Financial emergencies can strike without warning, leaving individuals and families scrambling to cover unexpected expenses. Whether it's a medical bill, urgent home repair, or sudden job loss, having access to quick funding can make the difference between managing a crisis and falling into deeper financial trouble. Emergency loans provide a lifeline for those facing urgent financial needs, offering faster approval processes and more flexible terms than traditional lending options. Understanding how these loans work, who qualifies, and what to consider before applying empowers borrowers to make informed decisions during stressful times.

Understanding Emergency Loans and How They Work

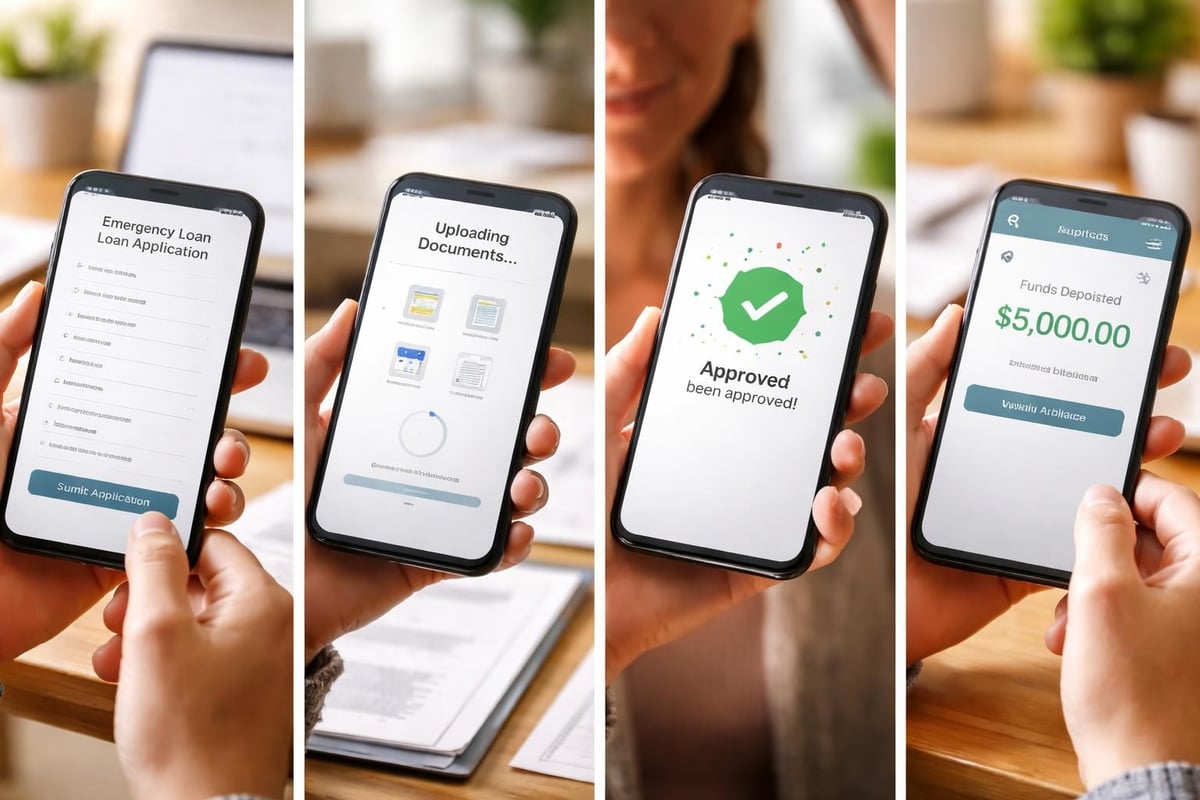

Emergency loans are financial products designed specifically to address urgent, unexpected expenses that cannot wait for traditional loan approval timelines. These loans prioritize speed and accessibility, often providing funds within 24 to 48 hours of approval.

Unlike conventional personal loans that may take weeks to process, emergency loans streamline the application and underwriting process. Lenders typically evaluate basic criteria such as income verification, employment status, and credit history, but many are willing to work with borrowers who have less-than-perfect credit scores.

Key characteristics of emergency loans include:

- Expedited application and approval processes

- Smaller loan amounts typically ranging from $500 to $10,000

- Shorter repayment terms, usually 12 to 60 months

- Higher interest rates compared to secured loans

- Minimal documentation requirements

- Funding disbursed within one to three business days

The flexibility of emergency loans makes them particularly valuable for residents across Louisiana, Mississippi, Tennessee, and Georgia who face regional challenges like hurricane damage, medical emergencies, or unexpected vehicle repairs needed for work commutes.

Common Reasons People Seek Emergency Loans

Financial emergencies take many forms, and understanding the most common scenarios helps borrowers recognize when this type of financing might be appropriate. Medical expenses top the list, with unexpected hospital visits, urgent procedures, or prescription costs creating immediate financial pressure.

Home repairs represent another major category. When a water heater fails, a roof leaks, or an HVAC system stops working in the middle of summer, homeowners need quick access to funds to prevent further damage and maintain safe living conditions.

Other frequent emergency loan uses include:

- Vehicle repairs necessary for work transportation

- Funeral and burial expenses

- Emergency travel for family situations

- Utility bills to prevent service disconnection

- Rent or mortgage payments during temporary job loss

- Legal fees for urgent matters

- Emergency veterinary care for pets

Natural disasters particularly impact communities in the Southeast, where hurricanes, floods, and severe storms can create widespread emergency funding needs. While federal emergency farm loans help agricultural producers recover from disasters, consumer emergency loans serve similar purposes for individuals and families.

Eligibility Requirements and Application Process

Qualifying for emergency loans involves meeting certain baseline criteria, though requirements vary significantly among lenders. Most financial institutions evaluate applicants based on their ability to repay the loan rather than solely on credit scores.

Standard eligibility criteria include:

- Minimum age of 18 years old

- U.S. citizenship or permanent residency

- Valid government-issued identification

- Verifiable source of regular income

- Active checking or savings account

- Contact information including phone and email

- Proof of residence

Income requirements differ by lender and loan amount. Many lenders establish minimum monthly income thresholds ranging from $1,000 to $2,000, though self-employment income and alternative income sources like disability benefits or Social Security often qualify.

Documentation Needed for Quick Approval

Preparing documentation in advance significantly accelerates the emergency loan approval process. Lenders require proof of identity, income, and residence to verify borrower information and assess repayment capability.

| Document Type | Examples | Purpose |

|---|---|---|

| Identification | Driver's license, passport, state ID | Verify identity and age |

| Income Proof | Pay stubs, tax returns, bank statements | Confirm ability to repay |

| Residence Verification | Utility bills, lease agreement, mortgage statement | Establish stability and contact |

| Bank Information | Account statements, voided check | Set up fund disbursement and payments |

Digital applications streamline the documentation process, allowing borrowers to upload photos or scans directly through secure portals. This technology particularly benefits those seeking same-day or next-day funding.

Interest Rates and Fees to Expect

The cost of emergency loans varies considerably based on lender type, borrower creditworthiness, loan amount, and repayment term. Understanding these costs helps borrowers compare options and select the most affordable solution for their situation.

Annual percentage rates (APRs) for emergency loans typically range from 6% to 36% for borrowers with good to excellent credit. Those with fair or poor credit may encounter rates at the higher end of this spectrum or beyond, particularly when working with alternative lenders.

Breaking Down Total Loan Costs

Beyond the interest rate, emergency loans may include various fees that impact the total cost of borrowing. Origination fees, typically 1% to 8% of the loan amount, cover administrative costs and are often deducted from the disbursed funds.

Common fees associated with emergency loans:

- Origination or processing fees (1% to 8%)

- Late payment penalties ($25 to $50 per occurrence)

- Returned payment fees ($15 to $35)

- Prepayment penalties (rare, but check terms)

- Credit check fees (usually waived)

Comparing offers from multiple lenders reveals significant cost differences. A $5,000 emergency loan at 10% APR over three years costs approximately $807 in interest, while the same loan at 20% APR costs $1,687 in interest-a difference of $880.

Residents seeking emergency loans through reputable sources benefit from transparent fee structures and competitive rates. Avoid lenders who obscure costs or refuse to disclose APR before application.

Types of Emergency Loan Options

Emergency funding comes in several forms, each with distinct advantages and considerations. Selecting the right type depends on the urgency of need, available collateral, credit situation, and repayment capacity.

Unsecured personal loans represent the most common emergency loan type. These loans require no collateral, relying instead on creditworthiness and income verification. Approval typically takes one to three business days, with funding arriving shortly after.

Payday alternative loans (PALs) from credit unions offer smaller amounts ($200 to $1,000) with application fees capped at $20 and APRs limited to 28%. These products specifically target borrowers who might otherwise turn to predatory payday lenders.

Home equity lines of credit (HELOCs) provide emergency access to funds for homeowners with sufficient equity. While rates are typically lower, the application process takes longer, and your home serves as collateral.

Secured vs. Unsecured Emergency Loans

The distinction between secured and unsecured emergency loans significantly impacts approval odds, interest rates, and risk levels for borrowers.

| Feature | Secured Loans | Unsecured Loans |

|---|---|---|

| Collateral Required | Yes (vehicle, savings, property) | No |

| Typical APR Range | 3% to 12% | 6% to 36% |

| Approval Speed | 2 to 7 days | 1 to 3 days |

| Credit Requirements | More flexible | Moderate to strict |

| Risk to Borrower | Loss of collateral | Credit score damage only |

| Loan Amounts | Higher limits available | Generally lower limits |

Secured loans make sense when you have valuable assets and need larger amounts with lower rates. However, the risk of losing your vehicle or other collateral during a financial emergency may outweigh the cost savings.

Credit Score Impact and Bad Credit Options

Credit scores influence emergency loan approval and terms, but many lenders recognize that financial emergencies don't discriminate based on credit history. Borrowers with scores below 670 still have viable options.

Lenders specializing in bad credit emergency loans focus on current income and employment stability rather than past credit mistakes. These institutions understand that medical bills, divorce, or job loss can temporarily damage credit without reflecting current financial responsibility.

Strategies for obtaining emergency loans with bad credit:

- Apply with lenders who advertise bad credit acceptance

- Consider adding a creditworthy co-signer

- Offer collateral to secure the loan

- Request smaller loan amounts to improve approval odds

- Demonstrate stable employment and income

- Explain credit issues in your application

- Check with local credit unions for relationship-based lending

Credit unions, particularly those serving Louisiana, Mississippi, Tennessee, and Georgia communities, often provide more personalized underwriting than national banks. They may consider factors beyond credit scores, including community ties and existing account relationships.

Building Credit While Managing Emergency Debt

Emergency loans, when managed responsibly, can actually improve credit scores over time. Consistent, on-time payments demonstrate financial reliability and contribute positively to payment history, which accounts for 35% of FICO scores.

Setting up automatic payments eliminates the risk of missed due dates. Even during subsequent financial stress, prioritizing emergency loan payments protects your credit and prevents additional fees.

Alternatives to Traditional Emergency Loans

Before committing to an emergency loan, exploring alternative funding sources may reveal better solutions for specific situations. Some options provide funds faster or at lower costs, depending on circumstances.

Payment plans directly with service providers often cost nothing in interest or fees. Medical facilities, repair companies, and utility companies frequently offer installment arrangements for customers experiencing financial hardship.

Credit card cash advances provide immediate access to funds, though they typically carry high APRs (25% or higher) and additional fees. This option works best for very small amounts needed urgently when repayment can happen within weeks.

Borrowing from retirement accounts through 401(k) loans allows access to your own money without credit checks. However, this strategy carries significant risks, including tax penalties if you leave your job before repayment and lost investment growth.

Community Resources and Assistance Programs

Local and regional assistance programs throughout the Southeast provide emergency financial help without the obligation of repayment. These resources specifically target common emergencies like utility disconnection, housing instability, and medical costs.

Community assistance options include:

- United Way emergency assistance programs

- Local church benevolence funds

- Salvation Army emergency services

- Community Action Agencies

- State emergency assistance programs

- Nonprofit medical bill assistance

- Legal aid societies for fee waivers

While these programs rarely cover entire emergency expenses, they may reduce the amount you need to borrow, lowering overall debt burden and interest costs.

Avoiding Predatory Lending Practices

The urgency of financial emergencies makes borrowers vulnerable to predatory lenders who exploit desperation. Recognizing warning signs protects you from agreements that worsen financial situations rather than resolve them.

Red flags indicating predatory lending:

- APRs exceeding 36% for unsecured personal loans

- Pressure to decide immediately without reviewing terms

- Requests for upfront fees before loan approval

- Loan amounts you cannot reasonably repay

- Rollover or renewal fees that extend debt indefinitely

- Lack of state licensing or registration

- Unwillingness to provide written loan agreements

Payday loans, despite their availability, typically charge APRs of 300% to 400% when annualized. A two-week $500 payday loan with a $75 fee costs an APR of 391%-far exceeding what most consumers can sustainably afford.

Title loans present similar dangers, with average APRs of 300% and the added risk of vehicle repossession. Losing reliable transportation during a financial crisis often creates cascading problems affecting employment and daily life.

Verifying Lender Legitimacy

Taking time to verify lender credentials prevents falling victim to scams or unlicensed operations. Legitimate lenders operate transparently and maintain proper state licensing for consumer lending.

Check lender credentials through state banking departments or the Better Business Bureau. Louisiana, Mississippi, Tennessee, and Georgia each maintain databases of licensed lenders operating within their borders.

Read online reviews from multiple sources, but recognize that emergency loan borrowers often leave feedback only when extremely satisfied or dissatisfied. Look for patterns in complaints rather than individual negative reviews.

Managing Emergency Loan Repayment

Successfully repaying emergency loans requires planning and discipline, particularly when the underlying financial situation remains challenging. Creating a repayment strategy before accepting funds sets you up for success.

Budget adjustment becomes necessary when adding a new monthly payment. Review discretionary spending categories like dining out, entertainment subscriptions, and non-essential purchases to identify areas for temporary reductions.

Track all debt obligations in one place, listing amounts, due dates, interest rates, and minimum payments. This comprehensive view helps prioritize payments when funds are tight and prevents overlooking obligations.

Strategies for Difficult Repayment Situations

When circumstances prevent making scheduled payments, proactive communication with your lender often leads to workable solutions. Many lenders prefer modified payment arrangements over default and collections.

- Contact your lender immediately when you anticipate payment difficulty

- Request hardship programs that may temporarily reduce payments

- Ask about skip-payment options during genuine emergencies

- Explore refinancing if interest rates have decreased since origination

- Consider debt consolidation if managing multiple high-interest obligations

- Seek credit counseling from nonprofit agencies for comprehensive planning

Ignoring payment problems compounds difficulties through late fees, increased interest rates, credit damage, and potential legal action. Lenders appreciate borrowers who acknowledge challenges and work toward solutions.

Smart Borrowing During Emergencies

Emergency situations demand quick decisions, but smart borrowing requires balancing urgency with careful evaluation. Taking several hours to compare options can save hundreds or thousands of dollars over the loan term.

Pre-qualifying with multiple lenders allows rate comparison without impacting credit scores. Most lenders now offer soft credit checks during initial qualification, revealing estimated rates and terms before formal application.

Borrow only what you genuinely need for the immediate emergency. While lenders may approve larger amounts, additional debt creates unnecessary financial burden and interest costs. Resist the temptation to address non-urgent expenses with emergency funds.

Understanding loan terms before signing prevents surprises. Review the repayment schedule, confirming that monthly payments fit comfortably within your budget after essential expenses. Consider whether income fluctuations might affect your ability to maintain consistent payments.

Emergency loans serve as crucial financial tools when unexpected expenses arise, providing fast access to funds during stressful situations. By understanding eligibility requirements, comparing rates and terms, avoiding predatory lenders, and planning for repayment, borrowers can navigate emergencies without falling into long-term financial hardship. Whether you're facing medical bills, home repairs, or other urgent needs across Louisiana, Mississippi, Tennessee, or Georgia, Standard Financial offers flexible financing solutions with personalized service, working with clients regardless of past credit challenges to find the right emergency loan for your situation.

No comment yet, add your voice below!