When you apply for a personal loan, the advertised interest rate isn't the only cost you'll encounter. Many lenders charge an origination fee, a one-time upfront expense that covers the administrative work required to process your application and fund your loan. This fee can significantly impact the total cost of borrowing, especially for consumers seeking financing for home improvements, medical expenses, or education. Understanding how this charge works and what influences its amount empowers you to make informed decisions about your financing options and potentially negotiate better terms.

What Is an Origination Fee

An origination fee is a charge that lenders assess to cover the costs associated with processing, underwriting, and funding a new loan. Origination fees typically range from 1% to 8% of the total loan amount, though the specific percentage varies based on the lender, loan type, and borrower qualifications. For a $10,000 personal loan with a 5% origination fee, you would pay $500 upfront, though this amount is usually deducted from the loan proceeds rather than paid separately out of pocket.

The fee compensates lenders for the work involved in evaluating your application, reviewing your credit history, verifying your income, and completing the necessary documentation. This process requires staff time, technology systems, and compliance resources that represent genuine business costs for lending institutions.

How Origination Fees Are Collected

Most lenders deduct the origination fee directly from the loan disbursement. If you're approved for a $15,000 loan with a 4% fee, you'll receive $14,400 after the $600 fee is subtracted. However, you'll repay the full $15,000 plus interest according to your loan agreement.

Some lenders may allow you to add the fee to the principal balance instead of deducting it upfront. While this means you receive the full requested amount, you'll pay interest on the fee throughout the loan term, increasing your total borrowing cost.

Types of Loans That Charge Origination Fees

Origination fees appear across various lending products, though the amounts and calculation methods differ significantly. Understanding which loans typically include these charges helps you budget accurately and compare offers effectively.

Personal Loans

Personal loan origination fees vary considerably among lenders. According to NerdWallet’s analysis of personal loans, fees typically range from 1% to 6% of the loan amount, with the specific percentage often tied to your creditworthiness. Borrowers with excellent credit may qualify for lower fees or have them waived entirely, while those with challenged credit histories might face higher charges.

Mortgage Loans

Mortgage origination fees follow different structures than personal loans. The Consumer Financial Protection Bureau explains that these fees cover various services including processing, underwriting, and loan officer compensation. Unlike percentage-based personal loan fees, mortgage origination charges may appear as flat fees or combinations of percentage-based and fixed costs.

Student Loans

Federal student loans include origination fees that the government sets annually. For the 2025-2026 academic year, Direct Subsidized and Unsubsidized Loans carry origination fees that are deducted from each loan disbursement. Private student loans may or may not charge origination fees depending on the lender's policies.

Factors That Influence Origination Fee Amounts

Several variables determine how much you'll pay in origination fees when securing financing. Recognizing these factors helps you understand your loan offers and identify opportunities for negotiation.

Credit Score and Credit History

Your credit profile significantly impacts origination fee amounts. Lenders view borrowers with higher credit scores as lower risk, which often translates to reduced fees. Someone with a credit score above 750 might pay just 1% to 2%, while a borrower with a score below 630 could face fees of 5% to 8% on the same loan amount.

Past credit issues don't automatically disqualify you from favorable terms. Many lenders, particularly those specializing in consumer lending across the Southeast, evaluate your complete financial picture rather than relying solely on credit scores.

Loan Amount and Term

The size and duration of your loan influence fee calculations. Larger loans may carry lower percentage-based fees because the lender's fixed costs represent a smaller proportion of the total amount. A $5,000 loan might have a 6% fee while a $25,000 loan from the same lender carries just 3%.

Longer loan terms can also affect fees. Extended repayment periods increase the lender's risk exposure, potentially resulting in higher origination charges to offset this risk.

Lender Business Model

Different lenders structure their compensation differently. Online lenders often charge higher origination fees but offer lower interest rates, while traditional banks might charge lower fees but higher rates. Credit unions frequently waive origination fees entirely for members in good standing.

| Lender Type | Typical Fee Range | Other Considerations |

|---|---|---|

| Traditional Banks | 0% – 3% | May require existing relationship |

| Online Lenders | 1% – 8% | Often lower interest rates |

| Credit Unions | 0% – 2% | Membership requirements apply |

| Consumer Finance Companies | 2% – 6% | More flexible credit requirements |

The True Cost of Origination Fees

Understanding the real impact of origination fees requires looking beyond the percentage to calculate the actual dollar amount and how it affects your loan's annual percentage rate (APR). This comprehensive view reveals the true cost of borrowing.

APR Versus Interest Rate

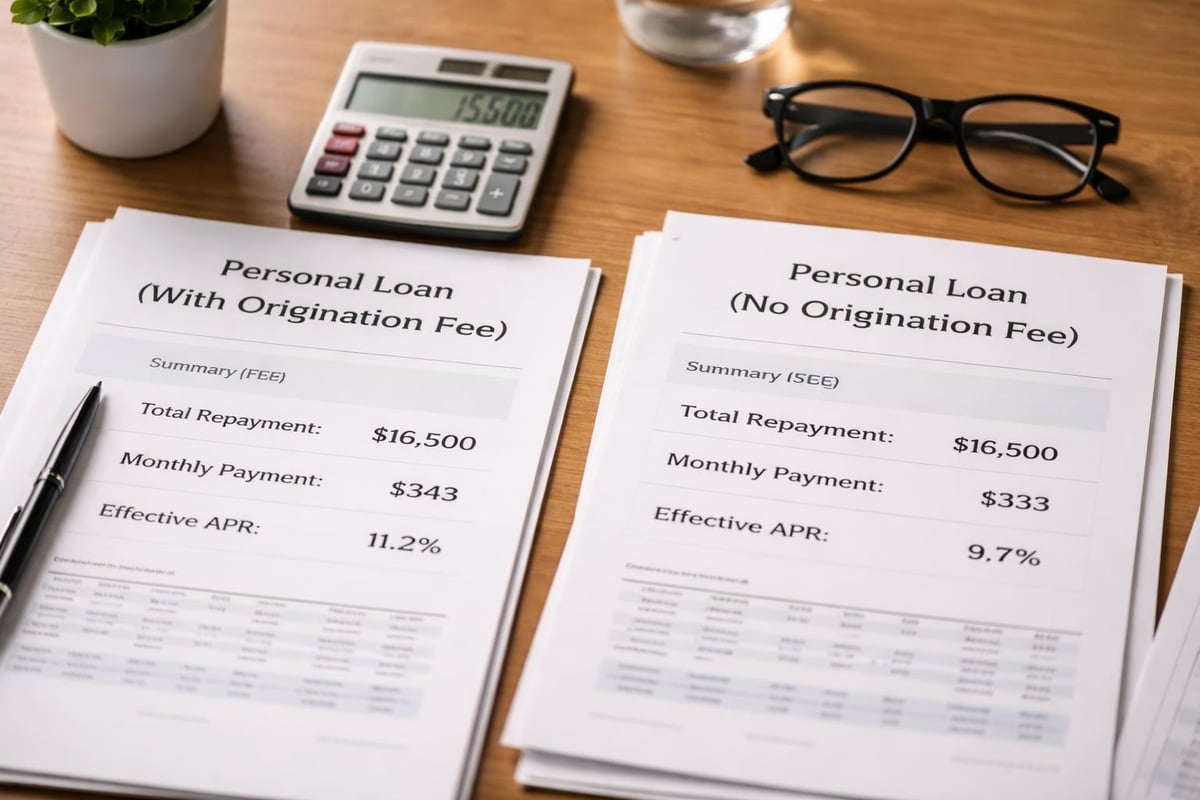

The interest rate advertises what you'll pay on the principal balance, but the APR includes the origination fee and other charges spread across the loan term. A loan with a 10% interest rate and 5% origination fee might carry an APR of 12% or higher depending on the repayment period.

This distinction matters when comparing offers. A loan advertising 8% interest with a 6% origination fee could cost more than one offering 10% interest with no fee, especially for shorter loan terms.

Calculating Total Loan Costs

To determine your actual borrowing cost, add the origination fee to the total interest you'll pay over the loan term. For a three-year $10,000 loan at 12% interest with a 5% origination fee, you'd pay approximately $2,000 in interest plus $500 in fees, totaling $2,500 beyond the principal.

Strategies for Reducing or Avoiding Origination Fees

While origination fees are standard practice, they're not always set in stone. Several approaches can help you minimize these costs or eliminate them entirely.

Negotiation Tactics

Many borrowers don't realize that origination fees are often negotiable. Here's how to approach this conversation:

- Research competitor rates before applying to understand market standards

- Highlight your creditworthiness by emphasizing strong payment history and stable income

- Request fee waivers for existing customers or those bringing multiple accounts

- Consider rate trade-offs by accepting a slightly higher interest rate in exchange for eliminating the fee

Shopping Around for Better Terms

Comparing offers from multiple lenders remains your most powerful tool for reducing costs. Request quotes from at least three to five lenders, ensuring you compare both fees and interest rates. Some institutions specializing in consumer lending across Louisiana, Mississippi, Tennessee, and Georgia may offer more competitive fee structures based on regional market conditions.

Timing Your Application

Your financial situation affects fee calculations. Applying after improving your credit score, paying down existing debts, or increasing your income can qualify you for better terms. Even a modest credit score improvement of 20 to 30 points might reduce your fee by one or two percentage points.

When Origination Fees Make Sense

Despite adding upfront costs, origination fees don't necessarily make a loan a bad deal. Certain circumstances justify these charges when weighed against the complete loan package.

Lower Interest Rates

Some lenders structure their pricing to charge higher origination fees while offering significantly reduced interest rates. For longer-term loans, the interest savings can far exceed the upfront fee cost. Running the numbers on total repayment amounts, not just comparing individual components, reveals whether this trade-off benefits you.

Access to Needed Funds

When you need financing for urgent expenses like medical bills or critical home repairs, the origination fee becomes a secondary concern. The value of accessing funds quickly when alternatives are limited often outweighs the fee cost, particularly when the fee is just 1% to 3% of the loan amount.

Credit Building Opportunities

For borrowers working to establish or rebuild credit, loans with origination fees from lenders who report to all three credit bureaus provide valuable credit-building opportunities. The fee becomes an investment in your financial future if the loan helps you demonstrate responsible payment behavior.

Origination Fees and Regulatory Guidelines

Lending regulations protect consumers from excessive fees while giving lenders flexibility to structure their pricing. Understanding these protections helps you recognize when fees exceed reasonable bounds.

Federal Regulations

Various federal regulations govern origination fees across different loan types. Federal regulations specify maximum origination fees for certain mortgage products, ensuring lenders cannot charge unlimited amounts. These caps protect consumers while allowing lenders to recover legitimate business costs.

Consumer lending regulations require clear disclosure of all fees before loan consummation. Lenders must present origination fees prominently in loan documents, enabling borrowers to understand total costs before signing agreements.

State-Level Protections

Individual states may impose additional restrictions on origination fees beyond federal requirements. States throughout the Southeast, including Louisiana, Mississippi, Tennessee, and Georgia, maintain consumer protection laws that regulate lending practices and fee structures. These regulations vary by state, creating different lending environments across the region.

Red Flags to Watch For

Not all origination fees represent fair compensation for legitimate services. Recognizing warning signs helps you avoid predatory lending practices.

- Excessive fees above 8% to 10% of the loan amount, especially for borrowers with decent credit

- Hidden charges not disclosed upfront or buried in fine print

- Pressure tactics pushing you to sign quickly without time to review terms

- Unwillingness to explain what services the fee covers

- Additional junk fees layered on top of the origination charge

Comparing Disclosure Documents

Legitimate lenders provide clear, comprehensive disclosure documents that itemize all fees and charges. Review these documents carefully, comparing the origination fee to the lender's stated services. If the documentation seems vague or the lender resists providing written fee schedules, consider it a red flag warranting further investigation.

Alternative Loan Structures Without Origination Fees

Some lenders structure their products differently, eliminating origination fees while building costs into other areas of the loan agreement. Understanding these alternatives helps you evaluate whether traditional fee-based loans or alternative structures serve your needs better.

No-Fee Personal Loans

Several lenders advertise no-fee personal loans that eliminate origination charges entirely. These products typically compensate through slightly higher interest rates or by targeting borrowers with excellent credit who present minimal risk. The absence of upfront fees means you receive the full loan amount, though you'll want to verify the interest rate doesn't exceed what you'd pay with a fee-based loan.

Credit Cards and Lines of Credit

Personal lines of credit and credit cards rarely charge origination fees, instead earning revenue through interest and transaction fees. For ongoing expenses or situations where you need flexible access to funds rather than a lump sum, these products might offer better value than traditional installment loans with origination fees.

Making Informed Borrowing Decisions

Origination fees represent just one component of your total borrowing cost. Effective comparison requires examining the complete financial picture, including interest rates, repayment terms, penalties, and your specific needs.

Creating a Comparison Framework

Develop a standardized approach to evaluating loan offers:

- Calculate total repayment including principal, interest, and all fees

- Determine actual funds received after fee deductions

- Review monthly payment amounts to ensure affordability

- Examine prepayment penalties that might restrict early payoff

- Assess lender reputation through customer reviews and regulatory records

Questions to Ask Lenders

Before accepting any loan offer, clarify these essential points with your lender:

- What specific services does the origination fee cover?

- Can the fee be reduced or waived based on my qualifications?

- How is the fee collected (deducted or added to principal)?

- What is the APR when all fees are included?

- Are there additional fees beyond the origination charge?

Regional Considerations for Southeast Borrowers

Consumers seeking financing across Louisiana, Mississippi, Tennessee, and Georgia encounter regional market dynamics that influence origination fees and lending practices. Local economic conditions, state regulations, and competitive landscapes create variations in available loan products.

Market Competition

Areas with numerous lending options typically see more competitive fee structures as lenders vie for customers. Metropolitan areas like New Orleans, Jackson, Memphis, and Atlanta often feature more lenders and potentially better terms than rural regions with limited competition.

Economic Factors

Regional employment patterns, income levels, and cost of living affect both loan demand and lender risk assessments. These factors influence how lenders structure their fees and what terms they offer to borrowers in different areas throughout the Southeast.

| State | Average Credit Score (2026) | Typical Fee Range | Common Loan Uses |

|---|---|---|---|

| Louisiana | 668 | 3% – 6% | Home repairs, medical expenses |

| Mississippi | 662 | 3% – 7% | Debt consolidation, emergencies |

| Tennessee | 679 | 2% – 5% | Home improvements, education |

| Georgia | 683 | 2% – 5% | Various personal needs |

Understanding origination fees empowers you to evaluate loan offers accurately and negotiate better terms. While these charges add to your borrowing costs, comparing the complete loan package including fees, interest rates, and repayment terms helps you identify financing that truly serves your needs. Whether you're planning home improvements, managing medical expenses, or pursuing educational goals, Standard Financial offers transparent lending solutions with flexible terms designed for borrowers throughout Louisiana, Mississippi, Tennessee, and Georgia, including those working to overcome past credit challenges.

No comment yet, add your voice below!