Managing personal finances requires careful planning and predictable costs. One of the most valuable tools for maintaining financial stability is understanding how fixed monthly payments work and why they matter for borrowers across various lending situations. Whether you're financing a home improvement project, consolidating medical debt, or pursuing educational opportunities, knowing what to expect each month eliminates uncertainty and helps you build a sustainable budget that accommodates your financial goals.

Understanding the Structure of Fixed Monthly Payments

Fixed monthly payments represent a consistent amount you pay toward a loan each month until the debt is fully satisfied. Unlike variable payment structures where the amount can fluctuate based on interest rate changes or other factors, these payments remain constant throughout the loan term. This predictability offers significant advantages for household budgeting and long-term financial planning.

The calculation behind these payments involves several key components: the principal amount borrowed, the annual percentage rate (APR), and the loan term. Lenders use a specific formula to determine the exact monthly obligation that will fully amortize the loan over the agreed period. Understanding how these calculations work helps borrowers make informed decisions about loan amounts and terms that fit their budget constraints.

Breaking Down Your Payment Components

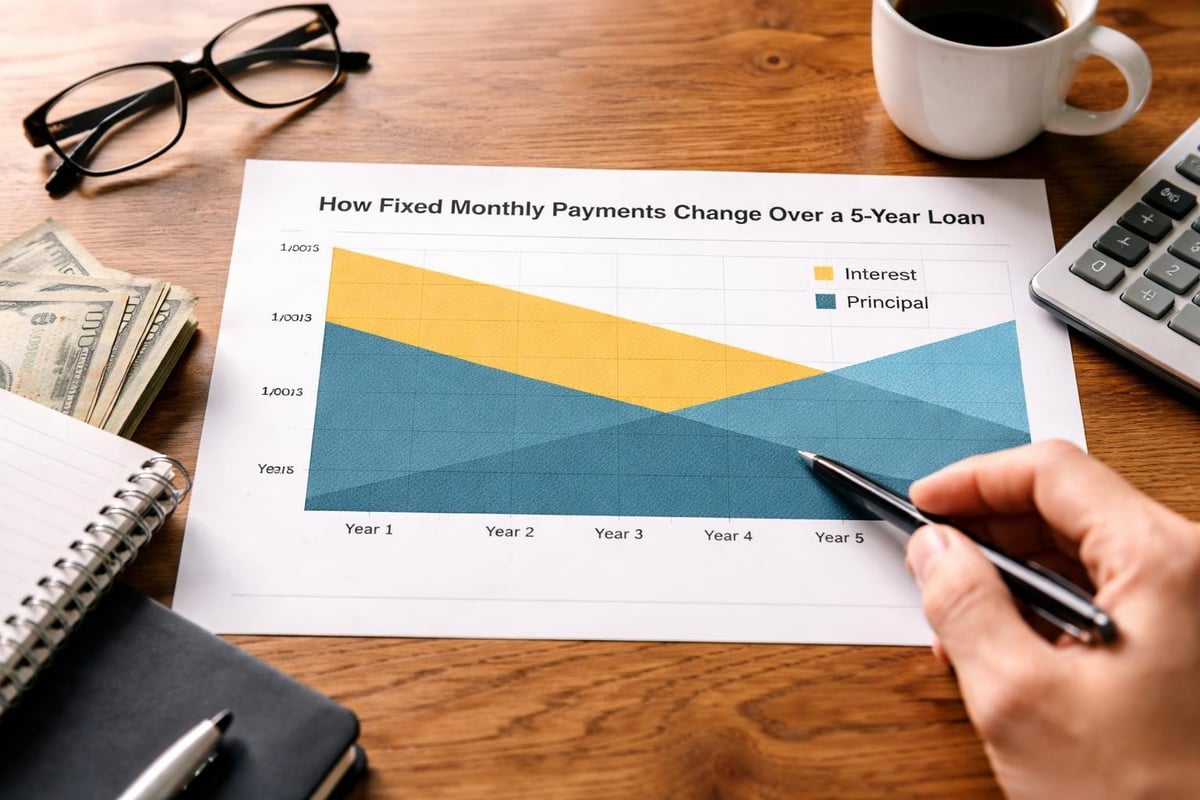

Each fixed monthly payment typically consists of two primary elements: principal reduction and interest charges. During the early stages of repayment, a larger portion goes toward interest, while the principal portion gradually increases over time. This amortization schedule ensures that by the final payment, the entire balance is satisfied.

Consider a personal loan of $10,000 with a 7% annual interest rate over five years:

| Payment Number | Monthly Payment | Principal | Interest | Remaining Balance |

|---|---|---|---|---|

| 1 | $198.01 | $139.68 | $58.33 | $9,860.32 |

| 12 | $198.01 | $148.03 | $49.98 | $8,341.26 |

| 24 | $198.01 | $157.10 | $40.91 | $6,499.08 |

| 36 | $198.01 | $166.66 | $31.35 | $4,505.42 |

| 60 | $198.01 | $197.86 | $0.15 | $0.00 |

This example demonstrates how consistent payments systematically reduce debt while maintaining budget predictability. The borrower knows exactly what they'll owe each month, making it easier to allocate income toward other expenses and savings goals.

The Advantages of Payment Predictability

Financial experts consistently emphasize the importance of predictability in debt repayment, particularly when managing multiple financial obligations. Fixed monthly payments provide a foundation for effective budgeting because they eliminate the guesswork from monthly expense planning.

When you know your payment amount won't change, you can:

- Build emergency savings with greater confidence

- Plan for major purchases without worrying about payment fluctuations

- Avoid budget shortfalls caused by unexpected payment increases

- Create accurate long-term financial projections

- Reduce financial stress and anxiety

Budget stability becomes particularly valuable during economic uncertainty. While other costs like groceries, utilities, and healthcare may rise unexpectedly, your loan payment remains constant. This reliability serves as an anchor in your financial plan, providing certainty amid changing economic conditions.

Protection Against Interest Rate Volatility

One of the most significant benefits of fixed monthly payments is protection from interest rate fluctuations. When market rates increase, borrowers with variable-rate loans face higher monthly obligations. Those with fixed-rate agreements maintain their original payment amount regardless of broader economic trends.

Between 2022 and 2025, many consumers experienced dramatic interest rate increases that affected variable-rate credit cards, home equity lines of credit, and adjustable-rate loans. Borrowers who secured fixed rates before these increases benefited from substantial savings and payment consistency.

Applications Across Different Loan Types

Fixed monthly payments appear in numerous consumer lending products, each serving specific financial needs. Understanding how they apply to different situations helps borrowers choose the right financing option for their circumstances.

Personal Loans for Home Improvements

Home renovation projects often require significant upfront capital. A personal loan with fixed monthly payments allows homeowners to spread costs over several years while knowing exactly what they'll pay each month. Whether installing new HVAC systems, replacing roofs, or remodeling kitchens, this payment structure helps homeowners budget for improvements without draining savings accounts.

The average home improvement loan ranges from $5,000 to $50,000, with terms typically spanning two to seven years. Fixed payments ensure that seasonal income variations or unexpected expenses don't derail your renovation financing.

Medical Expense Financing

Healthcare costs can arrive unexpectedly and create immediate financial pressure. Medical loans with fixed monthly payments transform large bills into manageable obligations spread over time. This approach proves especially valuable for procedures not fully covered by insurance, dental work, or ongoing treatment plans.

Key advantages for medical financing include:

- Immediate access to necessary treatments without delay

- Predictable repayment that doesn't interfere with recovery

- No impact from rising healthcare inflation on payment amounts

- Ability to maintain health insurance coverage while managing procedure costs

Educational Investment Loans

Investing in education, whether for degree programs, certification courses, or professional development, often requires financing. Fixed monthly payments for educational loans provide students and working professionals with clear repayment expectations that align with career advancement timelines.

Unlike some federal student loan programs with income-driven repayment plans, private educational loans typically feature consistent monthly obligations. This structure works well for borrowers with stable employment who value predictable budgeting over payment flexibility.

Qualification Considerations and Credit Factors

Lenders evaluate multiple factors when determining loan approval and fixed monthly payment amounts. Understanding these criteria helps prospective borrowers prepare applications and improve approval chances.

Income Verification and Debt-to-Income Ratios

Your ability to afford fixed monthly payments depends largely on your income relative to existing debt obligations. Lenders calculate debt-to-income (DTI) ratios by comparing monthly liabilities to gross monthly income. Most consumer lenders prefer DTI ratios below 43%, though some programs accommodate higher ratios with compensating factors.

| DTI Ratio Range | Lending Perspective | Typical Outcome |

|---|---|---|

| Below 36% | Excellent | Best rates and terms available |

| 36% to 43% | Good | Competitive approval with standard terms |

| 43% to 50% | Moderate | Possible approval with higher rates |

| Above 50% | Challenging | May require additional documentation or collateral |

Lowering your DTI ratio before applying improves your chances of securing favorable fixed monthly payments. Strategies include paying down existing debts, increasing income through additional work, or applying with a co-borrower who has strong financial credentials.

Credit History and Past Issues

Standard Financial and similar consumer lenders recognize that past credit challenges don't necessarily predict future payment behavior. Many borrowers have experienced financial setbacks due to medical emergencies, job loss, divorce, or other circumstances beyond their control. Progressive lending programs evaluate the complete financial picture rather than focusing exclusively on credit scores.

Factors that strengthen applications despite credit issues:

- Demonstrated income stability over recent months

- Evidence of improved financial management

- Explanation letters addressing past credit problems

- Recent positive payment history on current obligations

- Willingness to consider secured loan options

Even borrowers with previous credit difficulties can often qualify for personal loans with fixed monthly payments that help rebuild financial standing while addressing current needs.

Comparing Fixed Versus Variable Payment Structures

The choice between fixed and variable payment plans significantly impacts long-term financial outcomes. While variable-rate products sometimes offer lower initial rates, they carry inherent uncertainty that many borrowers find problematic.

Interest Rate Risk Assessment

Variable payment structures tie your monthly obligation to an underlying interest rate index. When these benchmark rates increase, your payment rises accordingly. This arrangement creates budget uncertainty and can lead to payment shock when rates jump significantly within short periods.

Fixed-rate products eliminate this risk entirely. The interest rate established at loan origination remains constant, ensuring your fixed monthly payments never change due to market conditions. This stability proves particularly valuable during periods of economic volatility or rising rate environments.

Long-Term Cost Analysis

Evaluating total loan costs requires looking beyond the initial interest rate. A variable-rate loan might start with a rate 0.5% to 1% below comparable fixed-rate products, creating the appearance of savings. However, if rates increase even modestly over the loan term, the total interest paid can exceed what a fixed-rate borrower would pay.

Consider a five-year $15,000 loan scenario:

- Fixed Rate at 8%: Monthly payment of $304.15, total interest of $3,249

- Variable Rate starting at 7%: Initial payment of $297.02, but if rates increase to 9% by year three, total interest could reach $3,650 or more

The apparent savings of $7 per month disappears quickly when rates rise, and the variable-rate borrower faces increased payment amounts precisely when least affordable.

Strategies for Managing Fixed Monthly Payments Successfully

Securing a loan with fixed monthly payments represents just the beginning of successful debt management. Implementing effective strategies ensures timely repayment and maximizes the benefits of payment predictability.

Automated Payment Systems

Setting up automatic payments directly from your checking account eliminates the risk of missed deadlines and potential late fees. Most lenders offer small interest rate reductions (typically 0.25%) for borrowers who enroll in autopay programs. This discount, combined with the convenience and payment security, makes automation highly beneficial.

Schedule automatic payments for dates that align with your income deposits. If you receive paychecks on the 1st and 15th, scheduling loan payments for the 3rd or 17th ensures funds are available and reduces overdraft risk.

Building Payment Buffers

While fixed monthly payments provide predictability, unexpected financial disruptions can still occur. Creating a dedicated buffer fund equal to three to six months of loan payments provides security against job changes, medical emergencies, or other income interruptions.

Steps to build a payment buffer:

- Calculate total monthly debt obligations including the new fixed payment

- Multiply by three to determine minimum buffer goal

- Set aside a small amount weekly or monthly toward this fund

- Keep buffer funds in a separate savings account to avoid casual spending

- Replenish the buffer if you need to use it

This safety net ensures you can maintain positive payment history even during challenging periods, protecting your credit standing and avoiding default consequences.

Refinancing Opportunities

As your credit profile improves or market conditions change, refinancing existing loans might provide opportunities to reduce fixed monthly payments or shorten loan terms. Evaluate refinancing when interest rates drop significantly below your current rate or when your credit score has improved substantially since origination.

Calculate whether refinancing savings justify any associated fees. A simple break-even analysis comparing monthly savings against closing costs reveals whether refinancing makes financial sense for your situation.

Special Considerations for Different Life Stages

Fixed monthly payments serve different purposes depending on where you are in your financial journey. Tailoring loan selection to your current life stage optimizes the benefits of payment predictability.

Early Career Borrowers

Younger borrowers often face competing financial priorities: building emergency savings, managing student debt, and establishing credit history. Fixed monthly payments on smaller personal loans help accomplish multiple goals simultaneously.

Taking a modest loan for specific purposes (professional certification, reliable transportation, essential home furnishings) and maintaining perfect payment history establishes positive credit patterns. This foundation supports future borrowing for larger purchases like homes or business ventures.

Mid-Career Financial Consolidation

Professionals in their peak earning years frequently use fixed monthly payments to consolidate higher-interest debts into single, manageable obligations. This strategy simplifies budgeting by replacing multiple variable payments with one predictable monthly amount.

Debt consolidation through personal loans works best when:

- The new fixed rate is lower than the weighted average of current debts

- You commit to avoiding new high-interest debt after consolidation

- The monthly payment comfortably fits within your budget

- The loan term balances affordability with total interest costs

Pre-Retirement Planning

As retirement approaches, reducing debt obligations and ensuring payment predictability become increasingly important. Fixed monthly payments that will be satisfied before retirement help align debt management with retirement income planning.

Many pre-retirees prioritize shorter loan terms (three to five years) that eliminate obligations while still working. This approach ensures retirement income covers lifestyle needs rather than debt service.

Regional Lending Considerations in the Southeast

Borrowers across Louisiana, Mississippi, Tennessee, and Georgia face unique economic conditions that influence lending decisions and the value of fixed monthly payments. Understanding regional factors helps optimize loan selection and terms.

Economic diversity across these states creates varied employment landscapes. Louisiana's energy and tourism sectors, Mississippi's manufacturing and agriculture, Tennessee's healthcare and automotive industries, and Georgia's technology and logistics hubs all present different income stability profiles. Fixed monthly payments provide certainty regardless of industry-specific economic cycles.

Regional cost-of-living differences also impact how fixed monthly payments fit into household budgets. A $300 monthly payment represents a different budget percentage for borrowers in rural Mississippi compared to metropolitan Atlanta. Working with local lenders who understand regional economics ensures loan structures align with realistic budgeting scenarios.

The Role of Transparency in Fixed Payment Lending

Consumer lending regulations emphasize transparency in loan disclosures and payment calculations, ensuring borrowers understand their obligations before committing. This regulatory framework protects consumers while promoting informed decision-making.

Truth in Lending Act (TILA) requirements mandate clear disclosure of:

- Total amount financed

- Annual percentage rate (APR)

- Finance charges over the loan term

- Payment schedule with due dates

- Total of all payments

Reviewing these disclosures carefully before signing loan documents ensures you understand exactly what you're committing to with fixed monthly payments. Don't hesitate to ask lenders to explain any terms or calculations that seem unclear.

Making Informed Borrowing Decisions

Choosing the right loan with appropriate fixed monthly payments requires evaluating your complete financial picture and future goals. This comprehensive assessment ensures borrowing supports your broader financial strategy rather than creating unnecessary burden.

Start by calculating your actual available monthly income after essential expenses like housing, transportation, food, and utilities. The amount remaining represents your realistic capacity for debt service. Financial advisors typically recommend limiting total debt payments (excluding mortgage) to 15% to 20% of gross income.

Next, consider the loan's purpose and whether it represents an investment in your future (education, home improvements that increase property value) or addresses immediate needs (medical expenses, debt consolidation). Understanding the purpose helps evaluate appropriate loan terms and payment amounts.

Finally, compare offers from multiple lenders to ensure you're securing competitive terms. While rate shopping might feel time-consuming, even small interest rate differences create substantial savings over multi-year loan terms.

Fixed monthly payments provide the financial predictability and stability that help borrowers manage debt successfully while maintaining healthy household budgets. Understanding how these payments work, their advantages across different lending situations, and strategies for successful management empowers you to make informed borrowing decisions that support your financial goals. Whether you're planning home improvements, managing medical expenses, investing in education, or consolidating existing debts, Standard Financial offers flexible personal loan solutions with transparent terms and fixed monthly payments designed to fit your unique circumstances, even if you've faced credit challenges in the past.

No comment yet, add your voice below!