Dealing with collections can feel overwhelming, especially when you're uncertain how resolving these debts will affect your financial future. Many consumers wonder whether taking action on collection accounts will actually help their credit scores or if the damage is already done. The answer isn't straightforward because multiple factors influence how paying off collections impacts your credit, including which credit scoring model lenders use, the age of the debt, and whether you can negotiate specific terms. Understanding these nuances helps you make informed decisions about managing collection accounts and rebuilding your financial standing.

Understanding How Collection Accounts Affect Your Credit

Collection accounts represent debts that creditors have given up trying to collect themselves, instead transferring them to third-party collection agencies. These accounts typically appear on your credit report after an account becomes seriously delinquent, usually 120 to 180 days past due.

When a collection account hits your credit report, it signals to lenders that you've failed to meet your payment obligations. This negative mark can significantly lower your credit score because payment history accounts for 35% of your FICO score calculation. The impact isn't just limited to the collection itself. The original delinquency that led to collections also damages your credit.

The Timeline of Collection Reporting

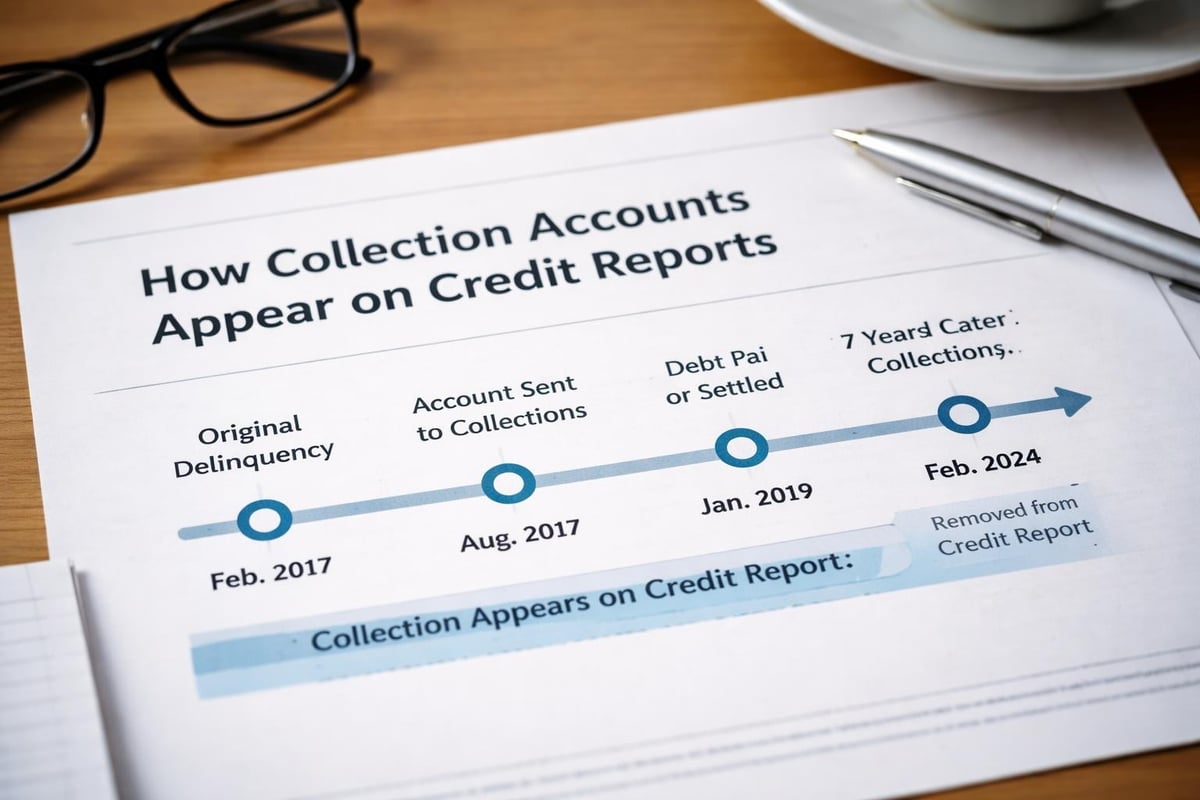

Collections can remain on your credit report for up to seven years from the date of the original delinquency. This timeline starts with the first missed payment that led to the account becoming delinquent, not when the collection agency took over the debt.

Key timeline factors include:

- Original delinquency date determines when the seven-year clock starts

- Collection agency transfers don't reset this timeline

- Partial payments on collections don't extend reporting periods

- The debt continues reporting even after you pay it off

Does Paying Off Collections Improve Credit Score Directly?

The question of does paying off collections improve credit score depends heavily on which credit scoring model evaluates your credit file. Different models treat paid collections differently, creating confusion for consumers trying to improve their financial standing.

Traditional FICO scores (versions 8 and earlier) treat paid and unpaid collections similarly. Under these older models, paying off a collection doesn't automatically boost your score because the negative mark remains on your report regardless of payment status. The collection account still indicates that you previously failed to pay as agreed.

However, newer scoring models show more leniency toward paid collections. FICO 9 and VantageScore 3.0 and 4.0 disregard paid collection accounts, meaning they won't negatively impact your score once paid. This represents a significant shift in how credit scoring treats resolved debts.

Credit Scoring Model Comparison

| Scoring Model | Treatment of Paid Collections | Market Usage |

|---|---|---|

| FICO 8 | Counts against score | Very common |

| FICO 9 | Ignores paid collections | Growing adoption |

| VantageScore 3.0/4.0 | Ignores paid collections | Increasing use |

| FICO 10 | Ignores paid medical collections | Limited adoption |

The challenge for consumers is that you typically don't know which scoring model a particular lender uses. Many lenders still rely on FICO 8, which treats paid and unpaid collections the same way.

Indirect Benefits of Paying Off Collections

Even when paying collections doesn't immediately improve your credit score under certain models, resolving these debts offers several important advantages that support your financial health and future creditworthiness.

Lenders reviewing your credit application manually often view paid collections more favorably than unpaid ones. This human element matters when applying for mortgages, auto loans, or personal loans. A loan officer may approve your application despite past collections if they see you've resolved those debts, demonstrating financial responsibility and willingness to make things right.

Additional benefits include:

- Stopping collection calls and letters

- Eliminating the risk of lawsuits over the debt

- Preventing wage garnishment in states where allowed

- Reducing your overall debt-to-income ratio

- Creating a foundation for credit rebuilding

Paying off collections also prevents the debt from growing. Collection agencies often add fees and interest, increasing the amount you owe over time. Resolving the debt stops this accumulation and provides peace of mind.

When Paying Collections Makes the Most Sense

You should prioritize paying collections when you're actively applying for credit, especially for significant purchases like homes or vehicles. Many mortgage lenders require you to resolve all outstanding collections before approval, regardless of how payment affects your credit score.

Recent collections typically have more impact than older ones. If a collection is from the past year or two, paying it off can prevent additional damage and show lenders you're addressing your financial obligations. Older debts nearing the seven-year reporting limit may not warrant payment from a credit score perspective, though ethical and legal obligations still exist.

Strategic Approaches to Paying Collections

How you handle paying off collections can significantly impact the outcome. Strategic negotiation and payment methods can sometimes result in better credit report treatment than simply paying the full amount immediately.

Pay-for-Delete Agreements

One powerful strategy involves negotiating a "pay-for-delete" agreement with the collection agency. Under this arrangement, you agree to pay the debt in exchange for the agency removing the collection from your credit report entirely. While not all collection agencies agree to this practice, many will consider it, especially for smaller debts.

- Contact the collection agency and request a pay-for-delete arrangement

- Get any agreement in writing before making payment

- Specify that the collection account will be removed from all three credit bureaus

- Keep all documentation of the agreement and payment

- Verify removal from your credit reports within 30-45 days

Pay-for-delete offers the best possible outcome because the negative mark disappears completely. This immediately improves your credit score under all scoring models since there's no collection to report.

Settlement Negotiations

If the collection agency won't agree to pay-for-delete, you can still negotiate the amount you pay. Many agencies will accept less than the full balance, sometimes settling for 40-60% of the original debt. While settled collections still appear on your credit report, resolving them for less than you owe preserves your financial resources.

When you settle, the account will be marked "settled" or "paid for less than the full balance" on your credit report. This status is better than unpaid but not as beneficial as paid in full under manual underwriting reviews.

Validation Requests

Before paying any collection, request debt validation. Collection agencies must prove you owe the debt and that they have the legal right to collect it. Send a written validation request within 30 days of the agency's first contact.

If the agency cannot validate the debt with proper documentation, they must stop collection activities and remove the account from your credit report. This approach works particularly well for older debts where documentation may be incomplete or lost.

Medical Collections Receive Special Treatment

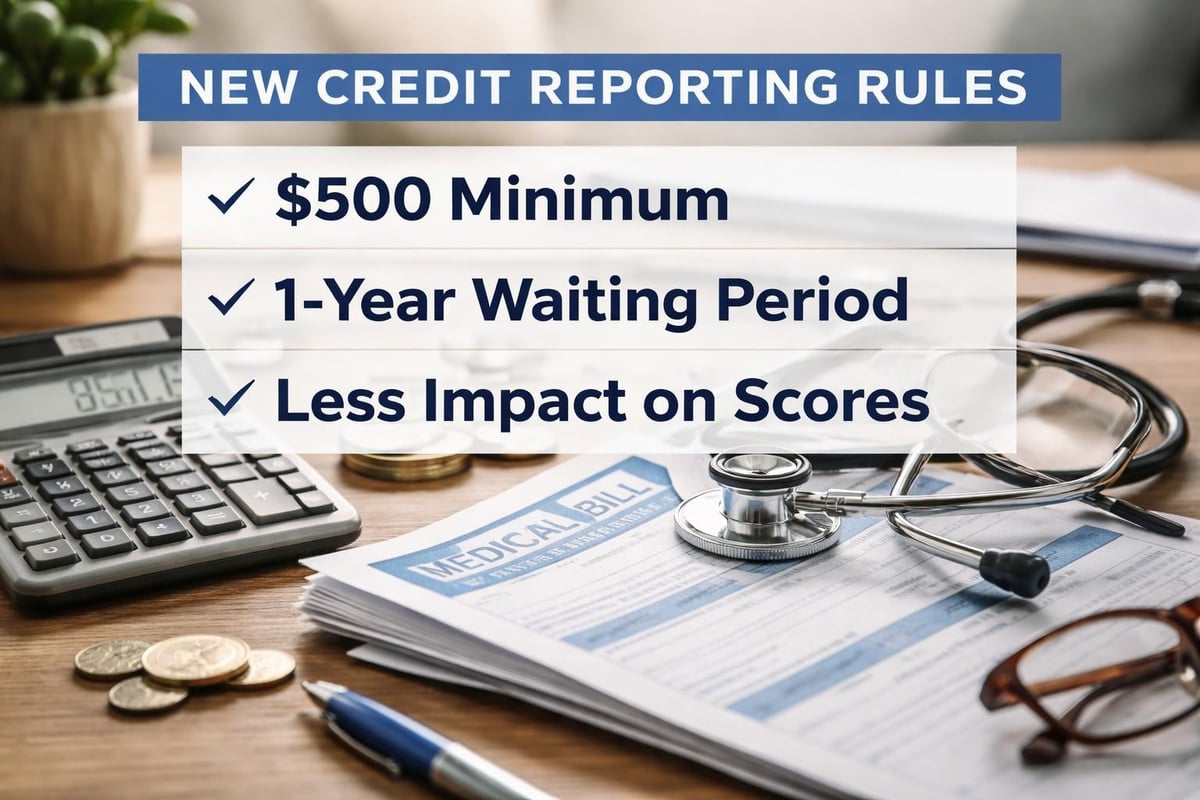

Medical collections differ from other collection types in important ways that affect your credit score. Recent changes to credit reporting and scoring have made medical collections less damaging than other debt types.

As of 2023, the three major credit bureaus don't report medical collections under $500, regardless of payment status. Additionally, they provide a one-year waiting period before reporting any medical collection, giving consumers time to resolve billing issues with insurance companies or healthcare providers.

Medical collection advantages include:

- Collections under $500 don't appear on credit reports

- One-year grace period before reporting

- FICO 10 ignores all paid medical collections

- Many lenders view medical debt differently than other collections

- More opportunities for financial assistance and payment plans

If you have medical collections, prioritize resolving these debts because they offer the best chance for credit score improvement when paid. The newer scoring models' favorable treatment of paid medical collections means settling these accounts can have immediate positive effects.

Rebuilding Credit After Resolving Collections

Paying off collections represents just one step in rebuilding your credit. A comprehensive approach to credit improvement delivers better long-term results than focusing solely on collection accounts.

After resolving collections, establish positive payment history with current accounts. Payment history remains the most significant factor in your credit score, so consistent on-time payments gradually offset the negative impact of past collections. Even small credit cards or secured cards used responsibly demonstrate creditworthiness.

Building Positive Credit Behavior

Opening a secured credit card provides an accessible way to rebuild credit after collections. These cards require a security deposit that becomes your credit limit, minimizing risk for the issuer while allowing you to establish positive payment patterns.

Strategic credit rebuilding includes multiple elements:

- Making all payments on time across all accounts

- Keeping credit card balances below 30% of limits

- Avoiding new collection accounts or delinquencies

- Maintaining older credit accounts to improve average account age

- Limiting hard inquiries by applying selectively for new credit

Consider becoming an authorized user on someone else's well-managed credit card. If the primary cardholder has excellent payment history and low utilization, their positive account information may appear on your credit report, potentially boosting your score.

Monitoring Your Credit Progress

Regular credit monitoring helps you track improvement and identify errors. You're entitled to free credit reports from each bureau annually through AnnualCreditReport.com. Stagger these requests every four months to maintain year-round visibility into your credit.

Review your reports for accuracy after paying collections. Ensure the accounts update to reflect payment within 30-45 days. Dispute any errors you find because inaccurate information can unfairly lower your score.

Special Considerations for Different Types of Debt

The type of debt in collections influences how payment affects your credit and how aggressively you should pursue resolution. Understanding these distinctions helps you prioritize which collections to address first.

Credit card collections typically result from unsecured debt and represent purely financial obligations. These collections carry standard treatment under credit scoring models and reporting timelines. Utility collections from phone, electric, or cable bills function similarly.

Auto loan or mortgage collections involve secured debts. While these still damage credit, they often accompany repossession or foreclosure, which create additional negative marks. Paying these collections doesn't remove the repossession or foreclosure from your report.

Student Loan Collections

Federal student loans in collections offer unique rehabilitation programs. Successfully completing a rehabilitation program (typically nine on-time payments over ten months) removes the collection from your credit report entirely. This opportunity doesn't exist for most other debt types.

Private student loan collections follow standard collection rules but may offer fewer resolution options than federal loans. These debts are generally not dischargeable in bankruptcy, making negotiation particularly important.

The Role of Time in Credit Score Recovery

While does paying off collections improve credit score is an important question, time also plays a crucial role in credit recovery. As collection accounts age, their impact on your credit score gradually decreases, even if they remain unpaid.

Credit scoring models weigh recent activity more heavily than older information. A five-year-old collection hurts your score less than a six-month-old one, assuming no other negative information has been added. This time-based diminishing impact occurs because older information predicts future behavior less accurately than recent activity.

| Collection Age | Relative Impact | Consideration |

|---|---|---|

| 0-12 months | Severe | Maximum negative impact |

| 1-3 years | Moderate-High | Still significantly damaging |

| 3-5 years | Moderate | Impact decreasing |

| 5-7 years | Low-Moderate | Approaching removal |

| 7+ years | None | Should be removed |

After seven years from the original delinquency date, collections must be removed from your credit report regardless of payment status. If a collection remains on your report beyond this period, dispute it with the credit bureaus for removal.

Common Mistakes to Avoid When Handling Collections

Many consumers inadvertently worsen their credit situations when attempting to resolve collections. Avoiding these common errors protects your credit and financial resources.

Never make a payment on an old collection without understanding the consequences. In some states, making a payment can restart the statute of limitations for legal collection, giving the agency more time to sue you. Verify your state's laws before paying debts approaching or past the statute of limitations.

Avoid acknowledging ownership of questionable debts. If you don't recognize a collection or believe it's not yours, don't admit responsibility. Instead, request validation and dispute the debt if the agency cannot provide adequate proof.

Additional mistakes include:

- Making electronic payments without written agreements

- Ignoring debt validation rights within the 30-day window

- Accepting verbal promises without written confirmation

- Failing to get pay-for-delete agreements in writing

- Not keeping records of all communications and payments

Don't assume all collection agencies are legitimate. Debt collection scams are common, with fraudsters posing as collection agencies to extract payment for nonexistent debts. Verify any collection with your credit report and request validation before making any payment.

Alternatives to Paying Collections in Full

When financial constraints prevent paying collections in full, several alternatives can help you address these debts while preserving your resources for other financial obligations.

Installment payment plans allow you to pay collections over time rather than in a lump sum. Many collection agencies accept monthly payments, though this approach may not improve your credit score until the debt is paid completely, depending on the scoring model used.

Debt settlement companies negotiate with collection agencies on your behalf, potentially reducing the amounts you owe. However, these services charge fees and may encourage you to stop paying current debts to fund settlements, which further damages your credit. Proceed cautiously with this option.

Consumer Credit Counseling

Non-profit credit counseling agencies offer free or low-cost assistance with debt management, including collections. These organizations can help you understand your options, create repayment plans, and sometimes negotiate with collection agencies.

Credit counselors provide objective advice without profit motives that might conflict with your best interests. They can assess whether paying specific collections makes financial sense given your overall situation and goals.

How Lenders View Paid Versus Unpaid Collections

Understanding lender perspectives helps you anticipate how paying collections affects your ability to secure financing. While credit scores provide standardized measures, lenders consider multiple factors when making approval decisions.

Mortgage lenders typically require resolution of all collections above certain dollar thresholds before closing. FHA loans, for example, mandate paying or establishing payment plans for collections over specific amounts. Paying these collections becomes necessary regardless of credit score impact.

Auto lenders and personal loan providers show more flexibility with collections, especially smaller amounts. However, they generally view paid collections more favorably than unpaid ones during manual underwriting. Demonstrating responsibility by resolving past debts can tip borderline applications toward approval.

Credit card issuers rely heavily on automated underwriting systems that primarily use credit scores. For these applications, whether you've paid collections matters less than your overall score, though newer scoring models that ignore paid collections may help.

Statute of Limitations Considerations

The statute of limitations determines how long collection agencies can legally sue you for unpaid debts. This timeframe varies by state and debt type, ranging from three to ten years in most jurisdictions.

Once the statute of limitations expires, collection agencies lose the legal right to sue you, though they can continue attempting to collect through phone calls and letters. The debt remains on your credit report until the seven-year reporting period expires, which is separate from the statute of limitations.

Understanding these distinctions matters when deciding whether to pay old collections. Paying a debt past the statute of limitations may restart that clock in some states, giving collectors renewed legal options. Additionally, very old debts nearing the seven-year reporting deadline may not justify payment from a credit perspective, though moral and ethical considerations remain personal decisions.

Understanding how collection accounts impact your credit score empowers you to make informed decisions about resolving past debts and rebuilding your financial foundation. While the answer to does paying off collections improve credit score depends on multiple factors, taking action to address these accounts generally supports your long-term financial health. If you're working to rebuild credit after resolving collections or need financing despite past credit challenges, Standard Financial offers flexible personal loan options designed for clients at all credit levels, with experienced staff at locations throughout Louisiana, Mississippi, Tennessee, and Georgia ready to help you move forward.

No comment yet, add your voice below!