Securing financing can feel overwhelming when your credit history doesn't reflect your current financial stability or your income doesn't meet traditional lending standards. A personal loan with cosigner offers a viable path forward for borrowers who need additional support to qualify for financing. This arrangement brings together two parties: the primary borrower who needs the funds and a cosigner who agrees to share responsibility for repayment. Understanding how this process works, the requirements involved, and the implications for everyone involved helps you make informed decisions about your borrowing options.

Understanding the Personal Loan with Cosigner Structure

A personal loan with cosigner involves two individuals taking legal responsibility for debt repayment. The primary borrower receives the loan proceeds and makes monthly payments, while the cosigner essentially acts as a guarantor who promises to cover payments if the borrower defaults.

Lenders view cosigned loans favorably because they reduce risk. When you apply with a cosigner who has strong credit and stable income, the lender gains assurance that payments will continue even if your circumstances change. This security often translates into better loan terms for borrowers who might otherwise face rejection or unfavorable rates.

Key Differences Between Cosigners and Co-Borrowers

Many people confuse cosigners with co-borrowers, but these roles carry distinct characteristics:

- Cosigner: Provides credit backing without receiving loan proceeds or ownership rights to purchased items

- Co-borrower: Shares equal access to funds and equal ownership of assets purchased with the loan

- Payment responsibility: Cosigners typically only pay if the primary borrower defaults, while co-borrowers share payment obligations from day one

- Credit reporting: Both arrangements appear on credit reports for all parties involved

Understanding how cosigners differ from co-borrowers helps you determine which arrangement suits your situation best. For most personal loans where one person needs the funds, a cosigner arrangement provides the appropriate structure.

Who Benefits from a Personal Loan with Cosigner

Several borrower profiles find value in cosigner arrangements. Young adults building credit histories often need parental support to qualify for their first personal loans. College graduates seeking funds for relocation or professional certification frequently turn to family members with established credit.

Individuals recovering from past financial setbacks represent another significant group. Even if you've experienced bankruptcy, foreclosure, or extended unemployment, a personal loan with cosigner can provide access to necessary funds while you rebuild your credit profile.

Common Scenarios Where Cosigners Make Sense

| Borrower Situation | Challenge | How Cosigner Helps |

|---|---|---|

| Recent graduate | Limited credit history | Established credit profile improves approval |

| Career changer | Income verification gap | Cosigner income strengthens application |

| Credit rebuilding | Past delinquencies | Positive cosigner history offsets negatives |

| Debt consolidation | High utilization ratio | Combined income improves debt-to-income ratio |

Self-employed borrowers with fluctuating income documentation also benefit from cosigner support. Traditional lenders often struggle to verify irregular income streams, but a cosigned application alleviates these concerns.

Qualifying Requirements for Cosigners

Not everyone qualifies to serve as a cosigner on a personal loan. Lenders impose specific requirements to ensure cosigners can fulfill their obligations if needed. Understanding these eligibility requirements and associated risks helps both parties enter the arrangement with clear expectations.

Credit Score Thresholds

Most lenders require cosigners to maintain credit scores above 670, with many preferring scores exceeding 700. The cosigner's credit profile should demonstrate:

- Consistent on-time payment history across all accounts

- Low credit utilization ratios (typically below 30%)

- Minimal recent hard inquiries

- No active collections or charge-offs

- Established credit history spanning several years

Higher cosigner credit scores generally unlock better interest rates and terms for the primary borrower.

Income and Employment Verification

Lenders verify that cosigners maintain stable employment and sufficient income to cover existing obligations plus the new loan payment. Documentation typically includes:

- Recent pay stubs covering the past 30-60 days

- W-2 forms or tax returns from the previous two years

- Employment verification letters from current employers

- Bank statements showing consistent deposits

- Additional income documentation (rental properties, investments, retirement income)

The combined debt-to-income ratio of borrower and cosigner strengthens the overall application, improving approval likelihood.

Benefits of Obtaining a Personal Loan with Cosigner

Adding a qualified cosigner to your loan application delivers multiple advantages beyond simple approval. These benefits can significantly impact your immediate financial situation and long-term credit building efforts.

Interest Rate Reduction: Lenders reserve their most competitive rates for lowest-risk applications. A strong cosigner transforms a potentially risky application into an attractive lending opportunity, potentially saving thousands in interest over the loan term.

Higher Borrowing Limits: With additional income and creditworthiness backing your application, lenders often approve larger loan amounts than you'd qualify for independently. This increased capacity helps you fully fund necessary expenses without seeking multiple financing sources.

Faster Approval Process: Applications with cosigners typically move through underwriting more quickly because they present less risk. Lenders spend less time scrutinizing borderline applications when a qualified cosigner provides additional security.

Credit Building Opportunities

A personal loan with cosigner creates opportunities to establish or rebuild credit when managed responsibly. Each on-time payment reports to credit bureaus under your name, gradually improving your credit profile. After 12-24 months of consistent payments, many borrowers refinance independently, removing cosigner obligations while maintaining better rates than originally available.

Risks and Responsibilities for All Parties

While cosigned loans offer significant benefits, both borrowers and cosigners must understand the serious obligations involved. These arrangements create legally binding responsibilities that persist until full loan repayment.

Primary Borrower Responsibilities

As the primary borrower, you carry the main obligation to make timely monthly payments. Missing payments damages not only your credit but also your cosigner's financial profile. This dual impact amplifies the consequences of financial mismanagement.

Your relationship with your cosigner depends on maintaining payment obligations. Family dynamics often suffer when financial agreements deteriorate, creating stress that extends beyond monetary concerns.

Cosigner Exposure and Obligations

Cosigners assume substantial financial risk when signing loan documents. The legal responsibilities and financial implications deserve careful consideration before committing to this arrangement.

Full Repayment Liability: If you default, your cosigner becomes immediately responsible for the entire remaining balance, not just missed payments. Lenders can pursue cosigners for payment without first exhausting collection efforts against primary borrowers.

Credit Impact: Late payments and defaults appear on cosigner credit reports with the same severity as if they had borrowed the funds directly. A single 30-day late payment can drop credit scores by 60-100 points.

Future Borrowing Capacity: The cosigned loan appears as debt on the cosigner's credit report, affecting their debt-to-income ratio for their own future borrowing needs. This can complicate mortgage applications, auto loans, or other major purchases.

Finding Lenders That Accept Cosigners

Not all lenders accept cosigner applications for personal loans. As lending practices evolved through 2025 and into 2026, many large banks eliminated cosigner options, focusing instead on technology-driven underwriting models that rely solely on primary borrower qualifications.

Regional lenders, credit unions, and community-focused financial institutions more commonly accept cosigner arrangements. These organizations maintain traditional underwriting approaches that value relationship banking and individualized assessment.

Where to Search for Cosigner-Friendly Lenders

- Credit unions: Member-focused institutions frequently accommodate cosigner requests

- Community banks: Regional banks often maintain flexibility for local customers

- Online lenders: Some digital platforms specifically market cosigner programs

- Consumer finance companies: Specialized lenders serving credit-challenged borrowers

When researching options, comparing lenders that accept cosigners helps you identify the most favorable terms for your specific situation. Pay attention to origination fees, prepayment penalties, and minimum credit requirements that vary significantly across institutions.

Application Process for Cosigned Personal Loans

Applying for a personal loan with cosigner requires coordination between both parties and thorough documentation preparation. Understanding the process helps you move efficiently from application to funding.

Step-by-Step Application Timeline

- Pre-qualification: Submit basic information to check potential rates without hard credit inquiries

- Cosigner commitment: Confirm cosigner willingness and verify they meet minimum requirements

- Documentation gathering: Collect required financial documents for both borrower and cosigner

- Formal application: Complete full application with both parties' information

- Underwriting review: Lender evaluates combined creditworthiness and income

- Approval and terms: Receive loan offer with specific rate, amount, and repayment schedule

- Document signing: Both parties sign legally binding loan agreements

- Funding: Receive loan proceeds via direct deposit or check

Most lenders complete this process within 2-7 business days for straightforward applications, though complex situations may require additional time.

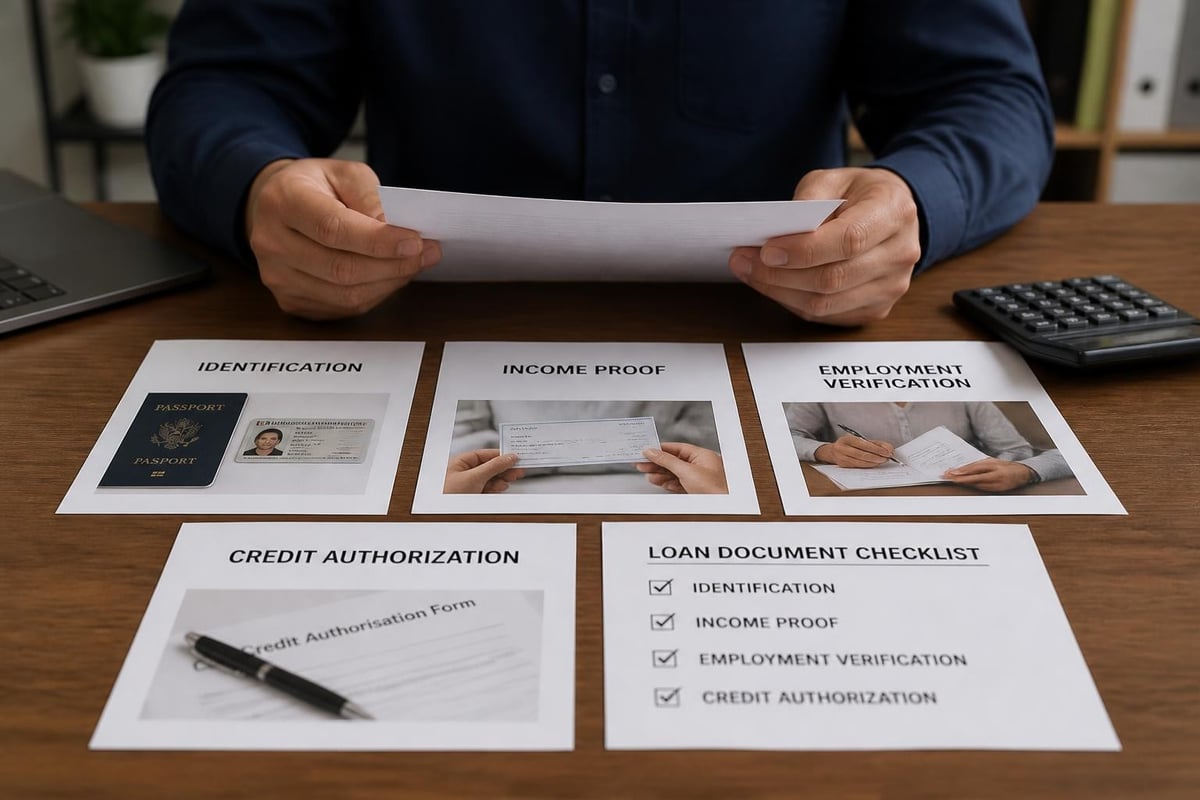

Required Documentation Checklist

| Document Type | Primary Borrower | Cosigner |

|---|---|---|

| Government ID | Required | Required |

| Proof of income | Required | Required |

| Employment verification | Required | Required |

| Bank statements | Typically required | Often required |

| Credit authorization | Required | Required |

| Proof of address | Sometimes required | Sometimes required |

Having all documentation ready when you begin the application prevents delays and demonstrates financial organization to underwriters.

Managing Your Cosigned Personal Loan Successfully

Once approved, managing your personal loan with cosigner responsibly protects both parties' financial interests and preserves important relationships. Establishing clear communication patterns and payment systems from the start prevents misunderstandings later.

Payment Best Practices

Set up automatic payments from your primary checking account to ensure you never miss due dates. Most lenders offer small interest rate discounts (typically 0.25%) for autopay enrollment, creating additional savings while eliminating payment timing concerns.

Create backup payment plans: Identify secondary funding sources you can access if unexpected expenses threaten your ability to make loan payments. Emergency funds, side income, or available credit lines provide safety nets that prevent cosigner involvement.

Maintain open communication: Inform your cosigner immediately if you anticipate payment difficulties. Early notification allows time to develop solutions before missed payments damage credit reports.

Monitoring and Reporting

Both borrowers and cosigners should actively monitor the loan account and credit reports. Many lenders provide online portals where cosigners can view payment history and outstanding balances without making payments themselves.

Review credit reports quarterly to verify accurate payment reporting. Errors occasionally occur, and quick correction prevents long-term credit damage. The three major credit bureaus (Equifax, Experian, TransUnion) each provide annual free credit reports.

Removing a Cosigner from Your Personal Loan

Most borrowers eventually want to release their cosigners from loan obligations, both to restore cosigner borrowing capacity and demonstrate financial independence. Several strategies enable cosigner release, though availability depends on lender policies and loan terms.

Refinancing Into a Solo Loan

The most common cosigner removal method involves refinancing your existing loan in your name only. After making consistent payments for 12-24 months, your improved credit profile may qualify you for independent approval.

Refinancing works best when:

- Your credit score has increased by 50+ points since original approval

- Your income has risen significantly

- Interest rates have decreased since your original loan

- You've paid down at least 20-30% of the principal balance

Formal Cosigner Release Programs

Some lenders offer cosigner release after you've made a specified number of consecutive on-time payments (typically 12-24 months). These programs require formal applications and credit reviews to verify you now qualify independently.

Review your loan agreement to determine if cosigner release provisions exist. Not all lenders offer this option, and requirements vary significantly among those that do.

Alternative Options to Cosigned Personal Loans

While a personal loan with cosigner solves many borrowing challenges, alternative approaches may better suit certain situations. Evaluating all options ensures you select the most appropriate financing method for your circumstances.

Secured Personal Loans

Offering collateral (savings accounts, certificates of deposit, vehicles) can help you qualify for personal loans without involving another person. Secured loans carry lower risk for lenders, potentially delivering competitive rates without cosigner requirements.

The trade-off involves pledging assets that lenders can seize if you default, creating different risk dynamics than cosigned arrangements.

Credit Builder Loans

These specialized products help establish credit history through forced savings programs. You make monthly payments into a locked savings account, and the lender reports positive payment history to credit bureaus. After completing all payments, you receive the accumulated funds.

Credit builder loans work well for long-term credit development but don't provide immediate access to cash like traditional personal loans.

Income-Based Lending Programs

Some modern lenders emphasize income verification over credit scores when making approval decisions. These platforms analyze bank account activity, employment stability, and cash flow patterns rather than relying primarily on credit history.

Understanding various personal loan options helps you determine whether cosigner arrangements truly offer the best solution for your specific financial needs.

Tax and Legal Considerations

Personal loans with cosigners create specific legal relationships and potential tax implications that both parties should understand before signing agreements.

Gift Tax Implications

If a cosigner makes payments on your behalf, the IRS may consider these payments as gifts. For 2026, individuals can gift up to $19,000 annually to another person without triggering gift tax reporting requirements. Amounts exceeding this threshold require filing Form 709, though most people never pay actual gift taxes due to lifetime exemption limits.

Legal Enforcement and Collection

Cosigner agreements constitute legally enforceable contracts. If you default, lenders can pursue collection actions against cosigners including:

- Wage garnishment in states where permitted

- Bank account levies

- Credit reporting damage

- Lawsuits for full loan balances plus fees and interest

Understanding these potential dangers and financial risks emphasizes the serious nature of cosigner commitments.

Impact on Financial Goals and Planning

A personal loan with cosigner affects both parties' broader financial planning beyond the immediate loan relationship. Careful consideration of long-term implications helps everyone make informed decisions aligned with their financial objectives.

For Primary Borrowers

Successfully managing a cosigned loan accelerates credit building and demonstrates financial responsibility. This foundation supports future independent borrowing for major purchases like homes or vehicles. However, taking on debt always involves opportunity costs-funds directed toward loan payments can't simultaneously build emergency savings or retirement accounts.

Balance your immediate financing needs against long-term wealth building priorities to ensure borrowing supports rather than hinders your overall financial health.

For Cosigners

The decision to cosign carries significant weight in personal financial planning. Before committing, cosigners should evaluate:

- How the additional debt obligation affects their own borrowing plans within the next 3-5 years

- Whether their emergency fund can absorb potential loan payments if the borrower defaults

- The relationship value and their confidence in the borrower's commitment to repayment

- Alternative ways to help the borrower that don't involve personal credit exposure

Many financial advisors counsel against cosigning except in carefully considered circumstances where cosigners can afford complete loan repayment without financial hardship.

Special Considerations for Different Loan Purposes

The purpose of your personal loan with cosigner can affect approval likelihood and terms. Lenders view certain loan purposes as lower risk than others, influencing their willingness to work with cosigner applications.

Home Improvement Loans

Personal loans for home improvements often receive favorable consideration because they theoretically increase property values. When you own the home being improved, lenders see additional security even in unsecured personal loan structures. Cosigners with homeownership experience may strengthen these applications particularly effectively.

Medical Expense Financing

Healthcare costs represent unavoidable expenses that lenders generally view sympathetically. A personal loan with cosigner for medical procedures or treatments often moves through approval efficiently because the purpose demonstrates necessity rather than discretionary spending.

Education and Training Costs

Investing in education or professional certification typically improves earning potential, creating better long-term repayment prospects. Lenders appreciate borrowers using funds for income-enhancing purposes, though they may require documentation of enrollment or program acceptance.

Debt Consolidation Applications

Using a personal loan with cosigner to consolidate high-interest credit card debt can improve your financial position while presenting relatively low risk to lenders. The key involves closing or restricting the credit cards being paid off to prevent accumulating new debt while repaying the consolidation loan.

A personal loan with cosigner provides valuable opportunities for borrowers who need additional support to access financing while building credit for future independence. Understanding the requirements, responsibilities, and strategies for successful management protects both borrowers and cosigners throughout the loan term. Whether you need funds for home improvements, medical expenses, education, or other important purposes, Standard Financial offers flexible personal loan options with branch offices throughout Louisiana, Mississippi, Tennessee, and Georgia to serve clients with diverse credit backgrounds and financial situations.

No comment yet, add your voice below!