Managing multiple debts with varying interest rates, payment schedules, and creditors can feel overwhelming. When you're juggling credit card bills, medical expenses, and personal loans, keeping track of due dates and minimum payments becomes a full-time challenge. Debt consolidation loans offer a practical solution by combining multiple debts into a single monthly payment, often with a lower interest rate and more favorable terms. For residents across Louisiana, Mississippi, Tennessee, and Georgia dealing with financial stress, understanding how these loans work can be the first step toward regaining control of your finances.

Understanding How Debt Consolidation Loans Work

A debt consolidation loan is a financial tool that allows you to pay off multiple existing debts by taking out one new loan. This approach to managing debt through consolidation replaces several creditors and payment schedules with a single lender and one monthly payment.

The process typically involves borrowing enough money to pay off your existing debts completely. Once approved, the lender either pays your creditors directly or provides you with funds to settle the balances yourself. From that point forward, you make one monthly payment to your new lender instead of tracking multiple due dates and amounts.

The Mechanics Behind Consolidation

When you apply for debt consolidation loans, lenders evaluate your credit history, income, and existing debt obligations. They determine your eligibility and the interest rate you'll receive based on these factors. Even if you've experienced credit challenges in the past, many lenders offer options tailored to various credit situations.

The loan amount you receive should cover the total of your outstanding debts. Here's what typically gets consolidated:

- Credit card balances

- Medical bills

- Personal loans

- Payday loans

- Collection accounts

- Store financing accounts

Interest rates on consolidation loans generally range from 6% to 36%, depending on your creditworthiness and the lender's terms. Borrowers with stronger credit profiles usually qualify for rates on the lower end of this spectrum.

Key Benefits of Choosing Debt Consolidation

Simplifying your financial life stands as the most immediate advantage of debt consolidation loans. Instead of remembering five or six different payment dates each month, you focus on a single due date. This reduced complexity minimizes the risk of missed payments and late fees.

Financial Advantages Worth Considering

Lower interest rates often accompany consolidation loans, especially when you're replacing high-interest credit card debt. Credit cards frequently carry annual percentage rates (APR) between 18% and 29%, while consolidation loans may offer rates significantly below this range.

| Debt Type | Average APR | Potential Consolidation Rate |

|---|---|---|

| Credit Cards | 18-29% | 8-15% |

| Payday Loans | 400%+ | 8-15% |

| Medical Bills | 0-12% | 8-15% |

| Personal Loans | 10-28% | 8-15% |

Reduced monthly payments represent another compelling benefit. By extending your repayment term, you can lower your monthly obligation, freeing up cash flow for other essential expenses. However, remember that longer terms mean paying more interest over the life of the loan.

Your credit score may improve over time with responsible management of debt consolidation loans. As you pay down the consolidated balance and maintain on-time payments, your credit utilization ratio decreases and your payment history strengthens.

Stress Reduction and Mental Clarity

The psychological benefits shouldn't be underestimated. Managing multiple debts creates constant anxiety about which bills to prioritize and whether you'll have enough money to cover everything. Consolidation eliminates this mental burden, allowing you to focus on a single, predictable payment strategy.

Types of Debt Consolidation Options Available

Understanding the various debt consolidation options helps you choose the right approach for your situation. Different methods suit different financial circumstances and credit profiles.

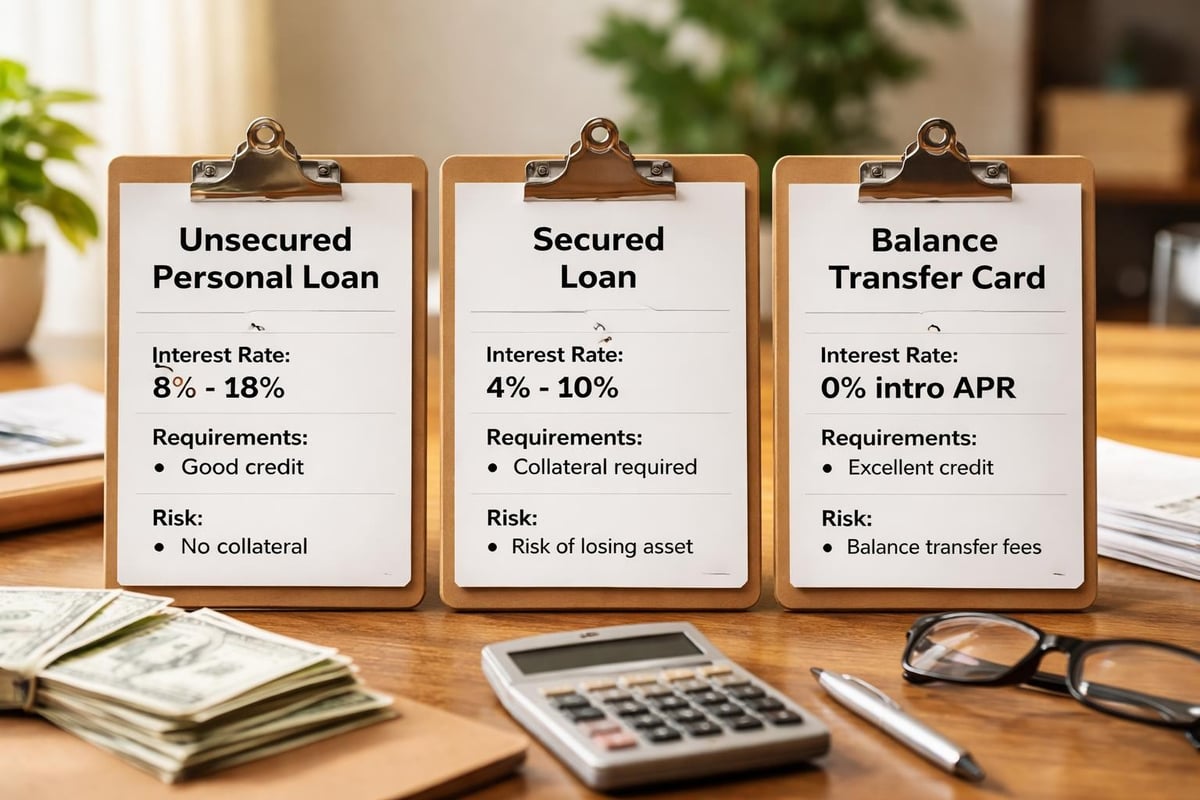

Unsecured Personal Loans

These loans don't require collateral, making them accessible for borrowers who don't own homes or prefer not to risk their assets. Approval depends primarily on your credit score, income verification, and debt-to-income ratio. Unsecured debt consolidation loans typically feature fixed interest rates and predictable monthly payments over terms ranging from two to seven years.

Lenders evaluate your ability to repay based on your employment history and income stability. For residents of Louisiana, Mississippi, Tennessee, and Georgia with steady employment, these loans offer a straightforward path to consolidation without risking property.

Secured Consolidation Loans

Secured loans require collateral such as a vehicle, savings account, or home equity. Because the lender has security in case of default, these loans often come with lower interest rates than unsecured options. Home equity loans or home equity lines of credit (HELOCs) fall into this category.

The trade-off involves risk. If you cannot make payments, the lender can seize the collateral to recover their losses. This makes secured loans less suitable for borrowers uncertain about their repayment ability.

Balance Transfer Credit Cards

Some borrowers use balance transfer credit cards offering 0% introductory APR periods for debt consolidation. This method works best when you can pay off the transferred balance before the promotional period ends, typically 12 to 21 months.

- Apply for a balance transfer card with favorable terms

- Transfer high-interest balances to the new card

- Pay aggressively during the 0% APR period

- Avoid new purchases on the card

- Pay off the balance before regular rates apply

Determining If Debt Consolidation Makes Sense

Not everyone benefits equally from debt consolidation loans. Assessing whether consolidation suits your financial situation requires honest evaluation of your circumstances and goals.

Ideal Candidates for Consolidation

You're likely a good candidate if you meet these criteria:

- You have multiple debts with high interest rates

- Your credit score qualifies you for better rates than you currently pay

- You have steady income to support monthly payments

- You're committed to avoiding new debt

- You struggle to track multiple payment schedules

Total debt amount matters too. Generally, consolidation makes most sense when you owe at least $5,000 to $10,000 across multiple accounts. Smaller amounts may not justify the application process and potential fees.

Warning Signs That Consolidation May Not Help

Certain situations suggest consolidation might not be your best option. If your debt stems from overspending habits you haven't addressed, consolidation simply postpones the problem. Without behavioral changes, you risk accumulating new debt on top of your consolidation loan.

Similarly, if your debt-to-income ratio exceeds 50%, you may struggle to qualify for favorable terms. In this case, alternatives like debt management plans or credit counseling might serve you better.

The Application Process for Debt Consolidation Loans

Securing debt consolidation loans involves several straightforward steps. Preparation increases your chances of approval and helps you obtain better terms.

Gathering Required Documentation

Lenders need to verify your identity, income, and financial obligations. Typical requirements include:

- Government-issued photo identification

- Proof of income (pay stubs, tax returns, bank statements)

- List of current debts with balances and account numbers

- Proof of residence (utility bill, lease agreement)

- Social Security number for credit check

Having these documents ready streamlines the application process and demonstrates your organizational skills to potential lenders.

Comparing Lender Offers

Don't accept the first offer you receive. Different lenders provide varying terms, interest rates, and fees. Request quotes from at least three to five lenders to ensure competitive pricing.

| Comparison Factor | Why It Matters | What to Look For |

|---|---|---|

| Interest Rate | Determines total cost | Lowest available rate for your credit tier |

| Loan Term | Affects monthly payment | Balance between affordability and total interest |

| Origination Fees | Upfront costs | 1-8% of loan amount or none |

| Prepayment Penalties | Early payoff flexibility | Avoid lenders that charge these fees |

Regional lenders with physical locations in Louisiana, Mississippi, Tennessee, and Georgia often provide personalized service and may consider factors beyond credit scores, such as employment stability and community ties.

Submitting Your Application

Most lenders now accept online applications, though some borrowers prefer in-person meetings for major financial decisions. The application asks for personal information, employment details, and specifics about the debts you wish to consolidate.

Processing times vary by lender. Some provide instant pre-approval decisions, while final approval and funding may take anywhere from one day to two weeks. During this period, continue making minimum payments on your existing debts to avoid late fees or credit damage.

Managing Your Consolidation Loan Successfully

Obtaining a debt consolidation loan represents just the beginning of your financial recovery journey. How you manage the loan determines whether it truly improves your situation.

Creating a Realistic Budget

With your new single payment established, build a comprehensive budget that accounts for all monthly expenses. This helps ensure you never miss a payment and identifies opportunities to pay extra toward your loan principal.

Your budget should include:

- Fixed expenses: Rent/mortgage, utilities, insurance, loan payment

- Variable expenses: Groceries, transportation, healthcare

- Discretionary spending: Entertainment, dining out, hobbies

- Emergency savings: At least $500-$1,000 for unexpected costs

- Extra loan payments: Any surplus directed toward debt reduction

Automating your loan payment eliminates the risk of forgetting due dates. Most lenders offer automatic withdrawal from your checking account, and some provide small interest rate discounts for enrolling in autopay.

Avoiding New Debt Accumulation

The biggest mistake borrowers make after consolidation involves accumulating new debt. Once you pay off credit cards through your consolidation loan, those accounts show zero balances. The temptation to use them again can be strong, especially during emergencies or when attractive purchases arise.

Discipline becomes essential. Consider these strategies:

- Close accounts you don't need, keeping one or two for emergencies only

- Remove saved payment information from online shopping sites

- Use cash or debit cards instead of credit

- Implement a 48-hour waiting period before non-essential purchases

- Build an emergency fund to handle unexpected expenses

Monitoring Your Progress

Track your declining balance monthly to stay motivated. Watching your debt decrease reinforces positive financial behaviors and provides tangible evidence of your progress. Many borrowers find that visualizing their journey toward being debt-free strengthens their commitment to the plan.

Consider celebrating milestones along the way. When you reach 25%, 50%, and 75% paid off, acknowledge your achievement. These celebrations don't need to involve spending money; they simply recognize your discipline and progress.

Understanding Potential Drawbacks and Risks

While debt consolidation loans offer significant advantages, they're not without potential downsides. Understanding these risks helps you make informed decisions and avoid common pitfalls.

Extended Repayment Periods

Lower monthly payments often come from stretching your repayment over a longer period. While this improves your monthly cash flow, you'll ultimately pay more in total interest. A $20,000 consolidation loan at 10% APR illustrates this point:

| Loan Term | Monthly Payment | Total Interest Paid | Total Repayment |

|---|---|---|---|

| 3 years | $645 | $3,220 | $23,220 |

| 5 years | $425 | $5,500 | $25,500 |

| 7 years | $330 | $7,720 | $27,720 |

The seven-year term costs $4,500 more in interest than the three-year option, despite having a monthly payment $315 lower.

Fees and Additional Costs

Some lenders charge origination fees, which reduce the amount you actually receive. If you borrow $15,000 with a 5% origination fee, you receive $14,250 but owe $15,000 plus interest. Understanding what federal law requires lenders to disclose protects you from unexpected costs.

Late payment fees, returned payment charges, and prepayment penalties can also increase your costs. Read all loan documents carefully before signing, and ask questions about any terms you don't understand.

Special Considerations for Different Credit Situations

Your credit history significantly influences the debt consolidation loans available to you. Different credit tiers require different strategies.

Options for Borrowers with Good to Excellent Credit

If your credit score exceeds 670, you'll qualify for the most competitive rates and terms. Banks, credit unions, and online lenders actively compete for your business, giving you negotiating leverage.

Shopping around becomes especially important in this tier. Even a 1-2% difference in interest rate translates to hundreds or thousands of dollars over the loan's life. Don't hesitate to use offers from one lender to negotiate with another.

Solutions for Past Credit Challenges

Borrowers who have experienced credit difficulties still have options for debt consolidation loans. Lenders specializing in working with various credit situations consider factors beyond just credit scores, including current income, employment stability, and debt-to-income ratios.

These loans may carry higher interest rates than prime offerings, but they still often beat credit card rates. More importantly, they provide an opportunity to improve your credit score through consistent on-time payments. After 12-18 months of responsible loan management, many borrowers qualify to refinance at better rates.

Co-signers can help borrowers with challenged credit access better terms. A co-signer with strong credit essentially guarantees your loan, reducing the lender's risk. However, remember that missed payments affect both your credit and your co-signer's credit, making this a serious responsibility.

Industry Standards and Best Practices

Working with legitimate debt consolidation programs requires knowing what separates reputable lenders from predatory ones. Industry best practices protect consumers and ensure fair treatment.

Red Flags to Avoid

Certain warning signs indicate you should walk away from a lender:

- Guaranteed approval regardless of credit history

- Requests for upfront fees before loan approval

- Pressure to decide immediately without time to review terms

- Unwillingness to provide written documentation

- Rates and terms that seem too good to be true

Legitimate lenders always provide clear, written disclosures about rates, fees, terms, and your rights as a borrower. They encourage you to read everything carefully and ask questions before committing.

Working with Regulated Lenders

Choose lenders licensed to operate in your state. Louisiana, Mississippi, Tennessee, and Georgia each regulate consumer lending, requiring specific licenses and compliance with state laws. Licensed lenders submit to oversight and follow established consumer protection guidelines.

Local lenders with physical branches often provide advantages over purely online operations. Face-to-face relationships, community investment, and personalized service create accountability that benefits borrowers. When questions or issues arise, walking into a branch office often resolves problems faster than navigating online customer service systems.

Alternatives to Traditional Consolidation Loans

Debt consolidation loans work well for many people, but they're not the only solution for managing multiple debts. Understanding alternatives helps you choose the best approach for your specific situation.

Debt Management Plans

Credit counseling agencies offer debt management plans that negotiate with your creditors to reduce interest rates and create a consolidated payment plan. You make one monthly payment to the agency, which distributes funds to your creditors. These plans don't involve taking out new loans, making them suitable for borrowers who don't qualify for favorable consolidation loan terms.

The trade-off involves closing your credit accounts and potential impacts on your credit report. However, for severely over-extended borrowers, this structured approach provides essential discipline and professional guidance.

Debt Settlement Programs

Debt settlement involves negotiating with creditors to accept less than the full balance owed. While this can significantly reduce your total debt, it severely damages your credit score and may have tax implications, as forgiven debt often counts as taxable income.

This option should be considered only when you cannot afford minimum payments and want to avoid bankruptcy. The credit damage takes years to repair, and understanding various consolidation approaches helps you make informed comparisons.

DIY Debt Payoff Strategies

Some borrowers successfully eliminate debt without consolidation through disciplined payoff strategies:

- Debt avalanche method: Pay minimums on all debts while directing extra money toward the highest-interest balance

- Debt snowball method: Pay minimums on all debts while directing extra money toward the smallest balance for psychological wins

- Debt snowflake method: Apply every small windfall (tax refunds, bonuses, side gig income) immediately to debt

These approaches require significant discipline but avoid taking on new debt and paying loan fees.

Debt consolidation loans provide a powerful tool for simplifying your finances and potentially reducing the total cost of your debt when used strategically. Whether you're dealing with medical bills, credit card balances, or other personal loans, consolidating into a single payment can reduce stress and accelerate your path to financial freedom. If you're ready to explore your consolidation options across Louisiana, Mississippi, Tennessee, or Georgia, Standard Financial offers flexible financing solutions tailored to your unique situation, including options for borrowers with past credit challenges. Contact us today to discuss how we can help you take control of your financial future.

No comment yet, add your voice below!