

- Building payment history when you lack credit references

- Bridge financing between financial setbacks and recovery

- Unexpected repairs to vehicles or essential home systems

They're less appropriate for discretionary purchases, ongoing cash flow problems, or situations where free alternatives exist.

State Regulations and Regional Differences

Consumer lending regulations vary significantly across states, creating different experiences for borrowers depending on their location. Standard Financial serves customers across Louisiana, Mississippi, Tennessee, and Georgia, where distinct regulatory frameworks apply.

Regional Lending Landscape

Louisiana

Louisiana's lending laws permit installment loans with certain restrictions on interest rates and fees. The state requires lenders to maintain physical locations and proper licensing through the Louisiana Office of Financial Institutions.

Mississippi

Mississippi allows installment lending with caps on loan amounts for certain license types. Lenders must comply with the Mississippi Department of Banking and Consumer Finance regulations.

Tennessee

Tennessee regulates installment lenders under its flexible lending statute, which sets maximum loan amounts and fee structures. The Tennessee Department of Financial Institutions oversees lender licensing and compliance.

Georgia

Georgia maintains stricter payday lending restrictions but permits installment loans under specific licensing categories. The Georgia Department of Banking and Finance regulates consumer lenders operating in the state.

How Location Affects Your Loan

Your state of residence determines:

- Maximum loan amounts available to borrowers

- Interest rate caps and allowable fees

- Minimum and maximum loan terms permitted

- Collection practices lenders may use

- Cooling-off periods between loans

Always verify that any lender you're considering holds proper licensing in your state. State regulators maintain public databases of licensed lenders, which you can search before submitting applications.

Responsible Borrowing Strategies

Accessing no credit check installment loans guaranteed approval searches often stems from financial pressure, but borrowing responsibly protects your long-term financial health and prevents debt cycles.

Before You Borrow

Create a comprehensive budget that accounts for your loan payment alongside existing obligations. Calculate your debt-to-income ratio by dividing total monthly debt payments by gross monthly income. Financial experts recommend keeping this ratio below 36% for financial stability.

Budget evaluation checklist:

- List all monthly income sources

- Document all recurring expenses

- Identify expenses you can reduce or eliminate

- Calculate remaining funds after essentials

- Determine affordable loan payment amount

- Include buffer for unexpected expenses

Choosing the Right Loan Terms

Longer repayment periods create smaller monthly payments but increase total interest paid over the loan's life. Shorter terms mean higher payments but faster payoff and less interest. Consider both monthly affordability and total cost when selecting terms.

Run calculations comparing different scenarios. A $2,000 loan at 100% APR costs dramatically different amounts depending on the repayment schedule:

- 6-month term: ~$400 monthly payment, ~$400 total interest

- 12-month term: ~$220 monthly payment, ~$640 total interest

- 24-month term: ~$130 monthly payment, ~$1,120 total interest

Balance your cash flow needs against minimizing total borrowing costs. Choose the shortest term you can comfortably afford to minimize interest expenses.

Building Credit While Repaying

While no credit check installment loans guaranteed approval lenders may not require hard credit pulls initially, many report payment activity to credit bureaus. This creates opportunities to build positive credit history through on-time payments.

Maximizing Credit Building Benefits

Not all alternative lenders report to credit bureaus, so ask before borrowing if building credit is a goal. When lenders do report, your payment history contributes to 35% of your FICO score calculation, making consistent on-time payments valuable for credit improvement.

Credit building strategies:

- Set up automatic payments to avoid missed due dates

- Pay more than the minimum when possible to reduce principal faster

- Monitor your credit reports quarterly for accurate reporting

- Avoid taking multiple loans simultaneously

- Keep debt utilization below 30% across all accounts

Moving Toward Traditional Credit

Successfully repaying installment loans demonstrates creditworthiness to future lenders. After establishing six to twelve months of positive payment history, explore graduating to traditional credit products with lower interest rates.

Consider applying for a secured credit card, which requires a deposit but reports to major credit bureaus. Combine this with your installment loan payments to build a diverse credit mix, which accounts for 10% of your credit score.

Managing Loan Payments Successfully

Staying current on your installment loan protects you from late fees, potential collection activity, and credit damage if the lender reports to bureaus. Develop systems that ensure consistent, on-time payments throughout your loan term.

Payment Automation and Tracking

Most lenders offer automatic payment deduction from your checking account on scheduled due dates. This eliminates the risk of forgetting payments but requires maintaining sufficient funds in your account.

If you prefer manual payments, set calendar reminders five days before each due date. This provides time to transfer funds if needed and ensures payments process before deadlines.

Payment management best practices:

- Choose payment dates aligned with your income schedule

- Maintain a payment buffer in your checking account

- Review account statements monthly for accuracy

- Contact your lender immediately if you anticipate payment difficulty

- Document all payments and communications with your lender

Handling Financial Setbacks

Life circumstances change, and you may face temporary inability to make scheduled payments. Contact your lender before missing payments rather than avoiding communication. Many lenders offer hardship programs, payment extensions, or refinancing options for borrowers experiencing temporary difficulties.

Proactive communication often results in workable solutions, while avoiding lenders leads to accelerated collection efforts and potential legal action. Remember that lenders prefer receiving payments to pursuing collections, creating motivation to work with borrowers facing genuine hardship.

Direct Lenders Versus Loan Marketplaces

When searching for no credit check installment loans guaranteed approval, you'll encounter both direct lenders and loan matching services. Understanding the distinction helps you navigate the application process efficiently and protect your personal information.

Direct Lender Advantages

Direct lenders fund loans using their own capital and make underwriting decisions internally. Working with direct lenders means:

- Single application processed by one company

- Direct communication about your loan status and terms

- Clear accountability for customer service and compliance

- Streamlined process without information sharing across networks

- Consistent experience from application through payoff

Standard Financial operates as a direct lender, providing face-to-face service through branch locations across four states while also offering online application convenience.

Understanding Loan Matching Services

Loan marketplaces collect your information and distribute it to multiple lenders seeking borrowers. While this creates potential access to various offers, it also means:

- Your information reaches multiple companies simultaneously

- You may receive numerous calls and emails from different lenders

- Each lender applies their own underwriting standards

- Privacy policies vary across the network

- Multiple soft inquiries may appear on credit monitoring services

Neither approach is inherently superior, but direct lenders typically provide more straightforward experiences with greater privacy protection for your financial information.

Total Cost Analysis and Comparison

High-interest rates on no credit check installment loans guaranteed approval products make total cost analysis essential. Understanding exactly how much you'll repay helps you make informed borrowing decisions and explore potential alternatives.

Calculating True Loan Costs

The Annual Percentage Rate (APR) represents the yearly cost of borrowing including interest and fees. However, focusing solely on APR without considering the dollar amount can be misleading for short-term loans.

Cost comparison example:

| Loan Details | Option A | Option B |

|---|---|---|

| Loan Amount | $1,500 | $1,500 |

| APR | 200% | 150% |

| Term Length | 6 months | 12 months |

| Monthly Payment | $337 | $195 |

| Total Repayment | $2,022 | $2,340 |

| Total Interest | $522 | $840 |

Option A carries a higher APR but costs less overall due to the shorter repayment period. Option B offers lower monthly payments but higher total interest charges. Your choice depends on whether monthly affordability or total cost takes priority in your situation.

Comparing Against Alternatives

Before accepting terms, compare the installment loan against other options available to you. Even if alternatives seem limited, quantifying costs helps validate your decision or identify better solutions you hadn't considered.

According to EasyFinance.com, fintech underwriting models create opportunities for competitive installment loan offers that can serve as practical alternatives to traditional credit when used appropriately.

Common Mistakes to Avoid

Borrowers searching for no credit check installment loans guaranteed approval often make preventable errors that increase costs or create additional financial stress. Learning from common mistakes helps you navigate the borrowing process more successfully.

Borrowing More Than Needed

The temptation to accept the maximum approved amount can be strong, especially when facing financial pressure. However, borrowing excess funds leads to:

- Higher monthly payments that strain your budget

- Increased total interest charges over the loan term

- Extended repayment obligations

- Greater financial burden if circumstances worsen

Borrow only the amount you genuinely need for your specific purpose. If approved for $3,000 but only need $2,000, decline the additional funds even though they're available.

Ignoring Alternative Solutions

Emergency situations create tunnel vision that prevents considering all available options. Before committing to a loan, exhaust free or lower-cost alternatives:

- Negotiate payment plans directly with creditors or service providers

- Sell unused items for quick cash through online marketplaces

- Pick up temporary work through gig economy platforms

- Request paycheck advances from employers who offer this benefit

- Access community assistance programs for specific needs like utilities or food

These alternatives may not provide complete solutions but can reduce the amount you need to borrow, lowering your total costs and repayment burden.

Failing to Read Loan Agreements

Loan agreements contain critical information about your obligations, rights, and potential penalties. Skimming terms or clicking acceptance without reading creates risk of unexpected costs and misunderstanding your commitments.

Pay particular attention to:

- Exact APR and how it's calculated

- Payment due dates and acceptable payment methods

- Late payment fees and grace periods

- Prepayment penalties if you pay early

- Default consequences and collection procedures

- Arbitration clauses affecting your legal rights

If terms are unclear, request clarification before signing. Legitimate lenders welcome questions and provide transparent answers about loan terms and conditions.

Understanding the realities of no credit check installment loans guaranteed approval helps you make informed decisions during financially challenging times. While true guaranteed approval doesn't exist with legitimate lenders, accessible options are available for borrowers with credit challenges who demonstrate current repayment capacity. If you're located in Louisiana, Mississippi, Tennessee, or Georgia and need flexible financing despite past credit issues, Standard Financial offers personalized loan solutions for home improvements, medical expenses, education, and other essential needs with professional service through multiple branch locations.

No comment yet, add your voice below!