Finding the best car loan refinance solution can transform your monthly budget and save you thousands of dollars over the life of your vehicle loan. Whether you're struggling with high interest rates from your original financing, experiencing changes in your financial situation, or simply looking to reduce monthly expenses, refinancing your auto loan offers a strategic pathway to better financial health. The refinancing landscape in 2026 presents numerous opportunities for borrowers across the credit spectrum, particularly in the Southeast region where competitive lending markets create favorable conditions for consumers seeking improved loan terms.

Understanding Car Loan Refinancing Fundamentals

Car loan refinancing involves replacing your existing auto loan with a new one, ideally with better terms that align with your current financial goals. This process allows you to renegotiate interest rates, adjust payment schedules, and potentially access equity you've built in your vehicle.

The mechanics of refinancing are straightforward yet require careful consideration. When you refinance, a new lender pays off your existing loan and creates a fresh agreement with new terms. Your credit profile, vehicle value, and market conditions all influence the rates and terms available to you.

Key Benefits of Refinancing Your Auto Loan

Refinancing delivers multiple financial advantages depending on your specific circumstances:

- Lower monthly payments by extending your loan term or securing a reduced interest rate

- Decreased total interest costs through better APR offers from competitive lenders

- Improved cash flow by freeing up hundreds of dollars each month for other expenses

- Simplified finances by consolidating multiple payment obligations

- Flexible term adjustments to align with your evolving financial goals

According to AutoInsurance.com’s review of the best auto loans for refinancing, many borrowers reduce their interest rates by 2-4 percentage points when market conditions align favorably with their improved credit profiles.

When Refinancing Makes Financial Sense

Timing your refinancing decision correctly maximizes your financial benefits. Several scenarios indicate you're positioned for successful refinancing:

Interest rate improvements represent the most common trigger. If market rates have dropped since your original financing or your credit score has improved significantly, you may qualify for substantially better terms. Even a one percentage point reduction can translate to meaningful savings on a $25,000 loan.

Credit score enhancements open new opportunities. Borrowers who have raised their credit scores by 50-100 points since their original purchase often discover they now qualify for prime or near-prime rates that weren't previously accessible.

Financial hardship situations sometimes necessitate refinancing to reduce monthly obligations. Extending your loan term increases total interest paid but can provide crucial breathing room during challenging periods.

Evaluating the Best Car Loan Refinance Lenders

The best car loan refinance providers distinguish themselves through competitive rates, transparent processes, and flexible qualification criteria. Understanding what separates exceptional lenders from average ones helps you make informed decisions.

Top-Tier Lender Characteristics

Premium refinancing lenders share several distinguishing features that benefit borrowers:

| Lender Quality | Excellent | Good | Average |

|---|---|---|---|

| APR Range | 3.99% – 8.99% | 7.99% – 12.99% | 11.99% – 18.99% |

| Credit Score Minimum | 580+ | 620+ | 640+ |

| Processing Time | 24-48 hours | 3-5 days | 7-14 days |

| Term Flexibility | 12-84 months | 24-72 months | 36-60 months |

These benchmarks help you assess whether a lender offers genuinely competitive terms or merely adequate options. NerdWallet’s overview of top cash-out auto refinance loans provides detailed comparisons of lenders across multiple categories, enabling side-by-side evaluation.

Regional Lenders Versus National Institutions

Borrowers in Louisiana, Mississippi, Tennessee, and Georgia benefit from choosing between regional specialists and national platforms. Regional lenders often provide personalized service, flexible underwriting for unique situations, and faster processing times due to localized decision-making.

National lenders counter with extensive digital infrastructure, 24/7 application processing, and sometimes more competitive rates due to economies of scale. The best car loan refinance choice depends on your priorities: personal service and flexibility versus technological convenience and potentially lower rates.

Qualification Requirements for Optimal Refinancing

Understanding what lenders evaluate during the refinancing process positions you for approval and better terms. Multiple factors influence your eligibility and the rates you'll receive.

Credit Profile Considerations

Your credit score serves as the primary determinant of available rates and terms. However, the best car loan refinance opportunities extend beyond perfect credit scenarios.

Prime borrowers (720+ credit scores) access the most favorable rates, often in the 4-7% APR range depending on loan term and vehicle age. These borrowers enjoy streamlined approvals and minimal documentation requirements.

Near-prime borrowers (660-719 scores) still qualify for competitive offers, typically ranging from 7-11% APR. This segment represents the majority of refinancing applicants and benefits significantly from shopping multiple lenders.

Subprime borrowers (580-659 scores) face higher rates but remain eligible for refinancing, particularly through lenders specializing in credit-challenged situations. Rates typically range from 11-18% APR, still potentially lower than their current terms if those were secured during credit difficulties.

Vehicle and Loan Specifications

Beyond creditworthiness, lenders evaluate your vehicle's characteristics and existing loan details:

- Vehicle age: Most lenders refinance vehicles up to 10-12 years old

- Mileage limits: Typically 125,000 miles maximum, though some extend to 150,000

- Loan-to-value ratio: Best rates require 125% LTV or lower

- Minimum loan amount: Usually $5,000-$7,500 to justify processing costs

- Remaining term: At least 12-18 months left on current loan

Capital One’s auto loan refinancing process clearly outlines these requirements, demonstrating how transparent lenders set appropriate expectations from the start.

Strategic Approaches to Maximize Refinancing Benefits

Securing the best car loan refinance terms requires more than simply accepting the first offer. Strategic preparation and informed decision-making significantly impact your outcomes.

Preparing Your Financial Profile

Timing your application strategically can improve your approval odds and available rates. Allow at least six months between your original loan and refinancing application to demonstrate payment history. Similarly, avoid applying immediately after major credit changes like new credit cards or other loans.

Gathering comprehensive documentation accelerates processing and demonstrates organization to lenders. Essential documents include:

- Current loan statement showing payoff amount and account number

- Proof of income (recent pay stubs or tax returns)

- Vehicle registration and insurance documentation

- Driver's license or government-issued identification

- Proof of residence (utility bill or lease agreement)

Improving your credit profile before applying can shift you into better rate tiers. Simple actions like paying down credit card balances below 30% utilization or disputing inaccurate items on your credit report can boost scores by 20-50 points within 60-90 days.

Comparing Multiple Refinancing Offers

The difference between accepting the first offer and shopping thoroughly often amounts to thousands of dollars over your loan term. Credible’s platform to compare auto loan refinance options demonstrates how modern comparison tools simplify this process, allowing you to evaluate multiple lenders simultaneously.

Rate shopping windows protect your credit score. Credit bureaus typically treat multiple auto loan inquiries within 14-45 days as a single inquiry, allowing comprehensive comparison without score damage.

Consider these factors when evaluating competing offers:

| Comparison Factor | Why It Matters | What to Look For |

|---|---|---|

| APR | Determines total interest paid | Lowest rate for your credit tier |

| Monthly payment | Affects budget flexibility | Sustainable amount for your income |

| Loan term | Impacts total cost and equity | Balance between payment and interest |

| Fees | Adds to total cost | Minimal or zero origination fees |

| Prepayment penalties | Limits early payoff flexibility | No penalties for extra payments |

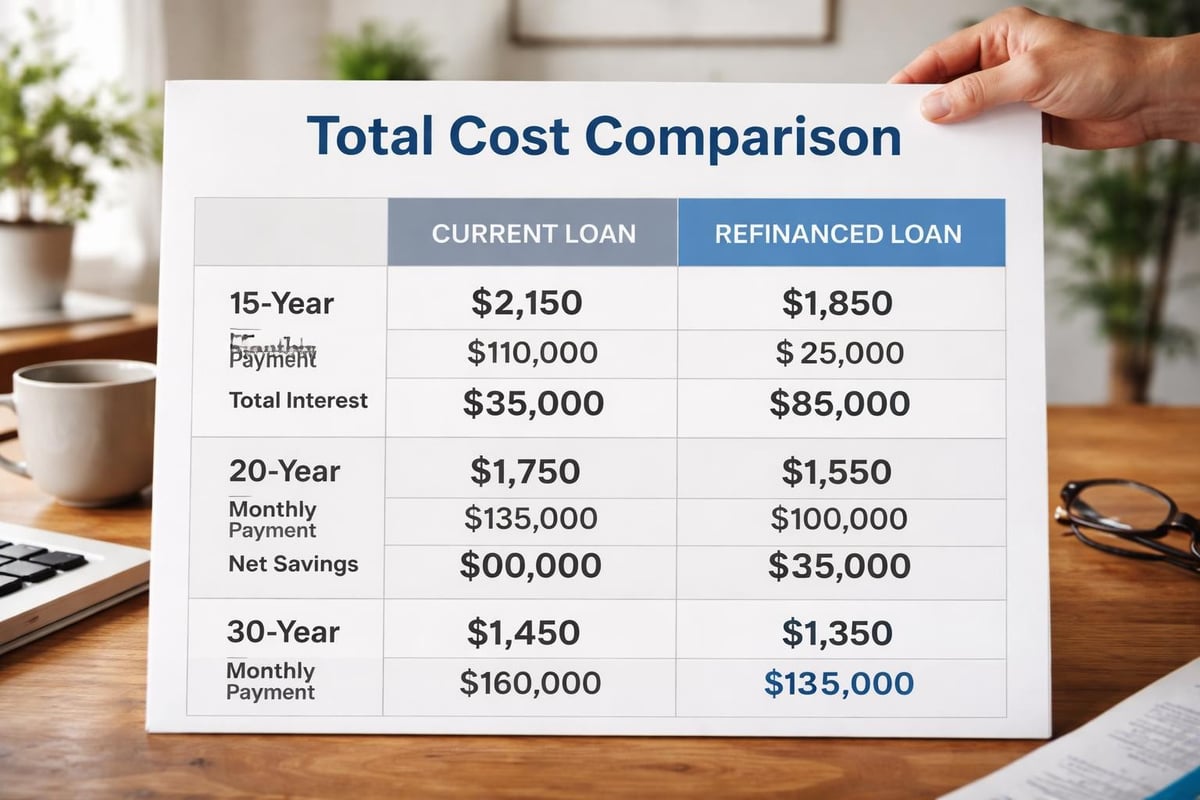

Understanding Total Cost Versus Monthly Payment

A common refinancing mistake involves focusing exclusively on monthly payment reduction while ignoring total loan cost. Extending your term from 36 to 60 months might reduce monthly payments by $150 but could add $2,000-$3,000 in total interest charges.

Calculate your break-even point by dividing any fees by your monthly savings. If refinancing costs $500 in fees and saves $75 monthly, you break even after 6.7 months. Any time beyond that represents genuine savings.

The best car loan refinance balances immediate cash flow relief with long-term cost efficiency. WalletHub’s comparison of auto loan refinance rates provides calculators that help visualize these trade-offs across different term lengths and rate scenarios.

Common Refinancing Mistakes to Avoid

Even experienced borrowers sometimes make errors that diminish refinancing benefits or create new financial challenges. Awareness of these pitfalls helps you navigate the process successfully.

Rolling Negative Equity Into New Loans

Negative equity (owing more than your vehicle's worth) presents complications during refinancing. While some lenders allow rolling this deficit into your new loan, doing so increases your total borrowing amount and may result in higher rates due to elevated loan-to-value ratios.

If you're significantly underwater, consider these alternatives:

- Make extra principal payments for 6-12 months before refinancing

- Refinance only the amount equal to your vehicle's value

- Wait until natural depreciation aligns more closely with your paydown schedule

Ignoring Prepayment Penalties on Current Loans

Some existing auto loans include prepayment penalties that charge fees for early payoff. Always review your current loan agreement before proceeding with refinancing applications. A penalty of $500-$1,000 might eliminate your first year of interest savings, fundamentally changing your refinancing calculus.

Overlooking Regional Lending Opportunities

National comparison platforms provide valuable starting points, but they don't always feature regional lenders offering competitive programs tailored to specific geographic markets. Borrowers in Louisiana, Mississippi, Tennessee, and Georgia sometimes find better terms through local institutions familiar with regional economic conditions and employment patterns.

ConsumerAffairs’ evaluation of top car loan refinancing companies emphasizes the importance of considering both national brands and regional specialists when building your comparison set.

Special Refinancing Situations and Solutions

Not all refinancing scenarios follow standard patterns. Understanding how lenders approach unique situations helps you identify appropriate options for your specific circumstances.

Refinancing with Credit Challenges

Past credit issues don't permanently disqualify you from beneficial refinancing. Lenders specializing in credit-challenged borrowers evaluate additional factors beyond credit scores:

Income stability often outweighs credit history for specialized lenders. Demonstrating consistent employment and sufficient income to cover your proposed payment comfortably can offset lower credit scores.

Payment history on your current auto loan provides powerful evidence of your commitment. Twelve consecutive on-time payments demonstrates reliability more convincingly than abstract credit scores.

Down payment or equity contribution reduces lender risk and may unlock better terms. Contributing even $500-$1,000 toward principal reduction at refinancing can improve your approval odds and available rates.

Cash-Out Refinancing for Additional Funds

Cash-out refinancing allows you to borrow against your vehicle's equity while simultaneously refinancing your existing loan. This approach suits borrowers needing funds for home improvements, medical expenses, education costs, or debt consolidation.

Equity requirements typically demand at least 20-25% equity in your vehicle before cash-out options become available. If your vehicle is worth $20,000 and you owe $12,000, you have $8,000 in equity (40%), making you a strong candidate for cash-out refinancing.

Rate implications mean cash-out refinancing often carries slightly higher APRs than standard refinancing due to increased loan-to-value ratios. However, these rates still typically beat personal loans or credit cards for accessing needed funds.

Managing Your Refinanced Auto Loan Successfully

Securing the best car loan refinance represents just the beginning. Managing your new loan strategically ensures you realize intended benefits and potentially accelerate debt elimination.

Setting Up Automatic Payments

Autopay enrollment typically reduces your APR by 0.25-0.50%, translating to hundreds in savings over your loan term. Additionally, automatic payments eliminate the risk of missed payments that could damage your credit score and potentially incur late fees.

Schedule automatic payments for 2-3 days after your paycheck deposits to ensure sufficient funds while maintaining the payment schedule.

Making Strategic Extra Payments

Even small additional principal payments dramatically reduce total interest costs and accelerate loan payoff. An extra $50 monthly on a $15,000 loan at 7% APR saves approximately $800 in interest and shortens your term by nearly a year.

Focus extra payments during the early loan period when interest comprises a larger portion of each payment. This timing maximizes the impact of your additional contributions.

Monitoring for Future Refinancing Opportunities

The best car loan refinance today might not remain optimal throughout your entire loan term. Annual rate reviews help you identify new opportunities as market conditions change or your credit profile improves further.

Set a calendar reminder each year to check current refinancing rates against your existing loan. If you discover rates have dropped another percentage point or your credit score has climbed significantly, you might benefit from refinancing your refinanced loan.

Best Reward Federal Credit Union’s vehicle loan refinance options demonstrate how credit unions often offer particularly competitive rates for members with established relationships, making them worth considering during future refinancing evaluations.

Technology and Digital Refinancing Platforms

The refinancing landscape in 2026 reflects significant technological advancement, streamlining processes that previously required extensive paperwork and multiple branch visits.

Online Application Benefits and Considerations

Digital-first lenders complete the entire refinancing process electronically, from initial application through funding. This approach offers convenience and speed, often delivering approvals within hours and funding within 24-48 hours.

Hybrid models combine online application convenience with personal service options for borrowers preferring human interaction during complex decisions. These platforms allow you to start applications digitally while maintaining access to loan specialists for questions and guidance.

Document Upload and Verification Systems

Modern refinancing platforms use sophisticated document verification that accepts smartphone photos of required paperwork. Optical character recognition technology extracts information from uploaded documents, eliminating manual data entry and reducing errors.

Some lenders now connect directly to payroll systems and banking institutions for instant income and asset verification, further accelerating approval timelines for borrowers comfortable sharing secure access.

Refinancing your auto loan presents a powerful opportunity to reduce monthly expenses, lower total interest costs, and improve your overall financial flexibility. By understanding qualification requirements, comparing multiple lenders, and avoiding common pitfalls, you position yourself to secure terms that align with your current financial situation and future goals. Whether you're looking to reduce your monthly payment, shorten your loan term, or access vehicle equity for other needs, Standard Financial offers flexible refinancing options tailored to borrowers across the credit spectrum, with personalized service through our Louisiana, Mississippi, Tennessee, and Georgia branch locations ready to help you find your best car loan refinance solution.

No comment yet, add your voice below!