Financial emergencies don't wait for perfect credit scores. When unexpected medical bills, car repairs, or home maintenance issues arise, many people in Louisiana, Mississippi, Tennessee, and Georgia find themselves searching for financing options that won't immediately reject them based on past credit mistakes. No credit check installment loans have emerged as a viable alternative for borrowers who need structured repayment terms without the anxiety of traditional credit scrutiny. These loan products evaluate applicants differently, focusing on current income and ability to repay rather than historical credit performance. Understanding how these loans work, their costs, and whether they align with your financial situation can help you make informed borrowing decisions.

Understanding No Credit Check Installment Loans

No credit check installment loans represent a category of personal financing that skips the traditional hard credit inquiry typically performed by banks and mainstream lenders. Instead of pulling your credit report from Equifax, Experian, or TransUnion, these lenders focus on alternative qualification criteria.

How the Approval Process Works

The application process for these loans prioritizes your current financial capacity over your credit history. Lenders typically verify:

- Current employment status and length of time with your employer

- Monthly income through pay stubs or bank statements

- Existing financial obligations through soft inquiries or self-disclosure

- Banking relationship demonstrating regular deposits and account management

- Identity verification through government-issued identification

This alternative approach means that a bankruptcy from three years ago or medical collections won't automatically disqualify you. Lenders want to see that you have steady income and can manage the monthly payments they're offering.

Types of Credit Checks Explained

It's important to understand that "no credit check" doesn't always mean zero credit review. The lending industry distinguishes between different types of credit inquiries that affect borrowers differently.

| Credit Check Type | Impact on Credit Score | What Lenders See | Common Use Cases |

|---|---|---|---|

| Hard Inquiry | Yes (5-10 points) | Full credit history | Traditional bank loans, mortgages |

| Soft Inquiry | No impact | Limited credit snapshot | Pre-qualifications, account monitoring |

| No Inquiry | No impact | No credit data accessed | Alternative installment loans |

Many lenders advertising no credit check installment loans actually perform soft inquiries or use alternative data sources. This allows them to assess risk without damaging your credit score, giving you the benefit of credit-friendly underwriting.

Benefits and Practical Applications

These financing products serve specific purposes for borrowers facing credit challenges. Understanding their advantages helps you determine if they match your situation.

Accessibility for Varied Credit Profiles

The primary advantage centers on accessibility. Traditional lenders might reject applicants with scores below 640, but no credit check installment loans open doors for:

- Individuals recovering from bankruptcy or foreclosure

- Young adults with limited credit history

- Self-employed workers with irregular income documentation

- Those with medical debt affecting their credit reports

- People who have avoided credit and lack a credit file

Standard Financial works with clients across Louisiana, Mississippi, Tennessee, and Georgia who have experienced past credit difficulties, recognizing that credit scores don't tell the complete story of financial responsibility.

Structured Repayment Plans

Unlike payday loans that demand full repayment within two weeks, installment loans provide structured monthly payments over extended periods. This structure offers several advantages:

- Predictable monthly budgeting with fixed payment amounts

- Longer repayment terms ranging from 6 to 60 months

- Larger loan amounts compared to single-payment alternatives

- Improved cash flow management without lump-sum repayment stress

A borrower might receive $3,000 for home repairs with 24 monthly payments of $150, making the expense manageable within their existing budget rather than creating a new financial crisis.

Speed and Convenience

Emergency situations require quick solutions. The application process for no credit check installment loans typically moves faster than traditional lending:

- Online applications completed in 10-15 minutes

- Approval decisions within hours, not days

- Fund disbursement within 1-2 business days

- Minimal documentation requirements compared to conventional loans

This speed proves invaluable when your car breaks down before your work shift or a medical emergency creates unexpected expenses.

Costs and Important Considerations

While accessibility provides clear benefits, borrowers must understand the costs associated with no credit check installment loans. These products typically carry higher interest rates than traditional bank loans, reflecting the increased risk lenders assume.

Interest Rates and APR

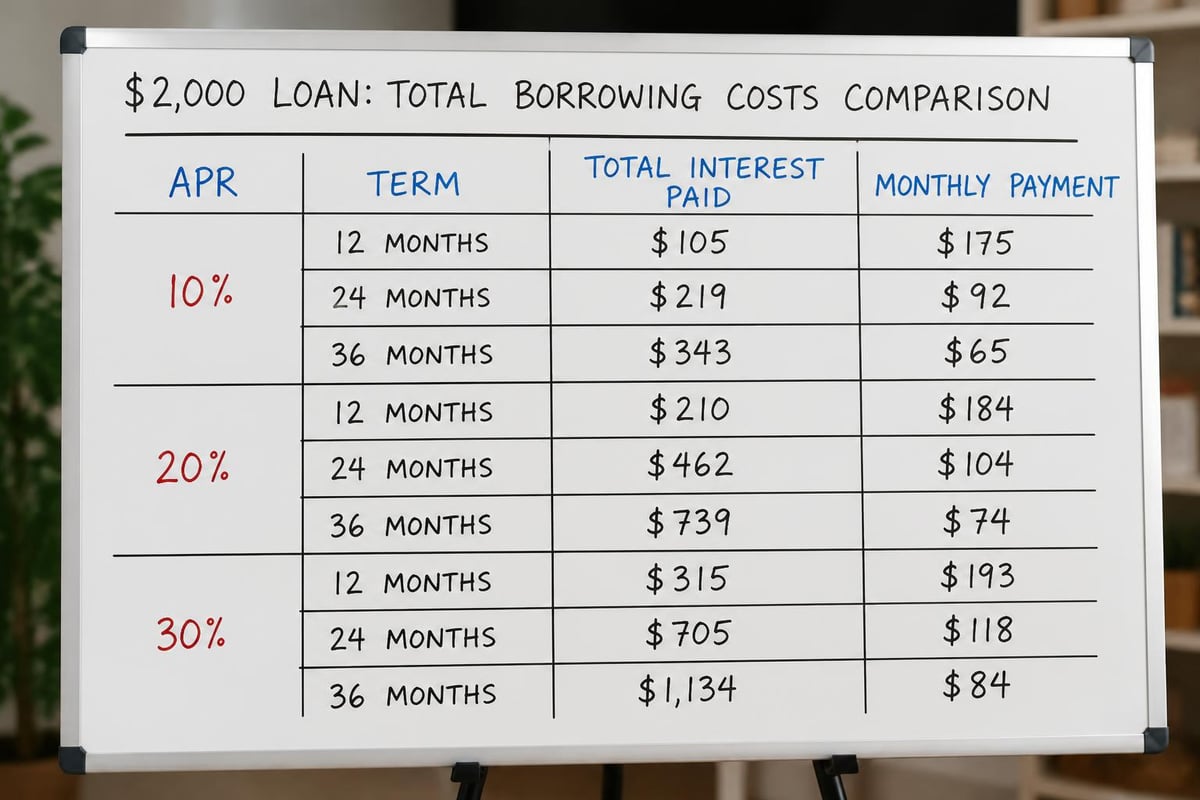

No credit check loans often feature higher APRs than credit-based lending products. Understanding these costs helps you make informed decisions:

- Traditional bank personal loans: 6% to 36% APR

- Credit union loans: 8% to 18% APR

- No credit check installment loans: 18% to 200%+ APR

- Payday loans: 300% to 500% APR

The specific rate you receive depends on loan amount, repayment term, state regulations, and the lender's assessment of your income stability. Always request the total cost of borrowing, including all fees, before accepting any loan offer.

Fee Structures to Watch

Beyond interest rates, pay attention to potential fees that increase borrowing costs:

| Fee Type | Typical Amount | When Charged | Avoidability |

|---|---|---|---|

| Origination Fee | 1% to 8% of loan | At disbursement | Sometimes negotiable |

| Late Payment Fee | $15 to $50 | Missed payment | Avoidable with on-time payment |

| Prepayment Penalty | Varies widely | Early payoff | Check loan agreement |

| NSF Fee | $25 to $40 | Bounced payment | Avoidable with sufficient funds |

Responsible lenders provide transparent fee schedules upfront. Understanding these cost components helps you calculate the true expense of borrowing and compare offers effectively.

State Regulations and Protections

Borrowers in Louisiana, Mississippi, Tennessee, and Georgia benefit from state-specific lending regulations that establish maximum interest rates and fee caps. These laws vary significantly:

Louisiana, for instance, has specific regulations governing consumer loans, while Tennessee and Georgia maintain different consumer protection frameworks. Always verify that your lender operates legally within your state and complies with applicable lending laws.

Qualifying for No Credit Check Installment Loans

Meeting eligibility requirements ensures smoother application experiences and better approval odds. While specific criteria vary by lender, common requirements include:

Basic Eligibility Criteria

Most lenders require applicants to meet fundamental qualifications:

- Minimum age of 18 years (21 in some states)

- U.S. citizenship or permanent residency

- Valid government-issued identification

- Active checking account in good standing

- Verifiable income source

- Working phone number and email address

- Residential address (not P.O. Box)

These baseline requirements establish that you're legally able to enter contracts and have the means to receive and repay funds.

Income Documentation

Since these loans focus on repayment ability rather than credit history, income verification becomes critical. Prepare to provide:

- Recent pay stubs covering the last 30-60 days

- Bank statements showing regular deposits

- Tax returns for self-employed applicants

- Proof of government benefits if applicable

- Employment verification through contact information

Self-employed individuals and those with irregular income may face additional documentation requirements but can still qualify with proper financial records.

Debt-to-Income Considerations

Even without traditional credit checks, lenders evaluate your debt-to-income ratio to ensure you can manage additional monthly obligations. This calculation compares your monthly debt payments to your gross monthly income.

A borrower earning $3,000 monthly with $900 in existing debt payments has a 30% debt-to-income ratio. Adding a $200 installment loan payment would increase that to 36.7%. Most lenders prefer ratios below 40-45%, though requirements vary.

Choosing the Right Lender

Not all no credit check installment loans offer equal terms or operate with the same ethical standards. Selecting a reputable lender protects you from predatory practices.

Red Flags to Avoid

Watch for warning signs that indicate potentially problematic lenders:

- Guaranteed approval regardless of circumstances

- Requests for upfront fees before loan approval

- Pressure to decide immediately without reviewing terms

- Vague or missing licensing information

- No physical address or customer service contact

- Unwillingness to provide written loan agreements

- Terms that seem too good to be true

Legitimate lenders, including established consumer lending companies with physical branch locations, provide transparent information and reasonable time to review agreements.

What to Look for in Quality Lenders

Reputable lenders demonstrate specific characteristics:

Transparency: Clear disclosure of all rates, fees, and terms before you commit.

Licensing: Proper state licensing and compliance with local lending regulations.

Communication: Accessible customer service through multiple channels.

Flexibility: Willingness to work with borrowers experiencing temporary payment difficulties.

Reputation: Positive reviews from independent sources and regulatory compliance history.

Standard Financial maintains branch offices throughout Louisiana, Mississippi, Tennessee, and Georgia, providing face-to-face service and transparent lending practices for clients with various credit backgrounds.

Alternatives Worth Considering

Before committing to no credit check installment loans, explore other options that might offer better terms or lower costs.

Credit Union Alternatives

Many credit unions offer payday alternative loans (PALs) with more favorable terms:

- Lower interest rates (typically 8-18% APR)

- Smaller application fees

- Flexible repayment terms

- Credit-building opportunities

- Membership requirements may apply

These products specifically target members needing small-dollar loans without resorting to high-cost alternatives.

Secured Loan Options

If you have assets, secured loans might provide:

| Asset Type | Typical Loan Amount | Interest Rate Range | Approval Timeline |

|---|---|---|---|

| Vehicle Title | 25-50% of value | 25-300% APR | Same day |

| Savings Account | Up to 100% of balance | 2-8% APR | 1-2 days |

| Valuables | Varies by item | 5-25% monthly | Same day |

| Home Equity | Up to 80% of equity | 3-12% APR | 2-6 weeks |

Secured options typically offer lower rates because the asset reduces lender risk. However, defaulting means losing the pledged property.

Payment Plans and Negotiation

Before borrowing, consider negotiating directly with creditors:

- Medical providers often offer interest-free payment plans

- Utility companies may provide extended payment arrangements

- Property managers might accept partial payments during hardship

- Service providers could waive late fees in exchange for payment commitment

These arrangements avoid borrowing costs entirely while addressing the underlying financial need.

Responsible Borrowing Practices

Successfully managing no credit check installment loans requires strategic planning and disciplined execution.

Borrowing Only What You Need

The temptation to borrow maximum available amounts can create unnecessary debt. Instead:

Calculate your specific need, including a small buffer for unexpected expenses. If you need $1,800 for car repairs, borrowing $2,000 provides slight cushion without excessive additional interest. Borrowing $5,000 because it's available creates long-term payment obligations you might not need.

Creating a Repayment Strategy

Before accepting any loan, develop a clear repayment plan:

- Review your monthly budget and identify available funds

- Set up automatic payments to avoid late fees

- Prioritize this payment alongside essential expenses

- Consider making extra payments when possible to reduce interest

- Build an emergency fund to avoid future borrowing needs

Understanding the full terms of your installment loan helps you avoid surprises and stay on track with payments.

Building Long-Term Financial Health

Use this borrowing experience as a stepping stone toward improved financial stability:

Track your progress: Monitor your loan balance and celebrate milestones.

Improve credit simultaneously: If your lender reports to credit bureaus, on-time payments build positive history.

Create savings habits: Even $25 monthly builds a cushion for future emergencies.

Address underlying issues: Identify what created the financial need and develop strategies to prevent recurrence.

Explore financial education: Many community organizations offer free financial literacy programs.

Impact on Your Financial Future

Understanding how no credit check installment loans affect your broader financial picture helps you make strategic decisions.

Credit Reporting Considerations

Not all lenders report payment activity to credit bureaus. Ask your lender about their reporting practices:

- Full reporting: Payments appear on all three major credit bureaus

- Selective reporting: Only negative information (defaults) gets reported

- No reporting: Neither positive nor negative activity appears

If building credit matters to you, prioritize lenders who report positive payment history. This transforms a borrowing necessity into a credit-building opportunity.

Future Borrowing Implications

Successfully repaying no credit check installment loans can improve your options for future financing needs. Demonstrating responsible borrowing behavior, even outside traditional credit systems, establishes a track record that some lenders value.

Conversely, defaulting on these loans can trigger collection activities, potential legal action, and damage to your banking relationships. The consequences extend beyond credit scores to affect your overall financial access.

No credit check installment loans provide valuable access to financing for borrowers facing credit challenges, offering structured repayment terms and faster approval processes than traditional lending. While these products carry higher costs than conventional loans, they serve important purposes when used responsibly and compared carefully. Standard Financial understands that past credit difficulties don't define your current financial responsibility. With flexible financing options across Louisiana, Mississippi, Tennessee, and Georgia, we work with clients who need personal loans for home improvements, medical expenses, education, and more. Contact Standard Financial today to explore personalized lending solutions that fit your situation and budget.

No comment yet, add your voice below!