A customer loan provides individuals with immediate access to funds for various personal needs, from unexpected medical expenses to planned home renovations. These financial products have become essential tools for millions of Americans seeking to manage cash flow, consolidate debt, or invest in life-improving purchases. Understanding the nuances of customer loan products helps borrowers make informed decisions that align with their financial goals and repayment capacity. Whether you're facing an emergency expense or planning a significant purchase, knowing your options empowers you to select the most suitable financing solution.

Understanding Customer Loan Fundamentals

A customer loan is a financial agreement where a lender provides a specific amount of money to a borrower, who agrees to repay the principal plus interest over a predetermined period. These loans differ from credit cards because they typically feature fixed repayment terms, predictable monthly payments, and lower interest rates for qualified borrowers.

The structure of a customer loan includes several key components that directly impact the total cost of borrowing. The principal represents the original amount borrowed, while the interest rate determines the cost of accessing those funds. Lenders calculate interest as either a fixed rate that remains constant throughout the loan term or a variable rate that fluctuates based on market conditions.

Key elements of customer loan agreements include:

- Loan term length (typically 12 to 84 months)

- Annual Percentage Rate (APR), which includes interest and fees

- Monthly payment amount

- Origination fees or closing costs

- Prepayment penalties or restrictions

- Collateral requirements for secured loans

Most personal customer loan products are unsecured, meaning they don't require collateral. Lenders approve these applications based on creditworthiness, income verification, and debt-to-income ratios. According to consumer lending regulations, financial institutions must follow specific guidelines to ensure fair lending practices and borrower protection.

Types of Customer Loan Products Available

Personal Loans for Home Improvement

Home improvement customer loan products enable homeowners to renovate, repair, or upgrade their properties without depleting savings. These loans typically range from $1,000 to $50,000, with repayment terms spanning three to seven years. Borrowers use these funds for kitchen remodels, roof replacements, HVAC installations, or energy-efficient upgrades that increase property value.

The advantage of dedicated home improvement financing lies in its flexibility compared to home equity products. Borrowers don't need substantial home equity to qualify, and the approval process moves faster than traditional home equity loans or lines of credit. Additionally, unsecured personal loans avoid placing a lien on the property.

Medical Expense Financing

Medical customer loan products address the growing challenge of healthcare costs not covered by insurance. These specialized loans help patients manage expenses for elective procedures, dental work, emergency treatments, or ongoing care needs. Many healthcare providers partner with lenders to offer financing options directly through medical offices.

Interest rates for medical loans vary significantly based on credit profiles and loan amounts. Some providers offer promotional periods with reduced or zero interest, making them attractive for borrowers who can repay quickly. However, understanding the terms after promotional periods end remains crucial for avoiding unexpected costs.

Educational Financing Solutions

While federal student loans remain the primary education funding source, customer loan products fill gaps for non-traditional educational expenses. These include vocational training, professional certifications, coding bootcamps, or continuing education courses that don't qualify for federal aid.

Education-focused personal loans offer flexibility for adult learners returning to school or professionals seeking career advancement through specialized training. The application process typically emphasizes current income and employment stability rather than academic enrollment status.

| Loan Type | Typical Amount | Common Term Length | Primary Use Cases |

|---|---|---|---|

| Home Improvement | $5,000-$50,000 | 3-7 years | Renovations, repairs, upgrades |

| Medical Expenses | $2,000-$35,000 | 2-5 years | Procedures, dental work, treatments |

| Educational | $3,000-$40,000 | 3-6 years | Certifications, training programs |

| Debt Consolidation | $5,000-$100,000 | 3-7 years | Credit card payoff, multiple debts |

The Customer Loan Application Process

Applying for a customer loan involves multiple steps designed to assess borrower qualifications and determine appropriate loan terms. The process begins with pre-qualification, where potential borrowers submit basic information to receive estimated rates without impacting credit scores.

The typical application workflow includes:

- Research and compare lenders based on rates, terms, and customer reviews

- Complete pre-qualification to understand potential approval odds

- Gather required documentation including pay stubs, tax returns, and identification

- Submit formal application with detailed financial information

- Undergo credit check and income verification

- Review and accept loan terms if approved

- Receive funds via direct deposit or check

Modern lenders increasingly streamline this process through digital platforms, enabling same-day or next-day funding for approved applicants. Technology has transformed customer loan accessibility, particularly for borrowers in underserved communities who previously faced limited options.

According to research on borrower expectations in consumer lending, today's customers prioritize transparent pricing, simple application processes, and flexible repayment options when selecting lenders.

Evaluating Customer Loan Offers Effectively

Comparing customer loan offers requires looking beyond advertised interest rates to understand the total cost of borrowing. The Annual Percentage Rate (APR) provides the most comprehensive comparison metric because it incorporates interest rates plus fees, presenting the true yearly cost.

Understanding Rate Structures

Fixed-rate customer loan products maintain consistent interest rates throughout the repayment period, creating predictable monthly payments that simplify budgeting. Variable-rate loans start with lower initial rates but adjust periodically based on index benchmarks, potentially increasing payment amounts over time.

For most personal borrowing needs, fixed rates offer superior planning advantages despite occasionally higher starting rates. The certainty of knowing exact payment obligations helps borrowers avoid financial surprises during economic fluctuations.

Analyzing Fees and Additional Costs

Origination fees represent a percentage of the loan amount charged upfront, typically ranging from 1% to 8% of the principal. Some lenders deduct these fees from disbursed funds, while others add them to the total amount owed. Understanding how origination fees impact the actual funds received helps borrowers accurately assess whether the loan meets their needs.

Late payment fees, prepayment penalties, and insufficient funds charges add potential costs that vary significantly among lenders. Reviewing fee schedules carefully prevents unexpected expenses and helps identify the most borrower-friendly terms.

When evaluating offers, resources like NerdWallet’s personal loan rating methodology provide frameworks for comparing lenders across multiple dimensions beyond just rates.

| Evaluation Factor | Why It Matters | What to Look For |

|---|---|---|

| APR | True cost comparison | Lowest rate for your credit tier |

| Origination Fees | Upfront costs | 0-2% or no fee options |

| Repayment Terms | Monthly payment size | Term length matching budget |

| Prepayment Options | Early payoff flexibility | No penalties for extra payments |

| Customer Service | Support accessibility | Multiple contact channels |

Improving Customer Loan Approval Chances

Borrowers with less-than-perfect credit histories often believe customer loan approval remains out of reach, but specialized lenders recognize that past financial challenges don't necessarily predict future repayment behavior. Several strategies improve approval odds and potentially secure better terms.

Building a Stronger Application

Demonstrating stable employment history shows lenders consistent income for meeting payment obligations. Applicants who've maintained the same job for at least two years present lower risk profiles than those with frequent employment changes. Similarly, longer residence at current addresses indicates stability that lenders value.

Reducing debt-to-income ratios before applying strengthens applications significantly. Lenders prefer borrowers whose total monthly debt payments consume less than 36% of gross monthly income. Paying down existing balances or increasing income through additional work can shift applications from denied to approved.

Innovative solutions like identity verification for thin-file applicants help lenders serve underbanked populations who lack extensive credit histories but demonstrate creditworthiness through alternative data points.

Considering Co-Signers or Collateral

Adding a creditworthy co-signer transforms an otherwise risky application into an approvable one by guaranteeing a second party's responsibility for repayment. Co-signers with strong credit profiles enable primary borrowers to access customer loan products with better rates than they'd qualify for independently.

Secured customer loan options require collateral such as vehicles, savings accounts, or other valuable assets. While risking collateral loss upon default, secured loans offer lower interest rates and higher approval rates for credit-challenged borrowers.

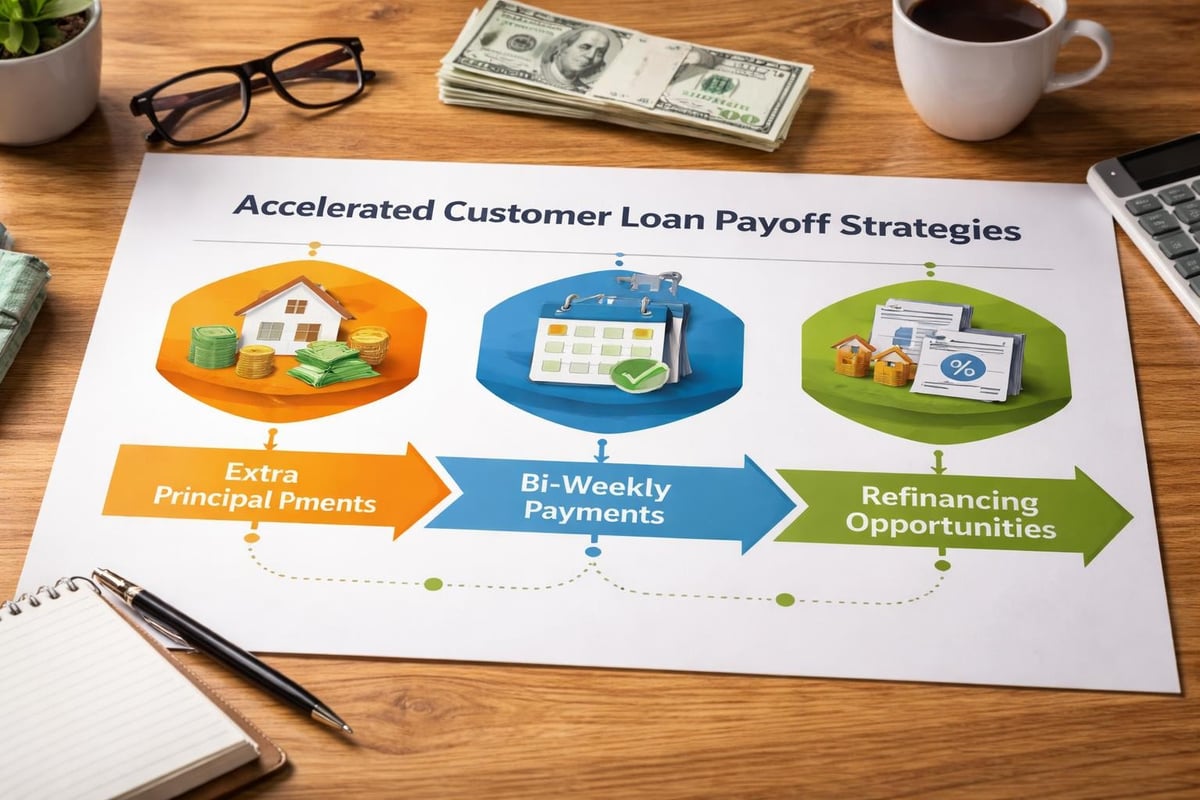

Managing Customer Loan Repayment Successfully

Responsible customer loan management extends beyond simply making monthly payments on time. Strategic approaches to repayment optimize financial outcomes and build stronger credit profiles for future borrowing needs.

Effective repayment strategies include:

- Setting up automatic payments to avoid late fees and missed payments

- Making bi-weekly half-payments instead of monthly full payments to reduce interest

- Applying windfalls or bonuses toward principal reduction

- Refinancing to lower rates when credit scores improve

- Maintaining emergency savings to prevent payment interruptions

Payment history comprises 35% of FICO credit scores, making consistent on-time payments the most impactful factor for credit improvement. Even one missed payment can damage scores significantly, while maintaining perfect payment records steadily builds creditworthiness.

Borrowers facing temporary financial hardship should contact lenders immediately to discuss hardship programs, payment deferrals, or modified arrangements. Most lenders prefer working with struggling borrowers over initiating collection processes, making early communication essential.

Regional Considerations for Customer Loan Access

Geographic location influences customer loan availability, rates, and terms due to varying state regulations, local economic conditions, and lender presence. Southeastern states including Louisiana, Mississippi, Tennessee, and Georgia feature diverse lending landscapes shaped by both national institutions and regional specialists.

Understanding State-Specific Regulations

Each state maintains unique consumer protection laws governing maximum interest rates, fee structures, and lending practices. Louisiana law limits certain loan fees and requires specific disclosures, while Mississippi regulations focus on licensing requirements for lenders operating within state borders. Tennessee and Georgia enforce their own consumer protection frameworks that shape available customer loan products.

Borrowers benefit from researching state-specific regulations to understand their rights and protections. State banking departments provide resources explaining local lending laws and offer complaint resolution services for disputes with lenders.

Accessing Local Lending Options

Branch-based lenders with physical locations throughout the Southeast offer personalized service and relationship-building opportunities that online-only lenders cannot match. Meeting loan officers face-to-face enables borrowers to explain unique circumstances, discuss flexible options, and build long-term banking relationships.

Community-focused lenders often consider factors beyond credit scores, evaluating local employment stability, family circumstances, and demonstrated commitment to financial improvement. This holistic approach particularly benefits borrowers with past credit challenges who've since established stable financial foundations.

Customer Loan Alternatives and Complementary Products

While customer loan products serve many financial needs effectively, alternative solutions sometimes offer superior benefits depending on specific circumstances. Understanding the full range of options ensures optimal decision-making.

Home Equity Products

Homeowners with substantial equity might find home equity loans or lines of credit (HELOCs) provide lower rates than unsecured customer loan products. These secured options leverage property value to reduce lender risk, translating to borrower savings. However, they require home equity, lengthier approval processes, and place properties at risk if payments cease.

Credit Card Balance Transfers

For debt consolidation needs, promotional credit cards offering 0% APR balance transfer periods sometimes beat customer loan economics. Borrowers who can repay balances within promotional windows avoid interest charges entirely. This strategy requires discipline and careful monitoring of promotional expiration dates.

Refinancing Existing Loans

Borrowers with improved credit scores or decreased interest rate environments should regularly evaluate refinancing opportunities for existing customer loan obligations. Refinancing replaces current loans with new ones featuring better terms, reducing total interest costs and potentially lowering monthly payments.

| Option | Best For | Key Advantage | Main Drawback |

|---|---|---|---|

| Personal Loan | Most general needs | Fixed terms, predictable payments | Higher rates for fair credit |

| Home Equity | Large amounts, homeowners | Lowest rates available | Property at risk |

| Balance Transfer | Debt consolidation | 0% promotional periods | Limited time frame |

| Refinancing | Existing loans | Improved terms | Application requirements |

The Future of Customer Loan Products

Consumer lending continues evolving rapidly through technological innovation, changing regulatory frameworks, and shifting customer expectations. Emerging trends shape how borrowers access customer loan products and interact with lenders throughout the borrowing lifecycle.

Artificial intelligence and machine learning enable lenders to assess creditworthiness using alternative data beyond traditional credit scores. These technologies identify qualified borrowers previously overlooked by conventional underwriting, expanding access while maintaining responsible lending standards.

Mobile-first experiences dominate modern customer loan applications, with borrowers expecting seamless smartphone-based processes from initial research through final payment. Lenders investing in intuitive mobile platforms gain competitive advantages by meeting customer preferences for convenient, anywhere access.

Personalization through data analytics allows lenders to tailor customer loan offers matching individual circumstances, preferences, and goals. Rather than one-size-fits-all products, future lending emphasizes customized solutions addressing specific borrower needs.

Environmental, social, and governance (ESG) considerations increasingly influence lending decisions, with some institutions offering preferential rates for energy-efficient home improvements or education in high-demand fields. These purpose-driven customer loan products align borrower goals with broader societal benefits.

Understanding customer loan options, application processes, and repayment strategies empowers borrowers to make confident financial decisions aligned with their goals and circumstances. Whether financing home improvements, medical expenses, or educational pursuits, selecting the right loan product and lender creates foundations for successful outcomes. Standard Financial serves Louisiana, Mississippi, Tennessee, and Georgia communities with flexible customer loan solutions designed for diverse needs and credit profiles, including options for those rebuilding their financial futures. Visit a nearby branch location to discuss personalized financing plans with experienced loan officers committed to your success.

No comment yet, add your voice below!