Understanding your financial position requires more than just checking your bank balance. The ability to gather, interpret, and apply financial insights transforms how consumers approach borrowing, budgeting, and long-term planning. Whether you're considering a personal loan for home improvements or refinancing existing debt, access to quality financial information shapes every decision you make. The difference between a strategic financial move and a costly mistake often comes down to the depth of insights you possess before taking action.

What Are Financial Insights and Why Do They Matter

Financial insights represent the actionable understanding derived from analyzing various sources of economic and personal financial data. These insights go beyond raw numbers to reveal patterns, opportunities, and potential risks in your financial situation.

For consumers navigating lending decisions, financial insights encompass several critical areas:

- Credit profile analysis showing how lenders view your borrowing history

- Debt-to-income ratios that determine loan eligibility

- Market interest rate trends affecting borrowing costs

- Personal spending patterns revealing budget optimization opportunities

- Economic indicators influencing future financial planning

The FINRA Foundation’s research on consumer financial decision-making demonstrates that consumers prioritize information credibility when making financial choices. This underscores the importance of sourcing insights from reliable channels rather than anecdotal advice or unverified claims.

The Role of Data in Personal Financial Planning

Modern consumers have unprecedented access to financial data, yet many struggle to convert this information into meaningful insights. Understanding which metrics matter most for your specific situation creates a foundation for sound decision-making.

Credit scores represent one of the most impactful data points in consumer lending. These three-digit numbers influence not just loan approval but also interest rates, terms, and borrowing limits. However, the score itself is just the starting point. True financial insights come from understanding the factors behind the score-payment history, credit utilization, account age, and recent inquiries.

Gathering Reliable Financial Information

The quality of your financial insights depends entirely on the reliability of your information sources. In an era of information overload, distinguishing between credible data and noise becomes essential for making informed borrowing decisions.

Primary Sources for Consumer Financial Data

Your personal financial records form the foundation of any meaningful analysis. Bank statements, pay stubs, tax returns, and existing loan documents provide the raw data needed to assess your current position and borrowing capacity.

| Information Source | What It Reveals | Update Frequency |

|---|---|---|

| Credit Reports | Payment history, accounts, inquiries | Monthly |

| Bank Statements | Income, expenses, cash flow patterns | Real-time |

| Tax Returns | Annual income, deductions, liabilities | Annually |

| Loan Statements | Current balances, interest rates, terms | Monthly |

| Pay Stubs | Current income, deductions, consistency | Bi-weekly/Monthly |

Beyond personal records, consumers benefit from understanding broader economic trends. The Federal Reserve Bank of Philadelphia’s Economic Insights publication offers quarterly analysis of economic policy and regional economic conditions that can affect local lending markets across states like Louisiana, Mississippi, Tennessee, and Georgia.

Evaluating Information Credibility

Not all financial information carries equal weight. When researching lending options or financial strategies, consider the source's expertise, transparency, and potential biases.

Government agencies and regulatory bodies provide unbiased economic data and consumer protection guidelines. Established financial institutions offer market research and lending trend analysis. Academic research delivers peer-reviewed findings on consumer finance behavior and outcomes.

Conversely, approach with caution any source that promises unrealistic results, lacks transparency about methodologies, or has clear conflicts of interest. The comprehensive guide to financial data sources emphasizes the importance of cross-referencing multiple reliable sources before making significant financial decisions.

Applying Financial Insights to Borrowing Decisions

Raw data becomes valuable only when transformed into actionable financial insights that guide specific decisions. For consumers considering personal loans, this transformation involves analyzing both personal circumstances and market conditions.

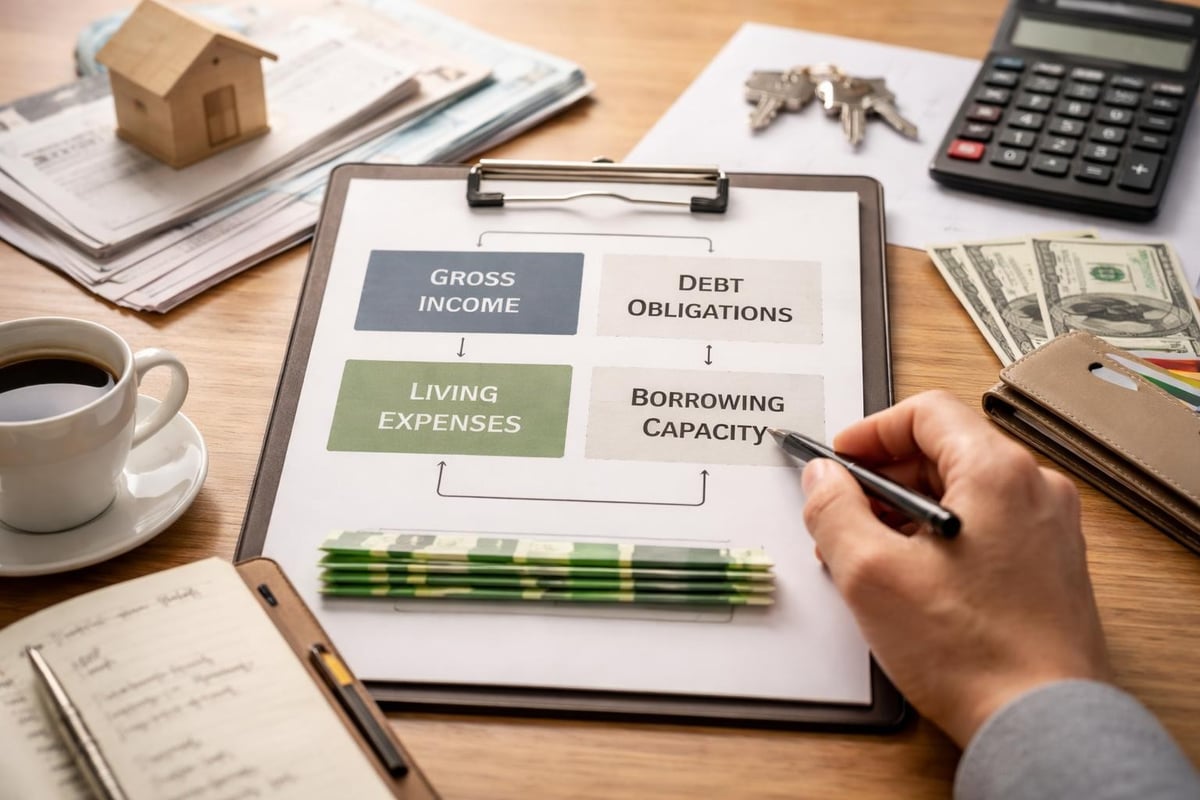

Assessing Your True Borrowing Capacity

Many consumers focus solely on whether they can get approved for a loan, overlooking the more important question of whether they should take on that debt. Financial insights help answer both questions.

Calculate your debt-to-income ratio by dividing monthly debt payments by gross monthly income. Lenders typically prefer ratios below 43%, though this varies by loan type and lender standards. However, just because you qualify at 43% doesn't mean that level of debt aligns with your financial goals.

Consider these factors when evaluating borrowing capacity:

- Current monthly obligations including rent, utilities, existing debt payments

- Income stability accounting for job security and income variability

- Emergency fund status ensuring you maintain financial buffers

- Near-term expenses like vehicle repairs or medical needs

- Long-term goals such as retirement savings or education funding

Comparing Loan Products and Terms

Financial insights enable meaningful comparisons between different lending options. A lower interest rate doesn't automatically make one loan superior to another when you account for fees, terms, and flexibility.

Create a comparison framework that evaluates:

- Annual Percentage Rate (APR) reflecting true borrowing cost

- Loan terms balancing monthly payment affordability with total interest paid

- Fees and charges including origination, prepayment, and late payment penalties

- Flexibility options such as payment modification or refinancing opportunities

- Customer service quality impacting your experience throughout the loan term

For borrowers with past credit issues, specialized lenders often provide more favorable terms than traditional banks. Understanding this market segmentation represents a valuable financial insight that opens doors previously considered closed.

Leveraging Financial Insights for Different Loan Purposes

Different borrowing needs require tailored analytical approaches. The financial insights most relevant for a home improvement loan differ from those critical for medical expense financing or educational funding.

Home Improvement Financing Decisions

When considering loans for home improvements, the decision involves both immediate financial capacity and long-term property value implications.

Key financial insights for home improvement loans:

- Expected return on investment for specific improvements

- Current home equity position and appreciation trends

- Contractor cost estimates versus market averages

- Energy savings potential offsetting monthly loan payments

- Impact on property tax assessments

Regional real estate markets significantly influence these calculations. Home improvement investments in growing markets may deliver substantially different returns than identical improvements in declining areas.

Medical Expense and Emergency Financing

Medical expense loans require different analytical considerations, often under time pressure that limits extensive research.

Prioritize these financial insights when facing medical financing decisions:

- Insurance coverage gaps and out-of-pocket maximums

- Provider payment plan options before seeking external financing

- Tax deductibility of medical expenses exceeding income thresholds

- Loan terms flexibility accounting for recovery periods affecting income

- Total cost comparison between financing options and credit cards

The analysis of investment information sources highlights how evaluating multiple channels of information leads to more informed decisions, a principle equally applicable to consumer lending.

Education and Career Development Funding

Educational loans represent an investment in future earning potential, requiring unique financial insights that balance current costs against projected returns.

| Education Financing Factor | Short-Term Impact | Long-Term Consideration |

|---|---|---|

| Tuition Costs | Immediate borrowing need | Credential value in target industry |

| Living Expenses | Monthly budget strain | Income potential post-completion |

| Program Duration | Extended debt accumulation | Career advancement timeline |

| Employment Prospects | Current income reduction | Salary increase projections |

| Skills Acquired | Time away from work | Marketability enhancement |

Monitoring and Updating Your Financial Insights

Financial insights aren't static. Market conditions, personal circumstances, and lending landscapes constantly evolve, requiring ongoing monitoring and analysis to maintain relevant understanding.

Establishing Regular Review Cycles

Create a structured approach to updating your financial knowledge and reassessing your position. Monthly reviews of spending patterns and debt progress, quarterly assessments of credit reports and scores, and annual comprehensive financial evaluations provide a rhythm for maintaining current insights.

Monthly monitoring priorities:

- Bank account balances and spending trends

- Credit card utilization rates

- Loan payment confirmation and balance reduction

- Budget variances and adjustment needs

Quarterly review focus:

- Credit report accuracy across all three bureaus

- Interest rate environment changes

- Refinancing opportunity evaluation

- Emergency fund adequacy

Annual comprehensive analysis:

- Total debt load and repayment progress

- Income growth and stability assessment

- Financial goal advancement

- Insurance coverage adequacy

- Retirement savings trajectory

Recognizing When to Seek Refinancing

Market conditions and improved personal financial positions often create refinancing opportunities that reduce borrowing costs or improve loan terms. The ability to recognize these moments represents valuable financial insight.

Consider refinancing evaluation when you experience credit score improvements of 50+ points, interest rates drop 1% or more below your current rate, your debt-to-income ratio improves significantly, or you need to adjust monthly payment amounts to align with changed circumstances.

Building Financial Literacy for Better Insights

The capacity to generate meaningful financial insights strengthens with improved financial literacy. Understanding fundamental concepts transforms how you interpret data and make decisions.

Core Concepts Every Borrower Should Understand

Compound interest affects both debt accumulation and savings growth. Grasping how interest compounds daily, monthly, or annually reveals the true cost of borrowing and the value of early debt repayment.

Amortization schedules show how each payment divides between principal and interest over a loan's life. Early payments predominantly cover interest, while later payments reduce principal more substantially. This insight influences decisions about extra payments and refinancing timing.

Opportunity cost represents what you give up when choosing one financial path over another. Every borrowing decision involves opportunity costs worth evaluating against alternatives.

The trusted financial news sources that provide actionable market insights can help consumers stay informed about economic conditions affecting lending decisions.

Developing Your Analytical Framework

Create a personal system for evaluating financial decisions that incorporates your values, goals, and circumstances. This framework should include decision criteria that matter most to you, minimum standards for acceptable options, information sources you trust, and processes for comparing alternatives objectively.

Your analytical framework evolves as your financial situation changes. The considerations most important when establishing credit differ from those relevant when managing substantial assets or planning retirement.

Regional Economic Factors Affecting Lending

Understanding regional economic conditions provides context for lending decisions, particularly when working with lenders focused on specific geographic areas like Louisiana, Mississippi, Tennessee, and Georgia.

State-Specific Economic Indicators

Each state presents unique economic characteristics influencing employment stability, income growth potential, and overall financial health of residents.

Louisiana's economy balances energy sector dependence with growing healthcare and technology industries. Economic diversification efforts affect long-term income stability for borrowers in different sectors.

Mississippi's economic landscape features strong agricultural and manufacturing bases alongside emerging industries. Understanding sector-specific trends helps borrowers assess job security and income projections.

Tennessee's growth markets, particularly Nashville and Memphis, create different lending environments than rural areas. Real estate appreciation, cost of living trends, and employment opportunities vary significantly across the state.

Georgia's economic strength in Atlanta contrasts with challenges in rural regions. Regional economic disparities influence both borrowing needs and repayment capacity.

Impact of Local Economic Conditions on Borrowing

Regional unemployment rates, median income levels, and cost of living indices all affect borrowing decisions. The economic data sources for research offer authoritative information useful for understanding regional economic conditions.

A loan that makes perfect sense in a low cost-of-living area might strain finances in a more expensive region, even at identical income levels. Similarly, employment in stable local industries provides more security than jobs in volatile sectors.

Technology Tools Enhancing Financial Insights

Modern technology democratizes access to sophisticated financial analysis previously available only to professionals. Consumers can now leverage tools that provide real-time insights into spending, saving, and borrowing decisions.

Digital Financial Management Platforms

Budgeting apps, credit monitoring services, and loan comparison platforms offer powerful capabilities for gathering and analyzing financial data. These tools aggregate information from multiple accounts, categorize transactions automatically, identify spending trends, and provide personalized recommendations based on your financial patterns.

The key lies in selecting tools that integrate with your financial institutions, maintain strong security protocols, offer insights relevant to your goals, and present information in formats you understand and will actually use.

Automated Alerts and Monitoring

Technology enables proactive financial management through automated alerts for unusual account activity, approaching credit utilization thresholds, upcoming payment due dates, interest rate changes on variable-rate products, and opportunities for refinancing or consolidation.

These automated systems transform reactive financial management into proactive optimization, helping you catch problems early and capitalize on opportunities promptly.

Making Peace with Past Credit Challenges

For many consumers, past credit issues create anxiety that prevents them from seeking financial insights that could improve their situation. Understanding how credit rehabilitation works and recognizing that past challenges don't permanently define your financial future represents an important mindset shift.

How Credit Recovery Actually Works

Credit scores reflect your recent behavior more heavily than distant history. Payment history from the past two years carries more weight than older information. This means consistent positive financial behavior steadily improves your credit profile regardless of past difficulties.

Strategic actions for credit improvement:

- Establishing consistent on-time payment patterns across all obligations

- Reducing credit utilization below 30% of available limits

- Avoiding new credit inquiries except when necessary

- Disputing inaccurate information on credit reports

- Building positive credit history through manageable new accounts

The Fidelity overview of fundamental analysis resources emphasizes how accessing public records and various data sources supports more informed decisions, a principle applicable to understanding your own credit situation.

Finding Lenders Who Specialize in Credit Rebuilding

Not all lenders evaluate applications identically. Some specialize in working with borrowers rebuilding credit, offering more flexible underwriting criteria that consider factors beyond credit scores alone.

These specialized lenders often evaluate recent payment patterns, current income stability, employment history, and overall financial trajectory rather than focusing primarily on past credit events. This approach opens opportunities for consumers who have stabilized their finances but haven't yet rebuilt their credit scores to optimal levels.

Understanding and applying financial insights empowers you to make borrowing decisions aligned with both your immediate needs and long-term goals. By gathering reliable information, analyzing your unique situation, and staying informed about market conditions, you position yourself for financial success regardless of past challenges. Standard Financial specializes in helping consumers across Louisiana, Mississippi, Tennessee, and Georgia access flexible financing solutions tailored to their circumstances, including options for those rebuilding credit. Whether you need funding for home improvements, medical expenses, or education, our team provides the personalized guidance and lending options to support your financial journey.

No comment yet, add your voice below!