Managing finances becomes significantly more challenging when income is limited, yet learning how to budget on a low income remains one of the most critical skills for achieving financial stability. Whether you're working toward paying off debt, building an emergency fund, or simply making ends meet each month, a well-structured budget provides the foundation for reaching your financial goals. The good news is that effective budgeting doesn't require a high income; it requires intentional planning, discipline, and the right strategies to maximize every dollar you earn.

Understanding Your Complete Financial Picture

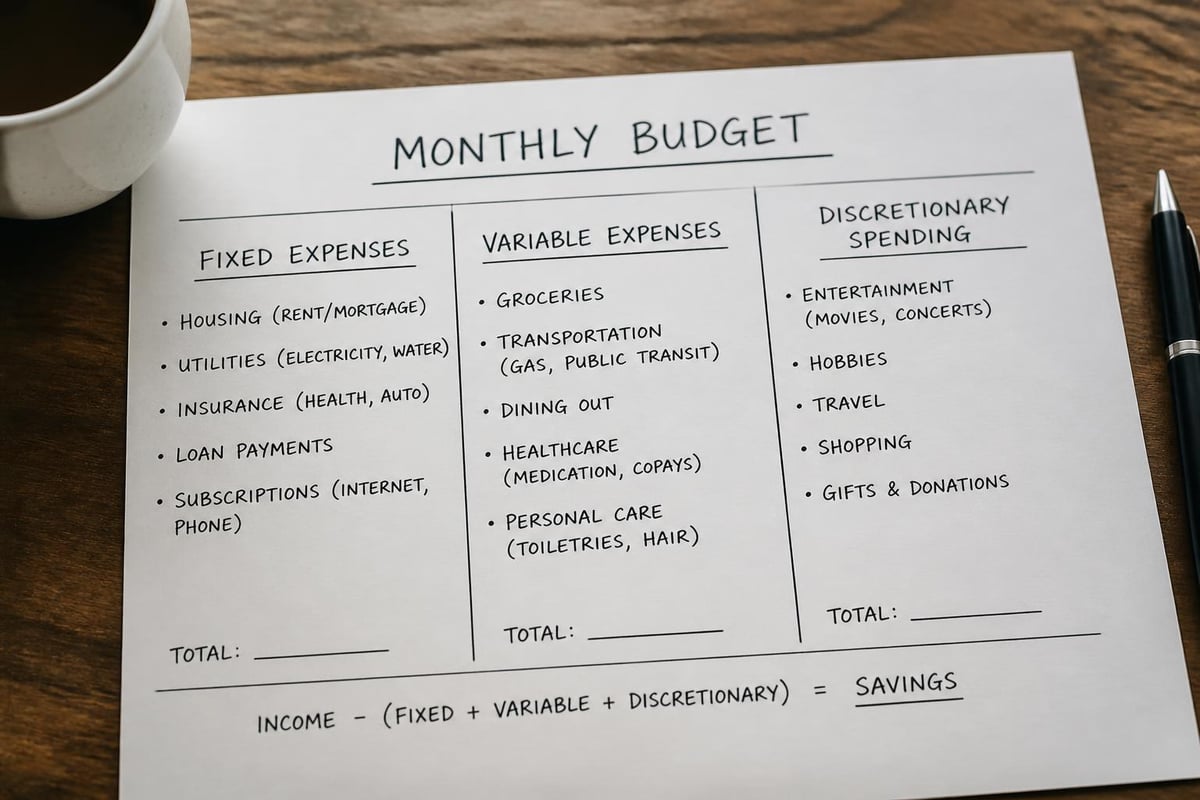

Before implementing any budgeting strategy, you need a clear understanding of your current financial situation. This means documenting every source of income and every expense, no matter how small.

Calculate Your Total Monthly Income

Start by adding up all sources of income you receive each month. Include your primary job, any part-time work, freelance earnings, government assistance, child support, or other regular payments. If your income varies from month to month, calculate an average based on the past three to six months to establish a baseline.

Key income sources to track:

- Wages from employment (after taxes)

- Self-employment or gig economy earnings

- Government benefits or assistance programs

- Child support or alimony payments

- Regular gifts from family members

- Interest or dividend income

For irregular income, conservative estimates work best when learning how to budget on a low income. Underestimating slightly creates a buffer rather than leaving you short at month's end.

Document Every Expense

Tracking expenses reveals where your money actually goes versus where you think it goes. For one full month, record every single purchase, bill payment, and cash transaction. Use a notebook, spreadsheet, or budgeting app to capture this information.

Divide your expenses into fixed costs (rent, car payment, insurance) and variable costs (groceries, gas, entertainment). This distinction becomes crucial when you need to identify areas for potential cuts.

Choosing the Right Budgeting Method

Different budgeting approaches work for different situations. When you're managing limited resources, the method you choose can make the difference between success and frustration.

The Zero-Based Budget Approach

The zero-based budget assigns every dollar a specific purpose before the month begins. Your income minus all planned expenses and savings should equal zero. This method ensures complete control over how to budget on a low income by eliminating unplanned spending.

Here's how it works: If you earn $2,400 monthly, you allocate exactly $2,400 across all categories including savings, debt payments, and expenses. Any leftover money gets assigned to a specific goal rather than sitting idle.

The 50/30/20 Rule Modified for Low Income

The traditional 50/30/20 rule suggests allocating 50% to needs, 30% to wants, and 20% to savings and debt repayment. However, when working with limited income, this breakdown often proves unrealistic.

A modified approach might look like this:

| Budget Category | Traditional | Low-Income Modified |

|---|---|---|

| Needs (housing, food, utilities) | 50% | 65-70% |

| Wants (entertainment, dining out) | 30% | 10-15% |

| Savings & Debt | 20% | 15-20% |

This adjustment recognizes that basic necessities consume a larger percentage of lower incomes while still maintaining focus on debt reduction and emergency savings.

The Pay-Yourself-First Method

This simplified approach prioritizes savings by automatically setting aside a predetermined amount immediately when income arrives. Even if you can only afford $25 or $50 monthly, automating this transfer ensures consistent progress toward financial goals.

The remaining funds cover necessities and other expenses. While this method requires careful monitoring to avoid overspending, it guarantees that savings happen regardless of other financial pressures.

Prioritizing Essential Expenses

When resources are tight, knowing which expenses take priority prevents difficult situations like eviction, utility shutoffs, or repossession.

The Four Walls Concept

Financial experts emphasize covering the "four walls" first: food, shelter, utilities, and transportation. These basics keep you housed, fed, and able to work. Everything else comes after securing these fundamental needs.

Priority ranking for expenses:

- Housing payments (rent or mortgage)

- Essential utilities (electricity, water, heat)

- Basic groceries and food

- Transportation to work

- Required insurance coverage

- Minimum debt payments

- Healthcare and medications

- All other expenses

This hierarchy ensures that you maintain stability while managing limited resources. Medical expenses and certain debts may require higher priority depending on your specific circumstances.

Negotiating and Reducing Essential Costs

Even necessary expenses offer opportunities for reduction. Contact service providers about financial hardship programs, payment plans, or lower-cost alternatives. Many utility companies, internet providers, and insurance companies offer assistance programs specifically designed for customers facing financial constraints.

For housing costs that exceed 30% of income, explore options like finding a roommate, relocating to more affordable housing, or applying for housing assistance programs in your area.

Cutting Costs Without Sacrificing Quality of Life

Learning how to budget on a low income requires creativity in reducing expenses while maintaining reasonable comfort and happiness.

Food and Grocery Strategies

Food represents one of the largest variable expenses with significant savings potential. Meal planning, buying generic brands, shopping sales, and cooking from scratch can reduce grocery bills by 30-50%.

Practical food savings tactics:

- Plan weekly menus around sale items and seasonal produce

- Prepare larger batches and freeze portions for later

- Pack lunches instead of buying meals at work

- Use cashback apps and store loyalty programs

- Buy protein in bulk when prices drop

- Grow herbs or vegetables if space allows

Eliminating or dramatically reducing restaurant meals and takeout creates immediate budget relief. Cooking at home consistently saves hundreds monthly while often providing healthier nutrition.

Transportation and Vehicle Costs

Transportation expenses extend beyond car payments to include insurance, fuel, maintenance, and repairs. Reducing these costs requires strategic thinking.

Consider carpooling, using public transportation for some trips, combining errands to reduce mileage, maintaining proper tire pressure for better fuel economy, and shopping insurance rates annually. If vehicle costs consume an excessive portion of your budget, downsizing to a less expensive, more fuel-efficient car might make financial sense.

Subscription and Service Audits

Review every recurring charge on bank and credit card statements. Streaming services, gym memberships, app subscriptions, and other monthly charges accumulate quickly. Cancel anything you don't actively use and consider rotating services rather than maintaining multiple simultaneously.

Many people discover they're paying for subscriptions they forgot existed or services they can replace with free alternatives.

Building Emergency Savings on Limited Income

Emergency funds prevent minor setbacks from becoming financial disasters. Even when mastering how to budget on a low income, setting aside small amounts consistently builds a crucial safety net.

Start With Micro-Savings Goals

Rather than feeling overwhelmed by recommendations to save three to six months of expenses, begin with achievable targets. Your first goal might be $500, then $1,000, gradually building from there.

| Savings Milestone | Monthly Savings Needed | Time to Goal |

|---|---|---|

| $250 | $25 | 10 months |

| $500 | $25 | 20 months |

| $500 | $50 | 10 months |

| $1,000 | $50 | 20 months |

These timeframes demonstrate that consistent small amounts create real financial cushions over time.

Automate Savings Transfers

Manual savings transfers often get skipped when budgets feel tight. Automating the process removes the decision-making and ensures progress. Schedule transfers for immediately after payday, treating savings as a non-negotiable expense.

Many employers offer direct deposit splitting, allowing you to send a portion of each paycheck directly to savings before you see it in checking. This "out of sight, out of mind" approach works remarkably well for building consistent savings habits.

Finding Extra Money for Savings

Beyond cutting expenses, increasing income accelerates savings progress. Consider selling unused items, taking on temporary seasonal work, freelancing skills you already possess, or participating in the gig economy through delivery services or task-based platforms.

Tax refunds, work bonuses, gifts, or other windfalls should go directly to emergency savings rather than discretionary spending. These irregular income sources can dramatically shorten the timeline for reaching savings goals.

Managing Debt While Budgeting

Debt payments consume significant portions of limited budgets, yet strategic approaches can reduce both balances and stress.

Debt Prioritization Strategies

Two popular methods for tackling multiple debts are the debt snowball and debt avalanche approaches. The snowball method focuses on paying off the smallest balance first for psychological wins, while the avalanche method targets the highest interest rate to minimize total interest paid.

For those learning how to budget on a low income, the snowball method often provides better results because early victories maintain motivation during a long payoff journey.

Refinancing and Consolidation Options

When managing multiple high-interest debts, consolidation through personal loans or refinancing can reduce monthly payments and simplify budgeting. A single monthly payment at a lower interest rate makes budgeting more predictable and potentially saves thousands in interest charges.

Standard Financial offers various personal loan options, including refinancing solutions designed specifically for clients working to improve their financial situations, even those with past credit challenges.

Avoiding New Debt

While eliminating existing debt, preventing new debt is equally important. This requires distinguishing between true emergencies and inconveniences, relying on your emergency fund when possible, and avoiding credit cards for discretionary purchases.

If new debt becomes necessary for genuine emergencies like essential vehicle repairs or medical expenses, exploring options with Standard Financial ensures you get flexible financing terms that work within your budget constraints.

Tracking Progress and Adjusting Your Budget

Budgets aren't static documents. They require regular review and adjustment based on changing circumstances and lessons learned.

Weekly Budget Check-Ins

Spending 15 minutes weekly reviewing transactions prevents month-end surprises. Compare actual spending against budgeted amounts in each category, identifying problems early enough to correct course before overspending significantly.

Weekly reviews also reinforce spending awareness, making you more mindful of purchases throughout the week.

Monthly Budget Reviews

Each month, conduct a comprehensive review examining which categories consistently run over or under budget. Use this information to create more realistic allocations going forward.

Questions for monthly reviews:

- Which expense categories exceeded their budgets?

- Where did I spend less than anticipated?

- Did any unexpected expenses occur?

- What adjustments would improve next month's budget?

- Am I making progress toward financial goals?

This reflection process transforms budgeting from a restrictive exercise into a learning opportunity that continuously improves financial management skills.

Celebrating Small Wins

Acknowledge progress along the way. When you reach a savings milestone, pay off a debt, or successfully stick to your budget for three consecutive months, recognize these achievements. Positive reinforcement makes sustainable behavior change more likely than focusing solely on restrictions and sacrifices.

Tools and Resources for Budget Success

Technology and community resources can simplify budgeting processes and provide support during challenging moments.

Budgeting Apps and Software

Free budgeting apps like Mint, YNAB (You Need A Budget), EveryDollar, and Goodbudget automate transaction tracking, categorization, and reporting. Many connect directly to bank accounts, providing real-time spending updates.

For those preferring simpler approaches, spreadsheet templates or paper budgets work equally well. The best budgeting system is the one you'll actually use consistently.

Community Resources and Assistance Programs

Many communities offer resources for those managing tight budgets. Local nonprofits may provide free financial counseling, food banks reduce grocery costs, utility assistance programs help with bills during difficult months, and community health centers offer affordable healthcare.

Research what's available in Louisiana, Mississippi, Tennessee, and Georgia through local social services departments, United Way chapters, or community action agencies. These resources stretch limited budgets further while you work toward financial stability.

Financial Education Opportunities

Free financial education through library programs, community college workshops, nonprofit organizations, and online resources builds skills for long-term success. Understanding concepts like compound interest, credit scores, and investment basics empowers better financial decisions as income increases.

Increasing Income Opportunities

While expense reduction helps, income growth creates more budget flexibility and faster progress toward financial goals.

Side Hustle Possibilities

The gig economy offers numerous opportunities for supplemental income that fits around existing work schedules. Driving for rideshare services, delivering food or groceries, freelancing specialized skills, tutoring students, or providing virtual assistance all generate additional funds for debt reduction or savings.

Career Advancement Strategies

Investing in skills development through free online courses, certifications, or training programs can lead to promotions or better-paying positions. Many employers offer tuition assistance or professional development programs that cost employees nothing.

Networking within your industry, volunteering for additional responsibilities at current jobs, and regularly updating resumes positions you for advancement opportunities when they arise.

Selling Unused Items

Most households contain hundreds or thousands of dollars worth of unused items. Selling clothes, electronics, furniture, books, or collectibles through online marketplaces generates one-time income boosts for emergency funds or debt payments.

Regular decluttering not only produces extra money but also prevents accumulating possessions that strain limited storage space and budgets.

Common Budgeting Mistakes to Avoid

Understanding frequent pitfalls helps prevent setbacks when implementing how to budget on a low income strategies.

Being Too Restrictive

Budgets that eliminate all discretionary spending rarely succeed long-term. Including small amounts for entertainment, hobbies, or treats prevents the deprivation mentality that leads to budget abandonment.

Even $20 monthly for fun spending provides breathing room that makes restrictions in other categories more tolerable.

Forgetting Irregular Expenses

Annual or semi-annual expenses like car registration, insurance premiums, holiday gifts, or tax preparation fees create budget crises when forgotten. Calculate the annual cost of irregular expenses, divide by twelve, and set aside that amount monthly in a dedicated savings category.

Not Adjusting for Life Changes

Job changes, family additions, relocations, health issues, or other life events require budget modifications. Failing to adjust budgets when circumstances change leads to unrealistic expectations and financial stress.

Review and revise your budget whenever significant life changes occur rather than forcing outdated plans onto new situations.

Giving Up After Mistakes

No one executes a perfect budget immediately. Overspending in categories, forgetting expenses, or making impulse purchases are learning opportunities, not failures. Analyze what happened, adjust the plan, and continue forward rather than abandoning budgeting entirely after setbacks.

Financial management is a skill developed over time through practice and refinement.

Alternative Budgeting Approaches

Traditional budgeting doesn't work for everyone. Alternative methods provide different frameworks that may better suit certain personalities or situations.

The Anti-Budget Method

The “anti-budget” approach simplifies financial management by focusing on three numbers: total income, fixed expenses, and savings goals. After automatically saving and paying fixed costs, the remainder covers variable expenses without detailed tracking.

This method works well for people who find traditional budgeting too restrictive or time-consuming, though it requires discipline to avoid overspending the untracked portion.

The 60/30/10 Budget

The 60/30/10 budgeting method allocates 60% of income to necessities, 30% to discretionary wants, and 10% to savings or debt repayment. This framework provides clear guidelines while remaining flexible within categories.

For low-income budgets where necessities consume more than 60%, this method can be modified to 70/20/10 or even 75/15/10 ratios while maintaining the structural approach.

Cash Envelope System

The envelope system uses physical cash divided into category-specific envelopes. Once an envelope empties, no more spending occurs in that category until the next budgeting period. This tangible, visual approach prevents overspending and creates immediate awareness of remaining funds.

While increasingly challenging in a digital payment world, the envelope system still works effectively for variable categories like groceries, entertainment, and personal spending.

Mastering how to budget on a low income creates financial stability regardless of your current earnings, providing the foundation for future growth and security. By implementing these strategies consistently, tracking progress honestly, and adjusting approaches as needed, you develop financial skills that serve you throughout life. If unexpected expenses or opportunities for debt consolidation arise during your budgeting journey, Standard Financial offers flexible personal loan options designed to work within your budget, with solutions available even if you've faced credit challenges in the past.

No comment yet, add your voice below!