When you need to borrow money for home improvements, medical expenses, or education costs, understanding your loan options is essential. The choice between secured vs unsecured personal loans significantly impacts your interest rate, borrowing limits, and financial risk. This decision affects not only your immediate borrowing costs but also your long-term financial health and asset protection. Making an informed choice requires understanding how each loan type works, what lenders expect from borrowers, and which option aligns with your current financial situation.

Understanding the Fundamental Differences

Personal loans fall into two primary categories based on how they're structured and what lenders require as protection against default. Secured loans require you to pledge an asset as collateral, while unsecured loans rely entirely on your creditworthiness and promise to repay.

The collateral requirement creates a ripple effect throughout the entire loan structure. When you offer collateral, lenders face less risk because they can seize the asset if you stop making payments. This reduced risk translates into more favorable terms for borrowers, including lower interest rates and higher borrowing limits. Unsecured loans, by contrast, leave lenders with no direct claim to your assets, which they compensate for through stricter approval requirements and higher interest rates.

How Collateral Changes the Lending Equation

Collateral serves as a safety net for lenders, fundamentally altering the risk-reward calculation. Common forms of collateral include:

- Real estate (home equity loans or lines of credit)

- Vehicles (auto-secured personal loans)

- Savings accounts or certificates of deposit

- Investment accounts

- Valuable personal property (though less common)

When evaluating secured vs unsecured personal loans, borrowers must recognize that pledging collateral creates a direct link between the loan and their assets. Missing payments on a secured loan doesn't just damage your credit; it puts your property at risk of repossession or foreclosure.

Interest Rates and Cost Comparisons

The financial implications of choosing between secured vs unsecured personal loans extend far beyond the initial borrowing decision. Interest rates represent the most immediate and measurable difference between these loan types.

Secured personal loans typically offer interest rates ranging from 3% to 12%, depending on the borrower's credit profile and the collateral value. Unsecured personal loans generally carry rates between 6% and 36%, with the specific rate determined by credit scores, income stability, and debt-to-income ratios. This spread can translate into thousands of dollars in interest payments over the life of a loan.

| Loan Feature | Secured Loans | Unsecured Loans |

|---|---|---|

| Typical APR Range | 3% – 12% | 6% – 36% |

| Collateral Required | Yes | No |

| Approval Speed | Moderate (appraisal needed) | Fast |

| Borrowing Limits | Higher ($25,000+) | Lower ($1,000-$50,000) |

| Credit Requirements | More flexible | Stricter standards |

Real-World Cost Examples

Consider a $15,000 loan with a five-year repayment term. With a secured loan at 7% APR, your monthly payment would be approximately $297, with total interest of $2,820. The same loan as an unsecured product at 15% APR would cost $357 monthly, with total interest of $6,420. That $3,600 difference illustrates why understanding secured versus unsecured loan structures matters for your wallet.

For borrowers across Louisiana, Mississippi, Tennessee, and Georgia, these cost differences become especially significant when financing major expenses like home repairs after storm damage or consolidating high-interest debt.

Credit Requirements and Approval Criteria

Lenders evaluate secured vs unsecured personal loans through different risk assessment frameworks, leading to distinct approval standards for each loan type.

Secured Loan Requirements

Secured loans offer more accessibility for borrowers with imperfect credit histories. Because collateral reduces lender risk, approval becomes possible even with:

- Credit scores below 640

- Recent bankruptcy or foreclosure (typically after 2-3 years)

- High debt-to-income ratios

- Limited credit history

- Self-employment income

The collateral value becomes a primary consideration. Lenders typically allow borrowing up to 80% to 90% of the asset's appraised value, ensuring adequate protection against default.

Unsecured Loan Standards

Without collateral protection, lenders scrutinize your financial profile more carefully. Most unsecured personal loans require credit scores of 650 or higher, with the best rates reserved for scores above 720. Income verification becomes more stringent, and lenders examine your employment stability, existing debt obligations, and payment history across all credit accounts.

The impact of loan type on your credit profile extends beyond approval odds. Both secured and unsecured loans appear on your credit report, but how you manage them influences your score differently based on the loan structure and your payment behavior.

Borrowing Limits and Loan Terms

The amount you can borrow varies dramatically when comparing secured vs unsecured personal loans. This difference stems directly from the collateral backing secured products.

Secured loans often allow borrowing from $5,000 to $100,000 or more, limited primarily by the collateral value. Home equity loans or lines of credit can reach even higher amounts. Unsecured personal loans typically cap between $1,000 and $50,000, with most lenders limiting individual borrowers to $35,000 without collateral.

Repayment terms also differ significantly:

- Secured loans often extend from 5 to 15 years, allowing smaller monthly payments spread over longer periods

- Unsecured loans typically range from 1 to 7 years, with most clustering around 3 to 5 years

- Home equity products may stretch to 30 years for certain structures

The extended terms available with secured loans reduce monthly payment pressure but increase total interest costs. When financing education expenses or major home improvements in markets like Memphis or Atlanta, these longer terms provide budget flexibility despite higher cumulative costs.

Risk Assessment for Borrowers

Understanding your personal risk exposure is crucial when evaluating secured vs unsecured personal loans. The consequences of default vary dramatically between these loan structures.

Secured Loan Risks

Putting your assets on the line creates serious consequences if financial circumstances change:

- Asset loss: Defaulting means losing the collateral, whether that's your vehicle, home equity, or savings

- Foreclosure or repossession: Lenders can legally seize pledged property

- Deficiency balances: If the collateral sale doesn't cover the outstanding balance, you may still owe money

- Credit damage: Default still severely impacts your credit score, compounding the asset loss

These risks require careful consideration of your income stability and emergency fund adequacy before pledging collateral.

Unsecured Loan Consequences

While you won't lose specific assets, defaulting on unsecured debt brings its own challenges:

- Severe credit score damage (drops of 100+ points)

- Collection agency involvement

- Potential wage garnishment through court judgments

- Legal action and court costs

- Difficulty obtaining future credit for years

The key differences in borrower obligations highlight why matching loan type to your financial stability and risk tolerance matters more than simply chasing the lowest interest rate.

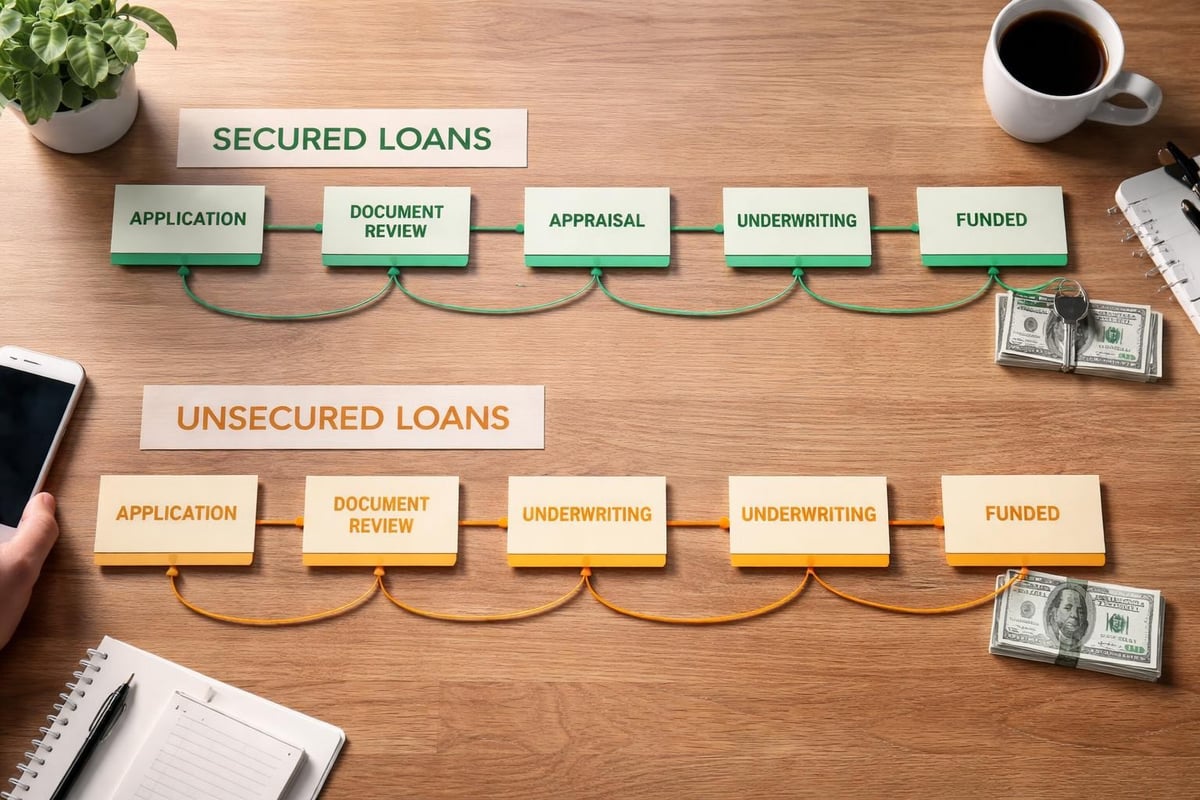

Application Process and Timeline

The mechanics of obtaining secured vs unsecured personal loans differ substantially, affecting how quickly you can access funds.

| Process Step | Secured Loans | Unsecured Loans |

|---|---|---|

| Initial Application | 30-45 minutes | 15-30 minutes |

| Collateral Appraisal | 1-2 weeks | Not required |

| Underwriting | 5-10 business days | 1-3 business days |

| Fund Disbursement | 2-4 weeks total | 1-7 days total |

| Documentation Required | Extensive (title, appraisal, insurance) | Moderate (income, ID, bank statements) |

Secured Loan Application Steps

Obtaining a secured personal loan involves several additional stages:

- Submit initial application with personal and financial information

- Provide collateral documentation (vehicle title, property deed, account statements)

- Complete collateral appraisal through lender-approved evaluators

- Review and sign security agreement legally pledging the asset

- Arrange required insurance (for vehicle or property collateral)

- Receive funds after all documentation is verified and recorded

Unsecured Loan Efficiency

The streamlined unsecured process eliminates appraisal delays. Many lenders now offer same-day or next-day funding for qualified borrowers, making unsecured loans ideal for urgent expenses like unexpected medical bills or emergency home repairs.

Refinancing and Flexibility Options

Your ability to refinance or modify loan terms depends partly on whether you initially chose secured vs unsecured personal loans. Both loan types offer refinancing opportunities, but the process and benefits differ.

Secured loan refinancing advantages:

- Access to additional funds through cash-out refinancing

- Potential to reduce interest rates if credit improves

- Option to extend terms for lower payments

- Ability to switch collateral in some cases

Unsecured loan refinancing benefits:

- Faster refinancing process without appraisals

- No collateral risk during the refinancing evaluation

- Simpler documentation requirements

- Easier lender switching for better rates

Borrowers across the Southeast often refinance personal loans as their financial situations improve. A Mississippi resident who initially needed a secured loan due to credit challenges might refinance to an unsecured product after two years of on-time payments and credit score improvement.

Choosing the Right Loan Type for Your Situation

Matching loan type to your specific circumstances requires honest assessment of several factors beyond just interest rates. Weighing the pros and cons of each loan structure helps clarify which option serves your needs.

When Secured Loans Make Sense

Consider secured personal loans if you:

- Need to borrow larger amounts ($25,000+)

- Have less-than-perfect credit (scores below 670)

- Want lower monthly payments through extended terms

- Can comfortably pledge collateral without risking essential assets

- Need financing for major projects like substantial home renovations

Many borrowers recovering from past credit issues find secured loans provide the only viable path to affordable financing for important expenses.

When Unsecured Loans Work Better

Unsecured personal loans suit situations where you:

- Need funds quickly (within days)

- Have strong credit (scores above 680)

- Prefer not to risk valuable assets

- Require moderate borrowing amounts ($5,000-$25,000)

- Want simpler application processes

For Tennessee or Georgia residents with stable employment and good credit seeking to consolidate high-interest credit card debt, unsecured personal loans often provide the optimal balance of speed, simplicity, and competitive rates.

Special Considerations for Different Borrower Profiles

Your personal circumstances significantly influence whether secured vs unsecured personal loans better serve your needs.

First-Time Borrowers

Building credit history presents unique challenges. Secured loans offer easier approval, helping establish positive payment history. Some lenders even report secured loan payments to all three credit bureaus, accelerating credit building. However, the collateral requirement means first-time borrowers must have assets to pledge.

Self-Employed Borrowers

Income documentation challenges make unsecured loans harder to obtain for self-employed individuals. Secured loans reduce the emphasis on income verification because collateral provides repayment assurance. Business owners across Louisiana and Mississippi frequently find secured options more accessible despite strong actual income.

Borrowers with Past Credit Issues

Previous bankruptcies, foreclosures, or charge-offs create barriers to unsecured credit. Secured loans provide a pathway to financing while rebuilding credit. The key is ensuring you can maintain consistent payments to avoid compounding past problems with new asset loss.

Regional Lending Considerations

Borrowers in Louisiana, Mississippi, Tennessee, and Georgia face specific market conditions affecting secured vs unsecured personal loans. State regulations, local economic factors, and regional lender competition all influence available terms.

Natural disaster risks in Gulf Coast states sometimes affect secured loan availability and terms, particularly for property-backed loans. Lenders may adjust loan-to-value ratios or require additional insurance in hurricane-prone areas. Conversely, strong regional economic growth in cities like Nashville and Atlanta creates competitive unsecured lending markets with favorable rates for qualified borrowers.

Understanding how collateral affects your loan obligations becomes especially important in markets where property values fluctuate or where economic conditions create employment uncertainty.

Impact on Long-Term Financial Health

The decision between secured vs unsecured personal loans reverberates through your financial life long after you've repaid the debt. Both loan types influence your credit utilization, payment history, and borrowing capacity for future needs.

Successfully managing either loan type builds positive credit history. However, secured loans demonstrate your ability to responsibly handle collateralized debt, which benefits future mortgage or auto loan applications. Unsecured loans prove creditworthiness without asset backing, valuable for credit card approvals and other unsecured products.

The key difference lies in recovery potential after financial setbacks. Defaulting on an unsecured loan damages credit severely but leaves assets intact for rebuilding. Secured loan default costs you both credit standing and valuable property, potentially setting back financial recovery by years.

Credit score factors affected by both loan types:

- Payment history (35% of FICO score)

- Credit utilization and debt levels (30%)

- Length of credit history (15%)

- Credit mix diversity (10%)

- New credit inquiries (10%)

Strategic use of either loan type within a broader financial plan strengthens your overall credit profile and borrowing power over time.

Choosing between secured vs unsecured personal loans requires balancing interest costs, approval likelihood, and personal risk tolerance based on your unique financial situation. Whether you need financing for home improvements, medical expenses, education costs, or debt consolidation, Standard Financial offers both secured and unsecured personal loan options across Louisiana, Mississippi, Tennessee, and Georgia, with flexible terms designed for borrowers at every credit level. Visit Standard Financial to explore your financing options and speak with a lending specialist who can help match you with the right loan structure for your needs.

No comment yet, add your voice below!