Applying for personal financing has become increasingly streamlined in recent years, yet many potential borrowers still find the process intimidating. Understanding how to properly complete a consumer loan application can significantly improve your chances of approval and help you secure favorable terms. Whether you're seeking funds for home improvements, medical expenses, or education, knowing what lenders expect and how to present your financial situation effectively makes all the difference in achieving your financing goals.

Understanding the Consumer Loan Application Process

A consumer loan application serves as the formal request for borrowed funds from a financial institution. This document collects essential information about your financial history, employment status, income sources, and the purpose of the loan. Lenders use this data to assess your creditworthiness and determine whether extending credit aligns with their risk tolerance.

The modern application process typically begins with a preliminary inquiry where you provide basic information. Many institutions now offer online portals that allow you to start your application from home, though some applicants prefer the personalized guidance available at physical branch locations. The consumer lending process is governed by federal regulations designed to protect both borrowers and lenders.

Digital vs. Traditional Application Methods

Today's borrowers can choose between digital platforms and traditional paper applications. Online submissions often provide instant pre-qualification decisions, allowing you to understand your potential approval odds within minutes. These systems use automated underwriting algorithms that quickly analyze your credit profile and financial ratios.

Traditional in-person applications offer distinct advantages for applicants with unique circumstances. Meeting face-to-face with a loan officer allows you to explain credit challenges, discuss flexible payment options, and receive personalized advice about strengthening your application. This approach proves particularly valuable for borrowers with past credit issues who benefit from human review rather than purely algorithmic assessment.

Essential Documentation for Your Consumer Loan Application

Gathering the right documents before starting your consumer loan application saves time and prevents delays. The personal loan application checklist varies slightly between lenders, but most require similar core documentation to verify your identity, income, and financial stability.

Required Personal Identification:

- Government-issued photo ID (driver's license or passport)

- Social Security card or verification of your Social Security number

- Proof of current address (utility bill, lease agreement, or mortgage statement)

- Contact information for references

Financial Documentation:

- Recent pay stubs covering the last 30-60 days

- W-2 forms or tax returns from the previous two years

- Bank statements from the past two to three months

- Documentation of additional income sources (rental income, alimony, investment returns)

Self-employed applicants face additional documentation requirements. You'll typically need profit and loss statements, business tax returns, and potentially a balance sheet demonstrating your business's financial health. These documents help lenders verify that your income remains stable and sufficient to support loan repayment.

Preparing Your Loan Application Packet

Creating a comprehensive loan application packet demonstrates your organizational skills and financial responsibility to potential lenders. The Consumer Financial Protection Bureau recommends assembling all necessary documents before beginning the formal application process.

Organize your materials logically, grouping similar documents together. Create clear labels for each section: identification, income verification, assets, and liabilities. This structured approach allows loan officers to review your application efficiently and reduces the likelihood of follow-up requests for missing information.

| Document Category | Typical Requirements | Purpose |

|---|---|---|

| Identification | Photo ID, SSN verification | Confirm identity and prevent fraud |

| Income Proof | Pay stubs, tax returns, bank statements | Verify ability to repay |

| Employment | Contact information, employment history | Assess job stability |

| Debt Information | Credit card statements, existing loans | Calculate debt-to-income ratio |

Credit Considerations in Consumer Loan Applications

Your credit profile plays a central role in the consumer loan application evaluation process. Lenders examine your credit score, payment history, credit utilization, and the mix of credit accounts you maintain. Understanding these factors allows you to address potential concerns proactively.

Credit scores range from 300 to 850, with higher scores indicating lower credit risk. Most lenders categorize scores into tiers that determine approval likelihood and interest rates. Excellent credit (740+) typically qualifies for the best terms, while fair to poor credit (below 670) may require additional documentation or result in higher interest rates.

Key Credit Factors Lenders Evaluate:

- Payment history (35% of your score)

- Credit utilization ratio (30% of your score)

- Length of credit history (15% of your score)

- New credit inquiries (10% of your score)

- Credit mix diversity (10% of your score)

Even applicants with challenged credit histories can successfully complete a consumer loan application. Specialized lenders focus on current financial stability rather than exclusively relying on past credit performance. Demonstrating steady employment, sufficient income, and responsible management of recent financial obligations strengthens applications despite previous credit issues.

Improving Your Application Before Submission

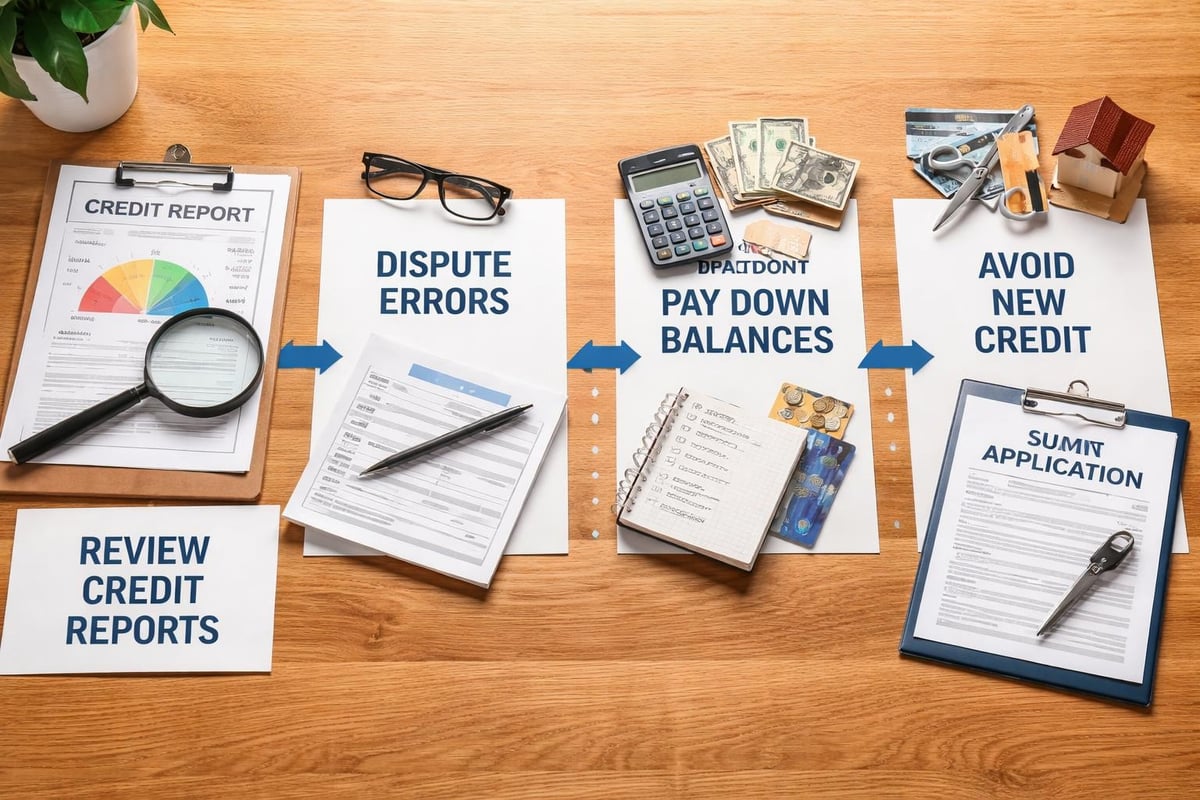

Strategic preparation can significantly enhance your consumer loan application's success rate. Begin by reviewing your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) at least 60 days before applying. Dispute any inaccuracies you discover, as correcting errors can improve your score.

Reduce outstanding credit card balances to lower your credit utilization ratio. Ideally, keep balances below 30% of your available credit limits, though under 10% demonstrates even stronger financial management. Avoid opening new credit accounts immediately before applying, as recent inquiries can temporarily lower your score.

Income and Employment Verification Requirements

Lenders need confidence that you possess sufficient income to manage monthly loan payments alongside your existing financial obligations. The income verification portion of your consumer loan application requires detailed documentation of all revenue sources.

Standard employment verification includes confirmation of your job title, hire date, and salary. Many lenders contact employers directly or use third-party verification services to confirm the information you provide. Having your employer's HR department contact information readily available expedites this process.

Alternative Income Documentation:

- Rental property income with lease agreements and deposit records

- Investment income with brokerage statements

- Retirement or pension income with award letters

- Disability or Social Security benefits with official documentation

- Alimony or child support with court orders and payment records

The Washington State Department of Financial Institutions provides helpful guidance about documenting various income types for loan applications. Consistent income over extended periods carries more weight than recent increases, as lenders seek stability rather than short-term earnings spikes.

Calculating Debt-to-Income Ratio

Your debt-to-income (DTI) ratio represents the percentage of your gross monthly income committed to debt payments. Lenders calculate this metric by dividing your total monthly debt obligations by your gross monthly income. Most consumer loan applications receive favorable consideration with DTI ratios below 43%, though some lenders accept higher ratios depending on other compensating factors.

Lower DTI ratios indicate greater capacity to absorb additional debt payments comfortably. If your ratio exceeds ideal thresholds, consider paying down existing debts before submitting your consumer loan application. Even small reductions in monthly obligations can meaningfully improve your DTI calculation.

The Application Review and Approval Timeline

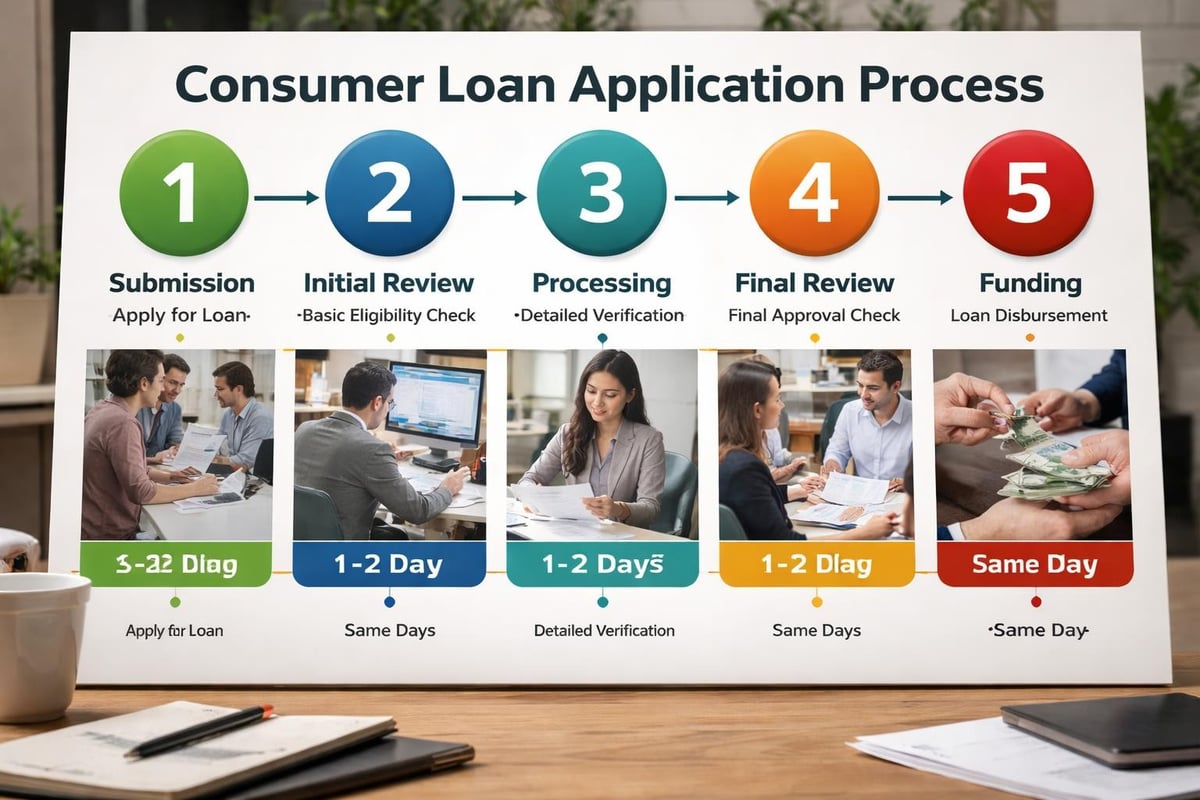

After submitting your consumer loan application, the review process begins. Understanding typical timelines helps manage expectations and plan accordingly. Initial pre-qualification decisions for straightforward applications often arrive within 24-48 hours, while comprehensive underwriting may require one to two weeks.

Typical Application Processing Stages:

- Initial Review (1-2 business days): Verification that application is complete and meets basic eligibility requirements

- Credit Analysis (2-3 business days): Detailed examination of credit reports and scores

- Income Verification (3-5 business days): Confirmation of employment and income documentation

- Underwriting Decision (1-3 business days): Final approval, conditional approval, or denial determination

- Funding (1-3 business days after approval): Transfer of approved loan amount

The complete lending process involves multiple checkpoints designed to protect both borrowers and lenders. Conditional approvals require additional documentation or clarification before final funding authorization.

Common Reasons for Application Delays

Several factors can extend the consumer loan application timeline beyond standard processing periods. Missing or incomplete documentation tops the list of delay causes. Submitting all required materials initially prevents back-and-forth communication that adds days to the review process.

Employment verification challenges occur when lenders struggle to reach HR departments or when applicants recently changed jobs. Self-employed borrowers experience longer verification periods due to the complexity of documenting variable income streams. Credit report discrepancies requiring investigation or disputes also extend timelines significantly.

Understanding Loan Terms and Conditions

Once your consumer loan application receives approval, carefully review all terms and conditions before accepting the offer. The loan agreement specifies critical details including the principal amount, interest rate, repayment schedule, fees, and any prepayment penalties.

Annual Percentage Rate (APR) represents the true cost of borrowing, incorporating both the interest rate and applicable fees. Comparing APRs across multiple offers provides clearer cost comparisons than interest rates alone. Fixed-rate loans maintain consistent payments throughout the loan term, while variable-rate products adjust based on market conditions.

| Loan Feature | Fixed-Rate Option | Variable-Rate Option |

|---|---|---|

| Payment Predictability | Consistent monthly amount | Fluctuates with rate changes |

| Rate Protection | Locked throughout term | Subject to market conditions |

| Initial Rate | Typically higher | Often lower initially |

| Budget Planning | Easier to plan | Requires flexibility |

Payment schedules vary by lender and loan type. Most consumer loans use monthly payment structures, though some institutions offer bi-weekly or customized schedules. Shorter loan terms result in higher monthly payments but lower total interest costs over the life of the loan.

Rights and Protections for Borrowers

Federal and state regulations provide important protections throughout the consumer loan application and repayment process. The Truth in Lending Act requires lenders to disclose all loan costs clearly, allowing informed borrowing decisions. The Equal Credit Opportunity Act prohibits discrimination based on race, color, religion, national origin, sex, marital status, age, or income source.

Understanding these protections empowers you to recognize any irregularities in how your consumer loan application is processed. If denied, lenders must provide specific reasons for the decision, allowing you to address concerns before reapplying. You have the right to review any credit reports used in the decision-making process.

Special Considerations for Different Loan Purposes

The intended use of loan proceeds can influence both the consumer loan application requirements and the terms offered. Home improvement loans may require contractor estimates or project plans. Medical expense financing might need billing statements or treatment cost documentation. Educational loans could require enrollment verification or tuition invoices.

Purpose-specific loans sometimes offer advantages over general personal loans. Lenders may extend more favorable terms when funds serve clearly defined, value-enhancing purposes. Home improvement loans, for example, can increase property value, potentially justifying lower interest rates than unsecured personal loans.

Loan Purpose Categories:

- Home improvements and repairs

- Medical and dental procedures

- Educational expenses and tuition

- Debt consolidation

- Major purchases (appliances, furniture)

- Emergency expenses

- Special events (weddings, vacations)

Some states impose specific requirements for certain consumer loan types and amounts. The California Department of Financial Protection and Innovation details regulations for loans between $2,500 and $10,000, including rate limitations and borrower education requirements. Understanding jurisdiction-specific rules ensures your application complies with applicable regulations.

Refinancing and Subsequent Applications

Borrowers with existing consumer loans may eventually consider refinancing to secure better terms or consolidate debt. The refinancing application process closely resembles initial loan applications, requiring updated financial documentation and credit review.

Successful loan repayment history strengthens subsequent consumer loan applications significantly. Demonstrating responsible payment behavior builds lender confidence and often qualifies you for improved terms. Many borrowers refinance after credit score improvements or income increases make them eligible for lower interest rates.

Timing matters when considering refinancing or additional borrowing. Allow sufficient time between applications to avoid excessive hard inquiries on your credit report. Multiple inquiries within short periods can negatively impact your credit score and raise lender concerns about financial distress.

Building Long-Term Lender Relationships

Establishing positive relationships with financial institutions benefits future borrowing needs. Customers with strong payment histories often receive streamlined application processes, pre-approved offers, and preferential rates. Maintaining accounts in good standing positions you favorably when submitting future consumer loan applications.

Regional lenders with multiple branch locations often provide personalized service that national institutions cannot match. These relationships prove particularly valuable when life circumstances create unique financing needs or when explaining credit challenges requires nuanced understanding rather than algorithmic assessment.

Successfully navigating the consumer loan application process requires preparation, organization, and understanding of lender expectations. Whether you need financing for home improvements, medical expenses, education, or other important life needs, proper documentation and credit awareness significantly improve approval odds. Standard Financial specializes in helping borrowers throughout Louisiana, Mississippi, Tennessee, and Georgia secure flexible financing solutions, even when past credit issues complicate applications. With multiple convenient branch locations and a commitment to personalized service, Standard Financial's experienced team can guide you through every step of the application process and help you find the right financing solution for your specific situation.

No comment yet, add your voice below!