Securing financing when your monthly debt obligations consume a significant portion of your income presents unique challenges. Many borrowers across Louisiana, Mississippi, Tennessee, and Georgia face this situation, wondering whether they can still qualify for the funding they need. Understanding how lenders evaluate your debt-to-income ratio and what options exist for those with higher percentages can make the difference between approval and rejection. The good news is that personal loans with high debt to income ratio requirements are available from specialized lenders who look beyond traditional metrics to assess your overall financial picture.

Understanding Debt-to-Income Ratio Fundamentals

Your debt-to-income (DTI) ratio represents the percentage of your gross monthly income dedicated to debt payments. Calculating your debt-to-income ratio involves dividing your total monthly debt obligations by your gross monthly income, then multiplying by 100.

Lenders use this metric to gauge your ability to manage monthly payments and repay borrowed funds. A lower ratio indicates you have more income available after covering existing debts, which reduces the lender's risk.

What Qualifies as a High DTI Ratio

Most traditional lenders prefer borrowers with DTI ratios below 36%. When your ratio exceeds this threshold, you enter high DTI territory. Ratios between 37% and 43% are considered elevated, while anything above 43% signals significant financial strain to conventional lenders.

Different loan types have varying DTI thresholds:

- Conventional personal loans: Typically require DTI under 36%

- Specialized personal loans: May accept DTI up to 50%

- Secured loan products: Often more flexible with DTI requirements

- Home improvement financing: Sometimes accommodates higher ratios

The specific threshold that defines "high" also depends on your overall credit profile, employment stability, and the lender's risk tolerance.

Why Traditional Lenders Scrutinize High DTI Ratios

Financial institutions view high debt-to-income ratios as red flags because they suggest limited financial flexibility. When a large percentage of your income already goes toward debt service, unexpected expenses or income disruptions could trigger payment defaults.

Risk Assessment Factors

Lenders evaluate several risk elements when reviewing applications with elevated DTI ratios. They consider whether you have emergency savings, the stability of your employment, and your payment history on existing obligations.

Your credit score plays a crucial role in this assessment. Borrowers with excellent credit (720+) and high DTI ratios often receive more favorable consideration than those with both poor credit and high debt burdens.

| DTI Range | Credit Score 720+ | Credit Score 640-719 | Credit Score Below 640 |

|---|---|---|---|

| Under 36% | Excellent approval odds | Very good approval odds | Moderate approval odds |

| 37-43% | Good approval odds | Moderate approval odds | Challenging approval |

| 44-50% | Moderate approval odds | Challenging approval | Requires specialized lenders |

| Above 50% | Challenging approval | Requires specialized lenders | Very limited options |

The combination of high DTI and other risk factors creates compound concerns for lenders evaluating personal loans with high debt to income ratio requirements.

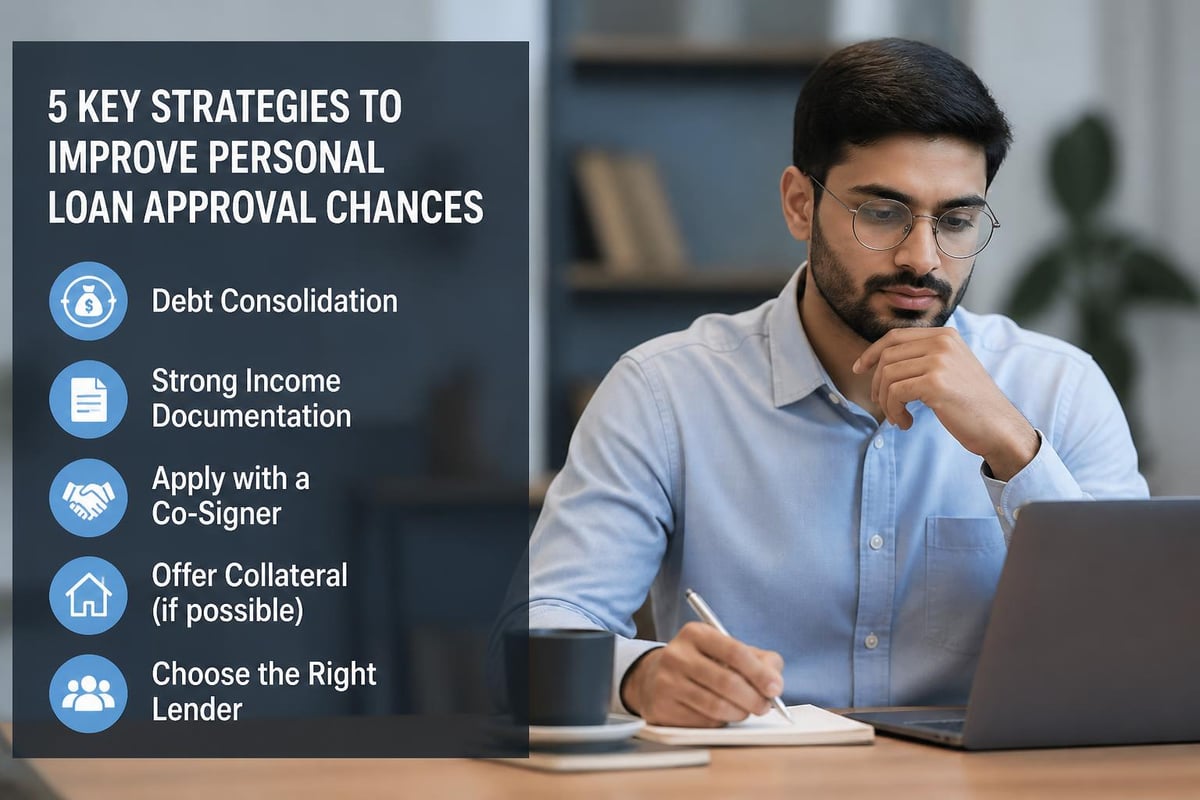

Strategies to Improve Your Loan Approval Chances

Several approaches can strengthen your application when seeking personal loans with high debt to income ratio circumstances. These tactics either reduce your DTI or compensate for it through other financial strengths.

Debt Consolidation Before Applying

Combining multiple high-interest debts into a single loan can reduce your monthly payment obligations. This strategy works particularly well when you consolidate credit card balances or payday loans into a personal loan with lower interest rates and extended terms.

The monthly payment reduction directly improves your DTI calculation. However, ensure the consolidation loan's terms genuinely benefit your financial situation rather than simply extending your debt timeline.

Increasing Your Income Documentation

Improving your chances of loan approval often involves demonstrating additional income sources. Many borrowers overlook legitimate income that could strengthen their applications.

Consider documenting these income sources:

- Freelance or consulting work

- Rental property income

- Investment dividends and interest

- Regular bonuses or commissions

- Child support or alimony payments

- Part-time employment earnings

Providing tax returns, bank statements, and employment verification for all income sources creates a more complete financial picture for lenders evaluating your application.

Adding a Co-Signer or Co-Borrower

Including someone with stronger financial metrics can offset your high DTI ratio. A co-signer with excellent credit and low debt obligations reduces the lender's overall risk exposure.

The co-signer becomes equally responsible for repayment, which provides the lender additional recourse if payments become delinquent. This arrangement works best when you have a trusted family member or partner willing to support your application.

Types of Personal Loans Available with High DTI

Not all personal loan products maintain identical DTI requirements. Understanding which loan types accommodate higher ratios helps you target appropriate lenders and products.

Secured Personal Loans

Offering collateral dramatically improves approval odds for borrowers with high debt-to-income ratios. When you pledge assets like vehicles, savings accounts, or investment portfolios, lenders gain security that reduces their risk exposure.

Secured loans typically offer:

- Lower interest rates compared to unsecured products

- Higher borrowing limits due to collateral protection

- More flexible DTI requirements (often accepting 50%+ ratios)

- Longer repayment terms that reduce monthly payment burdens

The primary drawback involves the risk of losing your collateral if you default on payments. Only choose secured loans when you have confidence in your repayment ability.

Medical and Home Improvement Loans

Specialized personal loans for specific purposes sometimes accommodate higher DTI ratios because they address necessary expenses. Medical financing and home improvement loans fall into this category, particularly when the expenditure adds value or addresses urgent needs.

These purpose-specific loans may have more lenient requirements because:

- Home improvements increase property value

- Medical procedures address health necessities

- Education loans build future earning potential

- Debt consolidation loans actually reduce DTI over time

Lenders recognize that these expenditures serve legitimate purposes rather than discretionary spending.

Alternative and Online Lenders

Non-traditional lenders often use different underwriting criteria than banks and credit unions. Many online platforms and specialized lenders consider factors beyond DTI ratios when evaluating applications.

| Lender Type | Typical Max DTI | Primary Advantages | Potential Drawbacks |

|---|---|---|---|

| Traditional Banks | 36-40% | Lowest rates, established relationships | Strict requirements |

| Credit Unions | 40-45% | Member-focused, competitive rates | Membership required |

| Online Lenders | 45-50% | Fast approval, flexible criteria | Higher interest rates |

| Specialized Consumer Lenders | 50%+ | Accept past credit issues, flexible terms | Premium pricing |

These alternative sources provide viable options for personal loans with high debt to income ratio situations when conventional lenders decline applications.

Documentation Requirements for High DTI Applications

Thorough documentation becomes even more critical when your debt-to-income ratio exceeds standard thresholds. Lenders need comprehensive financial information to offset concerns about your debt burden.

Essential Financial Documents

Prepare these materials before submitting applications:

- Pay stubs covering the most recent 30-60 days

- Tax returns for the previous two years

- Bank statements showing three to six months of transaction history

- Proof of additional income from all sources

- Current debt statements listing balances and minimum payments

- Employment verification letters or direct employer contacts

Complete documentation accelerates the approval process and demonstrates financial responsibility to lenders.

Explanation Letters

A well-crafted explanation letter helps lenders understand the context behind your high DTI ratio. Address temporary circumstances, upcoming debt payoffs, or recent income increases that standard calculations don't capture.

Your letter should explain:

- The specific reasons for your current debt burden

- Steps you're taking to improve your financial situation

- Any mitigating factors that offset the high ratio

- Your reliable payment history despite the elevated DTI

This personal context can influence underwriter decisions, particularly at lenders who review applications individually rather than relying solely on automated systems.

Impact of DTI on Loan Terms and Pricing

Understanding what constitutes a good debt-to-income ratio helps you anticipate how lenders will price your loan. Higher ratios typically result in less favorable terms, even when you receive approval.

Interest Rate Adjustments

Lenders charge premium interest rates on personal loans with high debt to income ratio approvals. This risk-based pricing compensates for the increased likelihood of default.

Expect rate increases of:

- 1-2 percentage points for DTI between 37-43%

- 2-4 percentage points for DTI between 44-50%

- 4-6 percentage points for DTI above 50%

These adjustments apply on top of the baseline rate determined by your credit score and loan amount. The combined effect can significantly increase your total interest costs.

Loan Amount Limitations

Even when approved, borrowers with high DTI ratios typically receive lower maximum loan amounts. Lenders limit exposure by capping the additional debt they'll extend to already burdened borrowers.

A borrower with 30% DTI might qualify for $35,000, while someone with 45% DTI seeking the same loan might only receive approval for $15,000 to $20,000. This protection prevents borrowers from taking on unmanageable debt levels.

Regional Considerations for Southern States

Borrowers in Louisiana, Mississippi, Tennessee, and Georgia face unique economic factors that influence DTI calculations and loan availability. Understanding regional employment patterns and cost-of-living variations helps contextualize your financial situation.

Economic Factors by State

Each state presents different economic realities that affect debt-to-income ratios:

Louisiana residents often work in energy, petrochemical, and tourism industries with variable income patterns. Seasonal employment and commission-based work require careful income documentation for lenders.

Mississippi borrowers frequently face lower median incomes but also benefit from lower housing costs. This combination can create moderate DTI ratios despite modest earnings.

Tennessee features diverse metropolitan and rural economies. Nashville and Memphis residents typically earn higher incomes but face elevated housing costs, while rural areas show inverse patterns.

Georgia borrowers, particularly in Atlanta's metro area, often contend with rising housing costs that increase debt burdens. However, the state's strong job market provides income growth opportunities.

State Lending Regulations

Understanding your state's consumer protection laws helps you identify fair lending practices. Each state maintains different regulations governing interest rate caps, fee limitations, and disclosure requirements.

These protections ensure that personal loans with high debt to income ratio options remain accessible without predatory terms. Reputable lenders comply with all state regulations while providing flexible solutions for challenging financial situations.

Long-Term Financial Planning with High DTI

Securing a loan represents only the first step. Developing a sustainable plan to reduce your debt-to-income ratio protects your long-term financial health and improves future borrowing opportunities.

Creating a Debt Reduction Timeline

Establish specific milestones for lowering your DTI ratio over 12, 24, and 36-month periods. This structured approach keeps you accountable and motivated as you work toward financial improvement.

Set realistic targets such as:

- Reducing DTI by 5% within six months

- Paying off one complete debt obligation within one year

- Achieving DTI below 43% within 18 months

- Reaching DTI under 36% within three years

Track your progress monthly and adjust strategies as your income or expenses change.

Building Emergency Reserves

High debt-to-income ratios leave little margin for unexpected expenses. Simultaneously building emergency savings while managing debt creates financial resilience that prevents future borrowing needs.

Start with small automatic transfers to savings, even $25 or $50 monthly. These modest contributions accumulate over time and provide a buffer against car repairs, medical bills, or temporary income disruptions that might otherwise require additional borrowing.

Common Mistakes to Avoid

Borrowers seeking personal loans with high debt to income ratio approvals often make errors that reduce their chances or result in unfavorable terms. Awareness of these pitfalls helps you navigate the process more successfully.

Applying to Too Many Lenders Simultaneously

Multiple hard credit inquiries within a short period can lower your credit score and signal desperation to lenders. While rate shopping for mortgages or auto loans groups inquiries together, personal loan applications often count individually.

Limit applications to three or four carefully selected lenders. Research requirements beforehand to target those most likely to approve your specific financial profile.

Failing to Address Underlying Issues

Taking another loan without addressing the behaviors that created high debt burdens simply compounds problems. Honest assessment of spending patterns, income stability, and financial habits determines whether additional borrowing provides genuine solutions or temporary relief.

Consider whether you need:

- Professional credit counseling to develop sustainable budgets

- Income enhancement through additional work or career advancement

- Expense reduction by eliminating discretionary spending

- Debt settlement for unmanageable obligations

These fundamental changes create lasting improvement rather than cyclical borrowing patterns.

Overlooking Total Cost Analysis

Focusing solely on monthly payment amounts obscures the true cost of loans. Personal loans with high debt to income ratio approvals often carry extended terms that reduce payments but dramatically increase total interest paid.

Compare these scenarios for a $10,000 loan at 12% APR:

| Loan Term | Monthly Payment | Total Interest Paid | Total Repayment |

|---|---|---|---|

| 24 months | $471 | $1,304 | $11,304 |

| 36 months | $332 | $1,952 | $11,952 |

| 48 months | $263 | $2,624 | $12,624 |

| 60 months | $222 | $3,320 | $13,320 |

While 60-month terms create the lowest monthly obligation, they cost $2,016 more in interest than 24-month repayment. Balance affordability against total cost when selecting loan terms.

Working with Specialized Consumer Lenders

Consumer lending specialists who serve borrowers with past credit issues or challenging financial circumstances offer distinct advantages for those seeking personal loans with high debt to income ratio solutions.

Relationship-Based Lending

Branch-based lenders in Louisiana, Mississippi, Tennessee, and Georgia often employ relationship lending approaches. These institutions consider your complete financial story rather than relying exclusively on automated underwriting systems.

Meeting face-to-face with loan officers allows you to:

- Explain unique circumstances affecting your DTI ratio

- Demonstrate employment stability and community ties

- Provide context that standard applications cannot capture

- Build ongoing relationships for future financial needs

This personalized approach frequently results in approvals when online algorithms would automatically decline applications.

Flexible Underwriting Standards

Specialized lenders design products specifically for borrowers who don't fit traditional lending boxes. Their underwriting criteria emphasize payment history, employment stability, and reasonable collateral over rigid DTI thresholds.

These lenders recognize that debt-to-income ratios represent one data point among many factors determining creditworthiness. A borrower with 48% DTI but five years of perfect payment history might pose less risk than someone with 35% DTI and recent delinquencies.

Successfully securing financing despite elevated debt obligations requires understanding lender perspectives, preparing thorough documentation, and targeting appropriate loan products. Whether you need funds for medical expenses, home improvements, or education, options exist even when your debt-to-income ratio exceeds conventional thresholds. Standard Financial specializes in flexible financing solutions for borrowers across Louisiana, Mississippi, Tennessee, and Georgia, including those with past credit challenges or high debt-to-income ratios. Visit one of our branch offices to discuss personalized loan options that address your unique financial situation and goals.

No comment yet, add your voice below!