When unexpected expenses arise or you're planning a major purchase, choosing between different financing options can feel overwhelming. Two of the most accessible forms of consumer credit are personal loans and credit cards, each offering distinct advantages depending on your financial situation and goals. Understanding the fundamental differences between these borrowing options will help you make informed decisions that align with your budget, credit profile, and long-term financial health. Whether you're consolidating debt, funding a home improvement project, or covering medical expenses, knowing when to use each type of credit can save you thousands of dollars in interest and fees.

Understanding the Core Differences

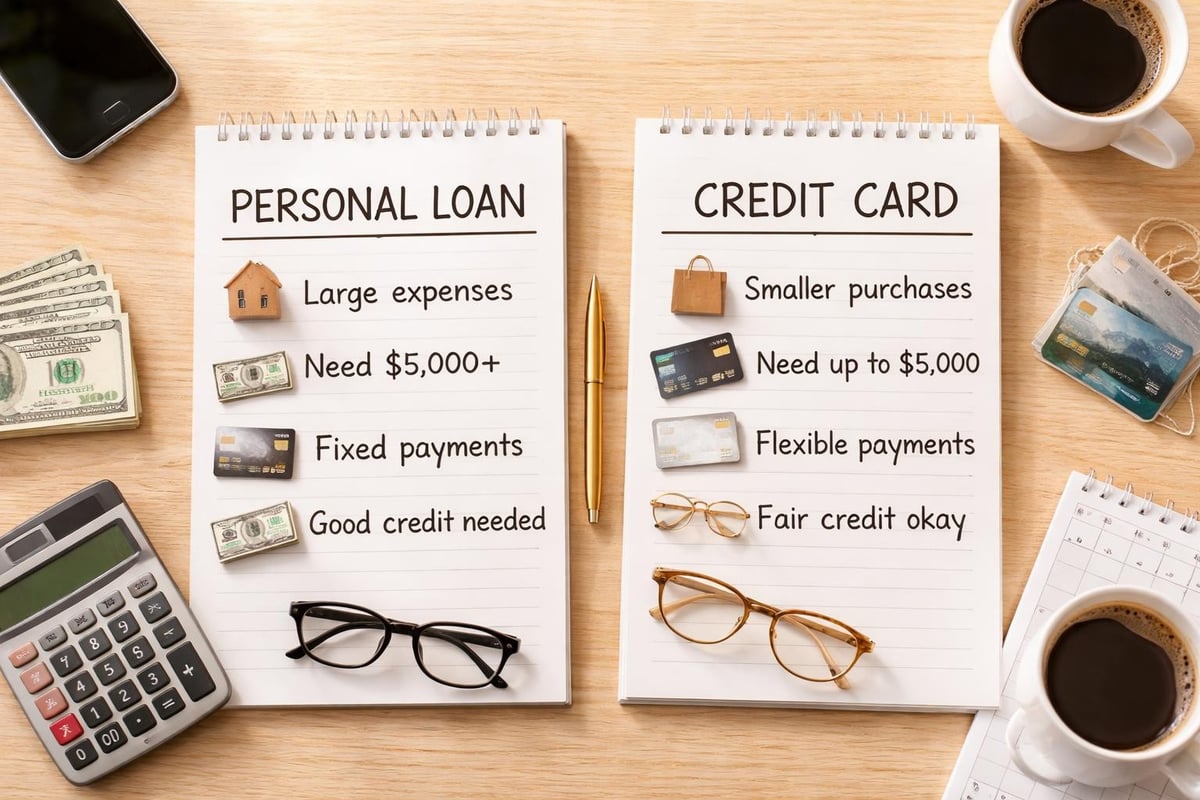

Personal loans and credit cards operate on fundamentally different principles, and recognizing these distinctions is essential for smart financial planning. A personal loan provides a lump sum of money upfront with a fixed repayment schedule, typically ranging from two to seven years. You receive the entire amount at once and make consistent monthly payments until the debt is fully repaid.

Credit cards, conversely, offer revolving credit that you can use repeatedly up to your credit limit. As you pay down your balance, that credit becomes available again for future purchases. This flexibility makes credit cards ideal for ongoing expenses, while personal loans work better for one-time costs with predictable repayment needs.

Interest Rate Structures

The way interest accrues represents one of the most significant differences in the personal loans vs credit cards debate. Personal loans typically feature fixed interest rates, meaning your rate stays constant throughout the loan term. This predictability allows for easier budgeting since your monthly payment never changes.

Credit card interest rates are usually variable, tied to the prime rate, and can fluctuate based on market conditions. Additionally, credit card APRs often range from 16% to 29%, significantly higher than many personal loan rates. For borrowers with good credit, personal loans may offer rates as low as 6% to 10%, though rates vary based on creditworthiness and lender requirements.

Key rate considerations:

- Personal loans lock in your rate at origination

- Credit cards can increase rates with market changes

- Promotional 0% APR credit card offers are temporary

- Missing payments can trigger penalty APRs on credit cards

Repayment Terms and Monthly Obligations

When evaluating personal loans vs credit cards, repayment flexibility plays a crucial role in determining which option suits your needs. Personal loans require fixed monthly payments that include both principal and interest, calculated to pay off the entire balance by the end of the loan term. This structured approach eliminates guesswork and ensures you're making consistent progress toward becoming debt-free.

Credit cards only require minimum monthly payments, typically 1% to 3% of your balance plus interest and fees. While this lower minimum provides short-term flexibility, paying only the minimum can extend repayment for years or even decades, resulting in substantially higher total interest costs.

| Feature | Personal Loans | Credit Cards |

|---|---|---|

| Payment Amount | Fixed monthly payment | Minimum payment (variable) |

| Payment Flexibility | Structured, predictable | Pay minimum or more |

| Repayment Timeline | 2-7 years typically | Indefinite if paying minimums |

| Total Interest | Lower with fixed term | Potentially much higher |

| Budget Planning | Easy to plan | Requires discipline |

Payment Example Scenario

Consider borrowing $10,000 to consolidate debt. With a personal loan at 9% APR over five years, you'd pay approximately $208 per month with total interest of about $2,480. Using a credit card at 20% APR and paying only the minimum, you could take over 20 years to pay off the same amount, with interest exceeding $15,000.

This dramatic difference illustrates why understanding the personal loans vs credit cards comparison matters for your financial wellbeing. The structured repayment of personal loans forces consistent progress, while credit card flexibility can become a trap without disciplined repayment habits.

Credit Score Impact and Utilization

Both personal loans and credit cards affect your credit score, but in different ways. Credit utilization, the ratio of your credit card balances to your credit limits, accounts for approximately 30% of your FICO score. High credit card balances relative to your limits can significantly damage your credit, even if you make all payments on time.

Personal loans don't factor into credit utilization calculations the same way. While they appear on your credit report as installment debt, they don't carry the same utilization penalty. In fact, adding a personal loan to your credit mix while paying down credit card balances can actually improve your credit score by diversifying your credit types and lowering your overall utilization ratio.

Credit impact factors:

- Opening either account triggers a hard inquiry (temporary score dip)

- Payment history matters equally for both (35% of your score)

- Personal loans improve credit mix diversity

- Paying off credit cards with a personal loan reduces utilization

- Credit age affects scores (keeping old cards open helps)

Strategic Credit Building

For borrowers rebuilding credit after past challenges, the personal loans vs credit cards decision becomes even more important. Personal loans provide a structured path to demonstrate responsible payment behavior, with progress clearly visible on your credit report each month. Standard Financial specializes in working with clients who have experienced credit difficulties, offering personal loans that help rebuild financial standing while addressing immediate needs.

Credit cards offer faster access to revolving credit but require more self-discipline to avoid accumulating balances that strain your budget. Some consumers benefit from using both strategically: personal loans for major expenses and credit cards for small, regularly paid-off purchases that build positive payment history.

Best Use Cases for Each Option

Determining when to use personal loans versus credit cards depends largely on the nature of your expense and your financial situation. Personal loans excel for large, one-time expenses with defined costs. Home improvement projects, medical procedures, debt consolidation, and major purchases like furniture or appliances are ideal candidates for personal loan financing.

The fixed repayment schedule ensures these significant costs don't linger indefinitely on your balance sheet. When you're financing a $15,000 bathroom renovation or $8,000 in medical expenses, knowing exactly when you'll be debt-free provides peace of mind and financial clarity.

Personal Loan Advantages

- Predictable budgeting: Fixed payments make monthly planning straightforward

- Lower interest rates: Especially for borrowers with good to fair credit

- Debt consolidation: Combine multiple high-interest debts into one payment

- Large lump sums: Access significant funding for major expenses

- Credit improvement: Structured repayment builds positive history

Credit Card Advantages

- Ongoing flexibility: Reusable credit for recurring needs

- Rewards programs: Earn cash back, points, or travel miles

- Short-term borrowing: 0% intro APR offers for qualified applicants

- Purchase protections: Extended warranties and fraud protection

- Emergency access: Immediate availability for unexpected costs

Fees and Additional Costs

Beyond interest rates, various fees affect the true cost of borrowing when comparing personal loans vs credit cards. Personal loans may include origination fees (typically 1% to 8% of the loan amount), late payment fees, and prepayment penalties, though many lenders have eliminated prepayment penalties in recent years. These costs are usually disclosed upfront, allowing you to calculate the total borrowing cost before committing.

Credit cards carry their own fee structure, including annual fees (ranging from $0 to $500+ for premium cards), balance transfer fees (typically 3% to 5%), cash advance fees, foreign transaction fees, and late payment penalties. While many cards waive annual fees, the cumulative cost of other fees can add up quickly, especially if you carry balances or use cash advances.

| Fee Type | Personal Loans | Credit Cards |

|---|---|---|

| Origination/Annual | 0-8% (one-time) | $0-$500 (yearly) |

| Late Payment | $25-$40 | $30-$40 |

| Balance Transfer | Not applicable | 3-5% of amount |

| Cash Advance | Not applicable | 3-5% plus higher APR |

| Prepayment Penalty | Varies by lender | None |

Calculating True Borrowing Costs

When evaluating the personal loans vs credit cards decision, calculate the Annual Percentage Rate (APR), which includes interest and certain fees, for a more accurate cost comparison. A personal loan with a 3% origination fee and 8% interest rate may have an effective APR closer to 10% when amortized over the loan term. Similarly, a credit card with a $95 annual fee effectively increases your APR if you maintain lower balances.

For residents in Louisiana, Mississippi, Tennessee, and Georgia seeking transparent lending terms, working with established lenders who clearly disclose all fees eliminates surprises and enables better financial planning.

Application and Approval Process

The application experience differs considerably between personal loans and credit cards. Personal loan applications typically require more documentation, including proof of income, employment verification, and detailed financial information. Lenders review your debt-to-income ratio, credit history, and ability to repay before approval. The process may take several days, though some lenders offer same-day decisions and funding.

Credit card applications are generally faster and less documentation-intensive. Many issuers provide instant decisions based primarily on your credit score and reported income. You might receive your card within a week of approval, or even immediately with instant card numbers for certain issuers.

Application requirements comparison:

- Personal Loans: Government-issued ID, proof of income, bank statements, employment verification, credit check

- Credit Cards: Government-issued ID, income information, Social Security number, credit check

Approval Considerations for Different Credit Profiles

Understanding how lenders evaluate applications helps you choose the right option. Personal loan lenders consider your complete financial picture, which can work to your advantage if you have steady income despite past credit challenges. Some lenders, including those specializing in consumer lending, offer programs specifically designed for borrowers rebuilding credit.

Credit card issuers rely heavily on credit scores for approval and limit determination. Borrowers with lower credit scores may only qualify for secured credit cards requiring deposits or cards with higher interest rates and lower limits. The personal loans vs credit cards decision sometimes comes down to which option you can actually access based on your current credit situation.

Borrowing Limits and Access to Funds

Personal loans typically range from $1,000 to $50,000, though amounts vary by lender and borrower qualifications. Once approved, you receive the entire amount as a lump sum, usually via direct deposit to your bank account. This makes personal loans ideal when you need substantial funding immediately for a specific purpose.

Credit card limits depend on your creditworthiness and can range from a few hundred dollars to $50,000 or more for premium cards and excellent credit. You can access funds immediately up to your available credit, making cards more suitable for ongoing or unpredictable expenses. However, using your entire credit limit damages your credit utilization ratio and can trigger over-limit fees.

Strategic Funding Approaches

For major expenses like home improvements or medical procedures, personal loans provide the full amount needed without the temptation to underfund the project or spread payments across multiple high-interest cards. A $20,000 kitchen renovation financed with a personal loan at 9% over five years costs far less than charging it across credit cards at higher rates.

Conversely, for ongoing business expenses, monthly bills, or situations where you need flexible access to funds over time, credit cards offer advantages. The key is matching the financial product to your specific need rather than defaulting to whichever seems more convenient.

Long-Term Financial Planning Implications

Your choice in the personal loans vs credit cards debate affects your financial trajectory beyond the immediate transaction. Personal loans create forced savings discipline through fixed payments, helping you build equity and improve financial habits. The defined end date provides psychological benefits, with clear progress toward a debt-free future.

Credit cards can support or sabotage long-term financial health depending on usage patterns. Used responsibly with full monthly payments, they build credit, earn rewards, and provide convenient payment methods. However, revolving high-interest debt month after month creates a financial burden that compounds over time, making it harder to save, invest, or pursue other financial goals.

Building a Balanced Credit Strategy

Many financially successful individuals use both personal loans and credit cards strategically. They finance major one-time expenses with personal loans for predictable repayment and lower interest costs, while using credit cards for everyday purchases paid in full monthly to earn rewards and maintain credit activity.

This balanced approach requires discipline but maximizes the benefits of each option while minimizing costs. If you're consolidating existing credit card debt, a personal loan can provide the structure needed to escape the revolving debt cycle, while keeping one credit card for emergencies and building positive payment history.

Special Considerations for Different Life Situations

Life circumstances significantly influence which option serves you best. Families facing medical expenses often benefit from personal loans that convert unpredictable healthcare costs into manageable monthly payments. The fixed repayment term ensures medical debt doesn't linger for years, allowing families to move forward financially.

Students and parents financing education expenses might use both options strategically: personal loans for tuition and major fees, with credit cards for books, supplies, and living expenses that vary semester to semester. Home improvement projects almost always favor personal loans, as renovation costs are substantial, defined, and benefit from lower interest rates over multi-year repayment periods.

Situation-specific recommendations:

- Medical expenses: Personal loans for large bills, payment plans for smaller amounts

- Home improvements: Personal loans for projects over $5,000

- Debt consolidation: Personal loans to combine multiple high-interest debts

- Emergency expenses: Credit cards for immediate access, then consider consolidation

- Everyday purchases: Credit cards paid in full monthly

Geographic Considerations

For residents in states like Louisiana, Mississippi, Tennessee, and Georgia, where Standard Financial maintains branch offices, local lending relationships offer advantages. Working with a lender who understands regional economic conditions and maintains physical locations provides accessibility that purely online lenders cannot match, especially for borrowers who value in-person service or need assistance navigating the application process.

Regional lenders also better understand local cost of living, employment markets, and economic factors that influence lending decisions, potentially offering more favorable terms for qualified borrowers in their service areas.

Making Your Decision

Choosing between personal loans and credit cards requires honest assessment of your financial situation, spending habits, and specific needs. Ask yourself these critical questions: Do you need a specific lump sum or ongoing access to credit? Can you commit to fixed monthly payments, or do you need flexibility? What interest rate do you qualify for with each option? How will this decision affect your credit score and long-term financial health?

For most large, one-time expenses, personal loans offer superior value through lower rates, structured repayment, and predictable budgeting. Credit cards serve better for smaller, ongoing purchases, emergency access, and situations where you can pay balances quickly to avoid interest charges.

The personal loans vs credit cards decision ultimately depends on your unique financial circumstances and goals. Personal loans provide structure, lower rates, and predictable payments for major expenses, while credit cards offer flexibility for ongoing needs. If you're considering a personal loan for home improvements, medical expenses, education costs, or debt consolidation, Standard Financial offers flexible financing options with branch offices throughout Louisiana, Mississippi, Tennessee, and Georgia. Their experienced team works with clients across various credit situations to find financing solutions that fit your budget and help you achieve your financial objectives.

No comment yet, add your voice below!