When financial emergencies strike and traditional lending doors seem closed, the promise of no credit check loans guaranteed approval can feel like a lifeline. These financial products target consumers who have experienced credit setbacks, offering quick access to funds without the traditional credit inquiry process. However, understanding the reality behind these loans, their true costs, and the alternatives available is essential for making informed borrowing decisions. The consumer lending landscape has evolved significantly in recent years, and borrowers across Louisiana, Mississippi, Tennessee, and Georgia now have more options than ever before, even when facing credit challenges.

Understanding No Credit Check Loans Guaranteed Approval

The term "no credit check loans guaranteed approval" describes lending products marketed to consumers who may not qualify for traditional financing due to poor credit history or limited credit profiles. These loans promise to skip the hard credit inquiry that typically appears on credit reports and affects credit scores.

What Lenders Actually Mean by Guaranteed Approval

No legitimate lender can truly guarantee approval for every applicant. Understanding what no credit check means reveals that even lenders who skip traditional credit bureau checks still verify income, employment, and basic identification. The "guaranteed approval" language primarily serves as marketing terminology designed to attract borrowers who feel excluded from conventional lending channels.

Most lenders offering these products use alternative verification methods:

- Bank account verification and transaction history analysis

- Proof of steady income through pay stubs or direct deposit records

- Employment verification with current employers

- State-issued identification and address confirmation

- Assessment of debt-to-income ratios using stated income

The approval process focuses less on past credit behavior and more on current ability to repay. This approach provides opportunities for borrowers rebuilding their credit or facing temporary financial hardships.

The True Costs of No Credit Check Loans Guaranteed Approval

Financial products that bypass traditional credit checks carry significantly higher costs than conventional personal loans. Lenders justify these elevated rates by citing increased risk when lending without comprehensive credit history reviews.

Interest Rates and Fee Structures

Borrowers pursuing no credit check loans guaranteed approval often encounter annual percentage rates ranging from 200% to 400% or higher. These rates dwarf the typical personal loan APRs of 6% to 36% available to borrowers with established credit.

| Loan Type | Typical APR Range | Average Loan Term | Common Fees |

|---|---|---|---|

| No Credit Check Loans | 200% – 400%+ | 2 weeks – 6 months | Origination, processing, late payment |

| Traditional Personal Loans | 6% – 36% | 2 – 7 years | Origination (1% – 8%) |

| Credit Union Loans | 7% – 18% | 1 – 5 years | Minimal to none |

The high costs and potential risks associated with these products can trap borrowers in cycles of debt. A $500 loan with a 300% APR for two weeks costs approximately $60 in interest alone, creating a repayment burden of $560.

Additional fees compound these costs. Origination fees, processing charges, and late payment penalties add layers of expense that significantly increase the total borrowing cost. For a $1,000 loan, total repayment amounts frequently exceed $1,400 to $1,600.

Short Repayment Terms Create Pressure

Unlike traditional installment loans with multi-year repayment schedules, no credit check loans guaranteed approval typically require full repayment within days or weeks. This compressed timeline creates financial pressure that many borrowers cannot sustain.

When borrowers cannot meet the initial repayment deadline, they often "roll over" the loan by paying additional fees to extend the term. Each rollover generates new charges while the principal balance remains unchanged, creating an expensive debt cycle that becomes increasingly difficult to escape.

Common Types of No Credit Check Loans Guaranteed Approval

The marketplace for loans without traditional credit checks includes several distinct product categories, each with unique characteristics and risk profiles.

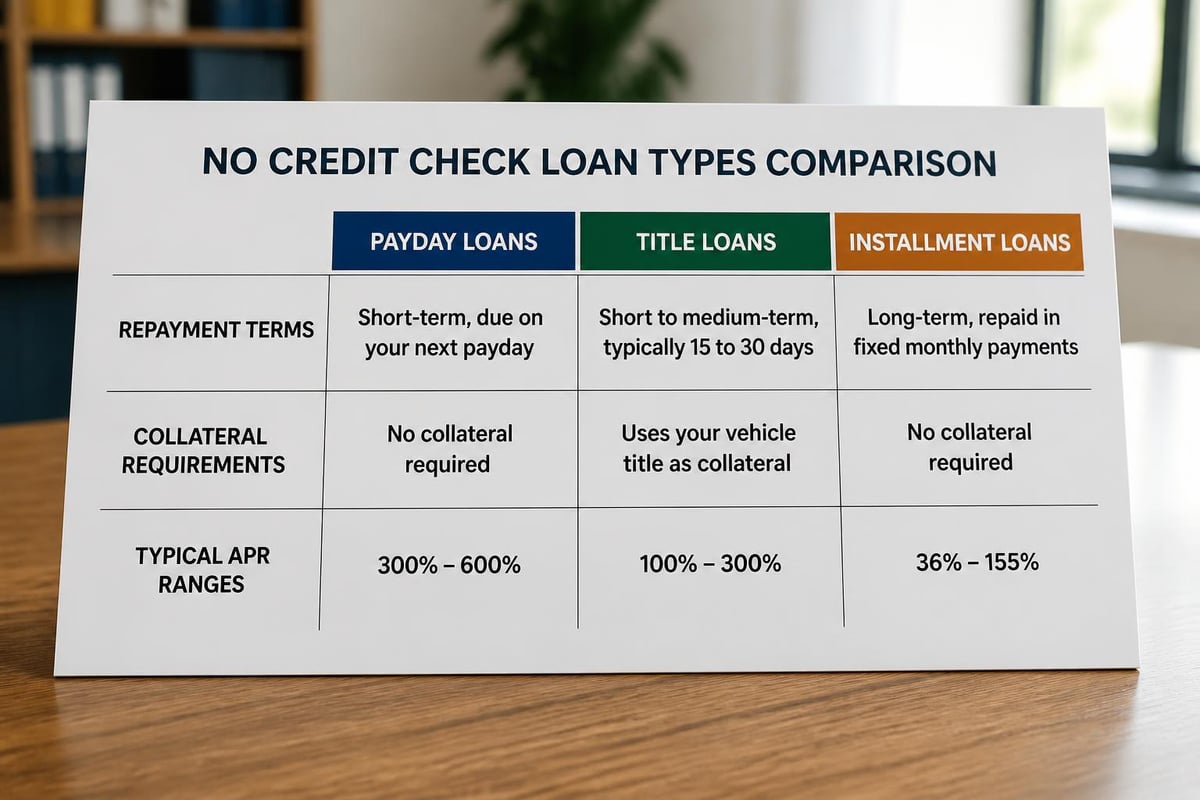

Payday Loans

Payday loans represent the most recognizable no credit check product. These short-term loans typically range from $100 to $1,000 and require repayment on the borrower's next payday, usually within two to four weeks. Lenders secure repayment by requiring post-dated checks or electronic access to borrower bank accounts.

The convenience of payday loans comes with extreme costs. Triple-digit APRs make these products among the most expensive borrowing options available in the consumer lending industry.

Title Loans

Title loans use vehicle ownership as collateral, allowing borrowers to access funds based on their car's value without traditional credit checks. Loan amounts typically range from 25% to 50% of the vehicle's assessed worth.

Key characteristics include:

- Repayment terms of 15 to 30 days

- APRs frequently exceeding 250%

- Risk of vehicle repossession upon default

- Continued vehicle use during the loan period

The risk of losing transportation makes title loans particularly dangerous for borrowers who depend on their vehicles for employment.

Installment Loans Without Credit Checks

Some lenders offer installment loans that skip traditional credit bureau inquiries while providing longer repayment terms than payday products. These loans feature fixed monthly payments over several months to a year, creating more manageable repayment schedules than single-payment payday loans.

How no-credit-check personal loans operate varies by lender, but installment products generally charge lower APRs than payday loans while still maintaining rates substantially higher than traditional lending products. Borrowers across Louisiana, Mississippi, Tennessee, and Georgia increasingly seek these products as middle-ground solutions between predatory payday lending and inaccessible traditional loans.

Risks Beyond High Interest Rates

The financial costs of no credit check loans guaranteed approval represent just one dimension of risk for borrowers considering these products.

Predatory Lending Practices

The no credit check lending sector attracts some operators who engage in deceptive or predatory practices. Borrowers should watch for warning signs including:

- Pressure to borrow more than needed

- Unclear fee disclosures or hidden charges

- Automatic rollover arrangements without explicit consent

- Collection practices that violate consumer protection laws

- Upfront fees before loan approval or funding

The risks associated with no-credit-check loans extend beyond immediate financial costs to include long-term consequences that affect financial stability and wellbeing.

Impact on Financial Health

While no credit check loans guaranteed approval may not initially affect credit scores through hard inquiries, defaulting on these loans creates serious consequences. Many lenders report delinquencies to collection agencies, which subsequently report to credit bureaus, damaging credit profiles.

The debt cycle created by high-cost borrowing diverts funds from essential expenses and savings goals. Borrowers caught in repeated borrowing patterns often struggle to:

- Build emergency savings funds

- Pay regular household expenses on time

- Address the underlying financial challenges that prompted initial borrowing

- Qualify for more affordable credit products in the future

Legal and Regulatory Considerations

State regulations governing no credit check loans guaranteed approval vary significantly across the United States. Louisiana, Mississippi, Tennessee, and Georgia each maintain distinct regulatory frameworks that establish maximum interest rates, loan amounts, and term limits.

Some states prohibit certain high-cost lending products entirely, while others impose caps on fees and interest charges. Borrowers should verify that lenders operate legally within their state and comply with all applicable consumer protection regulations.

Safer Alternatives to No Credit Check Loans Guaranteed Approval

Consumers facing credit challenges have access to multiple borrowing alternatives that provide more favorable terms than no credit check loans guaranteed approval.

Credit Union Payday Alternative Loans

Many federal credit unions offer Payday Alternative Loans (PALs) designed specifically for borrowers seeking small-dollar credit. These products feature:

- Loan amounts from $200 to $1,000 (PAL I) or $200 to $2,000 (PAL II)

- Application fees capped at $20

- APRs limited to 28%

- Repayment terms from one to twelve months

Credit union membership requirements are typically minimal, and these institutions focus on member financial wellness rather than profit maximization.

Traditional Personal Loans for Bad Credit

Established lenders, including banks and specialized consumer lending companies, offer personal loans designed for borrowers with imperfect credit. While these products involve credit checks, approval criteria extend beyond credit scores to include:

- Income stability and employment history

- Total debt obligations relative to income

- Banking relationship history

- Collateral or co-signer availability

Interest rates for bad credit personal loans typically range from 18% to 36%, substantially lower than no credit check alternatives while still accessible to borrowers with credit challenges.

Payment Plans and Hardship Programs

Before seeking new loans, consumers should explore payment arrangements with existing creditors. Many service providers offer:

Hardship programs for customers experiencing temporary financial difficulties, including reduced payments or interest rate adjustments.

Extended payment plans that spread outstanding balances over longer timeframes without additional fees.

Settlement options for seriously delinquent accounts that reduce total amounts owed.

Medical providers, utility companies, and educational institutions frequently work with customers to establish manageable payment schedules that avoid the need for high-cost borrowing.

Family and Community Resources

Personal loans from family members or friends, while potentially awkward to arrange, eliminate interest charges and provide flexible repayment terms. Formalizing these arrangements through written agreements protects both parties and clarifies expectations.

Community assistance programs, religious organizations, and nonprofit agencies offer emergency financial support for specific needs such as utility bills, rent assistance, or medical expenses. These resources provide grants or interest-free loans that help bridge temporary financial gaps.

How to Evaluate No Credit Check Lenders

Borrowers who determine that no credit check loans guaranteed approval represent their best option should carefully evaluate potential lenders to minimize risks and identify the most reasonable terms available.

Verification and Licensing

Legitimate lenders maintain proper state licensing and comply with all applicable regulations. Borrowers should:

- Verify lender licensing through state financial regulatory agencies

- Check for complaints filed with the Better Business Bureau

- Review customer feedback on independent review platforms

- Confirm physical business addresses and contact information

- Research the lender's reputation and operational history

Whether no-credit-check loans are safe depends largely on lender legitimacy and regulatory compliance.

Comparing Terms Across Lenders

Interest rates and fees vary significantly among no credit check lenders. Obtaining quotes from multiple sources enables borrowers to identify the least expensive options. Key comparison points include:

| Comparison Factor | What to Evaluate | Questions to Ask |

|---|---|---|

| APR | Total annual cost of borrowing | What is the APR including all fees? |

| Loan Amount | Principal borrowed | What amount do I actually need? |

| Repayment Term | Time to full repayment | Can I realistically repay in this timeframe? |

| Fees | All charges beyond interest | What are origination, processing, and late fees? |

| Rollover Policies | Extension options and costs | What happens if I cannot repay on time? |

Reading the Fine Print

Loan agreements contain critical information about borrower rights, lender remedies, and dispute resolution procedures. Before signing, borrowers should understand:

- Exact repayment amounts and due dates

- Consequences of late or missed payments

- Lender's collection procedures and policies

- Process for disputing errors or unauthorized charges

- Options for early repayment and any associated penalties

Questions about contract terms should be addressed before finalizing agreements. Legitimate lenders provide clear answers and allow time for borrower review and consideration.

Building Credit to Avoid Future Need for No Credit Check Products

Long-term financial health depends on developing positive credit profiles that provide access to affordable mainstream lending products. Borrowers currently relying on no credit check loans guaranteed approval can take steps to improve their creditworthiness.

Secured Credit Cards

Secured credit cards require cash deposits that serve as credit limits, eliminating risk for card issuers while allowing consumers to demonstrate responsible credit use. Monthly on-time payments reported to credit bureaus gradually build positive payment history.

After six to twelve months of responsible use, many secured card issuers refund security deposits and convert accounts to traditional unsecured cards, further improving available credit and credit utilization ratios.

Credit-Builder Loans

Specialized credit-builder loans help consumers establish payment history without receiving immediate loan proceeds. Instead, borrowers make fixed monthly payments into savings accounts, accessing the accumulated funds only after completing all scheduled payments.

These arrangements create positive credit bureau reporting while simultaneously building emergency savings, addressing two fundamental aspects of financial stability.

Consistent Payment History

Payment history accounts for approximately 35% of FICO credit scores, making it the single most influential factor in credit calculations. Consistently paying all obligations on time, including:

- Rent payments (when reported to credit bureaus)

- Utility bills

- Phone and internet services

- Installment loans and credit cards

- Student loans

This systematic approach gradually rebuilds damaged credit profiles and expands access to affordable financing options.

Regional Lending Landscape in the Southeast

Borrowers in Louisiana, Mississippi, Tennessee, and Georgia operate within distinct regulatory environments that shape available lending products and consumer protections.

State-Specific Regulations

Each southeastern state maintains unique approaches to regulating high-cost lending:

Louisiana permits payday lending with restrictions on loan amounts and fees, while requiring lenders to verify borrower income and ability to repay.

Mississippi allows payday loans up to $500 with fees capped at specific percentages of loan amounts and restrictions on simultaneous loans.

Tennessee regulates both payday and title lending through licensing requirements and fee limitations designed to protect consumers.

Georgia prohibits payday lending entirely, though consumers still access certain high-cost installment products through licensed lenders.

Understanding state-specific regulations helps borrowers identify legal lending options and recognize potentially unlicensed or predatory operators.

Local Lending Options

The southeastern region hosts numerous consumer lending institutions that work with borrowers facing credit challenges. Branch-based lenders offer advantages including:

- In-person consultations that clarify loan terms and address questions

- Relationship-based lending that considers factors beyond credit scores

- Community connections and local accountability

- Flexible products designed for regional economic conditions

Consumers often find more favorable terms and customer service through established regional lenders compared to online-only operations with minimal borrower support infrastructure.

While no credit check loans guaranteed approval provide quick access to funds for borrowers with credit challenges, they carry substantial costs and risks that often create more financial problems than they solve. Understanding the true nature of these products, exploring safer alternatives, and working toward improved creditworthiness empowers consumers to make better borrowing decisions. For Louisiana, Mississippi, Tennessee, and Georgia residents seeking flexible financing options that accommodate past credit issues while providing reasonable terms and personalized service, Standard Financial offers personal loans for various needs including home improvements, medical expenses, and education, with refinancing options designed to help you achieve your financial goals.

No comment yet, add your voice below!