The landscape of personal financing has undergone a dramatic transformation over the past decade, with digital platforms fundamentally changing how Americans access credit. Securing a consumer loan online has become the preferred method for millions of borrowers seeking quick, convenient financing solutions. Whether you're planning a home renovation, covering unexpected medical bills, or consolidating existing debt, understanding the digital lending environment empowers you to make informed financial decisions. This comprehensive guide explores everything you need to know about obtaining financing through online channels, from application processes to approval criteria and best practices for selecting trustworthy lenders.

Understanding the Consumer Loan Online Marketplace

The digital lending sector has expanded rapidly, offering borrowers unprecedented access to credit products without visiting physical branches. A consumer loan online typically refers to unsecured personal loans obtained entirely through internet-based platforms, from application submission to fund disbursement.

Traditional financial institutions, credit unions, and specialized online lenders now compete in this space, creating a diverse marketplace with varying terms, rates, and qualification requirements. This competition generally benefits consumers by driving down interest rates and improving service quality across the industry.

Key Advantages of Digital Lending Platforms

Applying for financing through online channels offers several compelling benefits:

- Convenience: Complete applications from anywhere, at any time, without scheduling appointments or taking time off work

- Speed: Receive preliminary decisions within minutes and funding as quickly as the next business day

- Transparency: Compare multiple offers simultaneously to identify the most favorable terms

- Streamlined documentation: Upload required documents digitally rather than making multiple branch visits

- Broader access: Reach lenders nationwide rather than limiting options to local institutions

The FDIC provides comprehensive oversight of consumer lending practices, ensuring that digital platforms maintain appropriate standards for fairness and transparency. Understanding these regulatory protections helps borrowers recognize legitimate operations versus predatory lending schemes.

Eligibility Requirements and Application Process

Successfully obtaining a consumer loan online requires meeting specific criteria that lenders use to assess creditworthiness. While requirements vary among institutions, understanding common standards helps you prepare effective applications.

Standard Qualification Criteria

Most digital lenders evaluate applicants based on these factors:

| Criterion | Typical Requirement | Purpose |

|---|---|---|

| Credit Score | 580-660+ (varies by lender) | Assesses payment history and credit management |

| Income Verification | Steady employment or income source | Confirms ability to repay |

| Debt-to-Income Ratio | Generally below 43% | Evaluates existing financial obligations |

| Residency | U.S. citizenship or permanent residency | Legal and compliance requirements |

| Age | Minimum 18 years old | Legal capacity to enter contracts |

Many reputable lenders, including those with physical presence in states like Louisiana, Mississippi, Tennessee, and Georgia, extend financing to borrowers with past credit challenges. These institutions recognize that credit scores don't tell the complete story of financial responsibility.

Step-by-Step Application Process

Completing a consumer loan online application typically involves these stages:

- Pre-qualification: Submit basic information for a soft credit check that doesn't impact your score

- Formal application: Provide detailed personal, employment, and financial information

- Documentation upload: Submit pay stubs, bank statements, and identification documents

- Verification: Lender confirms information and may request additional clarification

- Approval decision: Receive loan terms, including amount, rate, and repayment schedule

- Agreement signing: Review and electronically sign loan documents

- Fund disbursement: Receive money via direct deposit to your bank account

The entire process can take anywhere from a few hours to several days, depending on the lender's procedures and how quickly you provide required documentation.

Evaluating Interest Rates and Loan Terms

Understanding the cost structure of a consumer loan online enables you to compare offers effectively and select the most economical option for your circumstances. Interest rates and terms vary significantly based on creditworthiness, loan amount, and repayment period.

Factors Influencing Your Interest Rate

Lenders consider multiple variables when determining the annual percentage rate (APR) they'll offer:

- Credit history: Higher scores typically qualify for lower rates

- Loan amount: Larger loans may carry different pricing than smaller amounts

- Repayment term: Shorter terms often feature lower rates but higher monthly payments

- Income stability: Consistent employment history can improve rate offers

- Debt obligations: Lower existing debt loads may qualify for better pricing

In 2026, consumer loan online interest rates generally range from approximately 6% for borrowers with excellent credit to 36% for those with significant credit challenges. The Consumer Financial Protection Bureau accepts complaints related to online marketplace lenders, providing oversight that helps maintain fair lending practices.

Comparing Total Loan Costs

Looking beyond the monthly payment reveals the true cost of borrowing:

| Loan Amount | APR | Term | Monthly Payment | Total Interest Paid |

|---|---|---|---|---|

| $10,000 | 12% | 3 years | $332 | $1,952 |

| $10,000 | 12% | 5 years | $222 | $3,346 |

| $10,000 | 18% | 3 years | $361 | $2,996 |

| $10,000 | 18% | 5 years | $254 | $5,240 |

This comparison demonstrates how both interest rates and loan duration significantly impact overall costs. Shorter terms mean less total interest despite higher monthly obligations.

Identifying Reputable Online Lenders

The proliferation of digital lending platforms has unfortunately attracted some illegitimate operators alongside reputable institutions. Protecting yourself requires knowing how to distinguish trustworthy lenders from potential scams.

Red Flags to Avoid

Watch for these warning signs that may indicate predatory or fraudulent operations:

- Guaranteed approval regardless of credit history or income

- Requests for upfront fees before loan approval

- Pressure tactics demanding immediate decisions

- Lack of physical address or state licensing information

- Unsolicited loan offers via email, text, or phone calls

- Unwillingness to provide terms in writing before signing

Experian offers guidance on evaluating the trustworthiness of online personal loan lenders, highlighting specific characteristics that separate legitimate businesses from questionable operators.

Verifying Lender Credentials

Before submitting a consumer loan online application, conduct these verification steps:

- Check state licensing: Confirm the lender is registered to operate in your state through your state banking department

- Review online presence: Examine the company website for complete contact information and professional presentation

- Read customer reviews: Look for patterns in feedback across multiple review platforms

- Verify Better Business Bureau status: Check ratings and complaint history

- Confirm secure technology: Ensure websites use HTTPS encryption and display security certificates

Established lenders with physical branch networks in multiple states typically offer additional credibility and accountability compared to purely digital operations with no physical presence.

Common Uses for Consumer Loans Online

Digital personal loans provide flexible funding for numerous purposes, giving borrowers autonomy to address their most pressing financial needs. Understanding typical use cases helps you evaluate whether this financing option aligns with your objectives.

Popular Loan Purposes

Borrowers frequently seek consumer loans online for these situations:

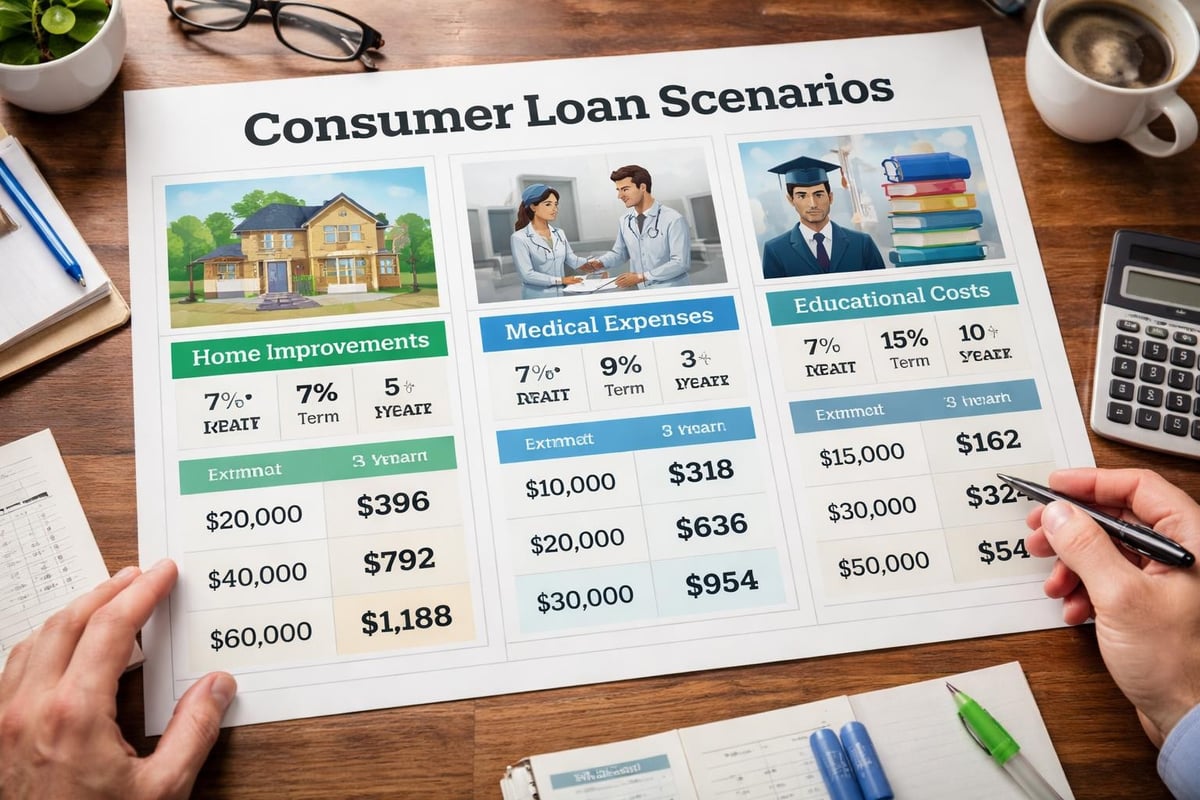

Home Improvements and Repairs

Financing renovations, roof replacements, HVAC systems, or other property upgrades that increase home value or address essential maintenance needs.

Medical Expenses

Covering procedures, treatments, or emergency care not fully covered by insurance, enabling access to necessary healthcare without depleting savings.

Debt Consolidation

Combining multiple high-interest credit card balances or other debts into a single loan with potentially lower rates and one manageable monthly payment.

Education and Training

Funding continuing education, professional certifications, or skills training that can enhance career prospects and earning potential.

Major Purchases

Acquiring necessary appliances, furniture, or electronics when paying cash isn't feasible and installment plans offer better terms than credit cards.

Emergency Situations

Addressing unexpected expenses like vehicle repairs, emergency travel, or temporary income gaps that require immediate funding.

The Consumer Financial Protection Bureau provides educational resources covering various aspects of credit and lending, helping borrowers make informed decisions about when personal loans represent the most appropriate financing solution.

Managing Your Loan Responsibly

Successfully obtaining a consumer loan online represents just the beginning of your borrowing relationship. Responsible management ensures you benefit from the financing while protecting and potentially improving your credit profile.

Best Practices for Loan Management

Implement these strategies to maximize the benefits of your personal loan:

- Set up automatic payments: Eliminate the risk of missed payments by scheduling automatic withdrawals on or before due dates

- Pay more than the minimum: Additional principal payments reduce total interest costs and shorten your repayment timeline

- Maintain communication: Contact your lender immediately if financial difficulties arise rather than defaulting on payments

- Monitor your credit: Track how consistent payments improve your credit score over time

- Avoid new debt: Resist accumulating additional obligations while repaying your existing loan

- Keep documentation: Retain all loan agreements, payment confirmations, and correspondence for your records

Building a positive payment history demonstrates creditworthiness that can qualify you for better terms on future financing needs.

Understanding Your Rights and Protections

Federal and state regulations provide important safeguards for borrowers securing consumer loans online. The CFPB offers compliance resources covering various lending topics, including consumer rights and lender obligations.

Key protections include:

| Protection | Description |

|---|---|

| Truth in Lending Act | Requires clear disclosure of loan terms, APR, and total costs |

| Fair Credit Reporting Act | Ensures accurate credit reporting and dispute resolution processes |

| Equal Credit Opportunity Act | Prohibits discrimination based on protected characteristics |

| Electronic Signatures in Global and National Commerce Act | Validates electronic agreements and disclosures |

Familiarizing yourself with these protections enables you to recognize violations and seek appropriate remedies if problems arise with your lender.

Comparing Online and Traditional Lending Options

While digital platforms dominate modern consumer lending, traditional branch-based institutions continue serving important roles in the financial ecosystem. Understanding the distinctions helps you select the approach that best matches your preferences and circumstances.

Online Lending Advantages

Digital-first lenders typically excel in these areas:

Speed and efficiency: Automated underwriting systems process applications faster than manual review processes, often providing decisions within minutes rather than days.

Lower overhead costs: Without extensive branch networks, online lenders may pass savings to customers through competitive interest rates and reduced fees.

24/7 accessibility: Submit applications, check account status, and manage your loan anytime without being constrained by business hours.

Wider market reach: Access lenders nationwide rather than limiting choices to institutions with local presence.

Traditional Lending Benefits

Branch-based institutions offer distinct advantages:

Personal relationships: Face-to-face interactions with loan officers who understand your unique financial situation and can offer customized guidance.

Local decision-making: Branch managers may have flexibility to consider factors beyond automated criteria, potentially approving borderline applications.

Comprehensive services: Access to full-service banking relationships including checking accounts, savings products, and financial planning assistance.

Community presence: Established institutions with physical locations provide tangible accountability and local economic investment.

Many modern lenders combine both approaches, maintaining branch networks in states like Louisiana, Mississippi, Tennessee, and Georgia while offering robust online application and management tools. This hybrid model delivers convenience without sacrificing personal service.

Refinancing and Future Borrowing Opportunities

Successfully managing your initial consumer loan online creates opportunities for improved financial flexibility through refinancing or additional borrowing at favorable terms.

When Refinancing Makes Sense

Consider refinancing your existing loan under these circumstances:

- Credit score improvement: If your score has increased significantly since your original loan, you may qualify for substantially lower rates

- Interest rate decreases: Market rate changes might enable you to reduce your APR even without credit changes

- Payment affordability: Extending your term can lower monthly obligations if budget pressures have increased

- Loan consolidation: Combining multiple loans simplifies finances and may reduce overall interest costs

Building Long-Term Lender Relationships

Establishing positive history with a consumer loan online provider creates valuable advantages:

- Streamlined future applications: Previous customers often receive expedited processing for additional loans

- Preferential pricing: Demonstrated reliability may qualify you for rate discounts on subsequent borrowing

- Higher approval amounts: Proven repayment capability can increase the funding you're eligible to receive

- Flexible terms: Existing relationships sometimes provide access to customized repayment schedules

The American Bankers Association offers comprehensive training on consumer lending principles, reflecting the industry's commitment to professional standards and customer service excellence.

Technology and Security Considerations

Protecting your personal and financial information remains paramount when conducting transactions through digital channels. Understanding security measures helps you engage confidently with online lending platforms.

Essential Security Features

Reputable lenders implement multiple protective layers:

Encryption protocols: Industry-standard SSL/TLS encryption secures data transmission between your device and lender servers, preventing interception by unauthorized parties.

Multi-factor authentication: Additional verification steps beyond passwords, such as one-time codes sent to your phone, prevent unauthorized account access.

Secure document upload: Encrypted portals protect sensitive documents like tax returns, bank statements, and identification when submitting application materials.

Privacy policies: Clear statements explaining how your information is used, stored, and protected, including restrictions on sharing with third parties.

Protecting Yourself Online

Take these precautions when applying for a consumer loan online:

- Use secure, private internet connections rather than public WiFi networks when submitting sensitive information

- Create strong, unique passwords for each financial account and change them periodically

- Monitor your credit reports regularly for unauthorized inquiries or accounts

- Review bank statements for any unexpected transactions related to loan applications

- Save confirmation emails and take screenshots of important application steps

- Report suspicious communications claiming to be from your lender directly to the institution

The CFPB provides guidance on navigating financial regulations and understanding your rights, helping consumers protect themselves in the digital lending environment.

Navigating the consumer loan online marketplace successfully requires understanding application processes, comparing terms carefully, and selecting reputable lenders who prioritize transparency and customer service. Armed with this knowledge, you can confidently pursue financing that aligns with your goals and budget. Whether you need funds for home improvements, medical expenses, education, or other personal needs, Standard Financial offers flexible financing solutions with personalized service backed by decades of experience serving communities throughout Louisiana, Mississippi, Tennessee, and Georgia, including options for borrowers with past credit challenges who deserve a second chance at financial success.

No comment yet, add your voice below!